South Africa’s state-owned special risks insurer SASRIA told Parliament it is working towards R30 billion in own funds by 2029 as it rebuilds after the July 2021 unrest generated roughly R32bn in claims and pushed its solvency position below zero.

In a briefing to the National Council of Provinces’ Select Committee on Finance this month, SASRIA’s representatives outlined the insurer’s performance, financial sustainability, governance, and progress since the committee’s last engagement with it in 2023.

Chief executive Mpumi Tyikwe said SASRIA’s “Vision 2029” strategy includes a longer-term reserve target of R200bn, although the formal near-term target is R30bn by 2029.

SASRIA is a legislated monopoly providing cover against politically motivated unrest, strikes, riots, terrorism, and public disorder, distributed through private insurers as agent companies and written on the back of underlying insurance policies.

Tyikwe said SASRIA has been in a rebuilding phase since 2021, with gross written premiums (GWP) rising from R2.786bn (2020/21) to R5.851bn (2024/25).

For 2024/25, SASRIA reported insurance revenue of R5.76bn (up by 9.7%), gross claims incurred of R666 million (claims ratio of 11.6%), and profit for the year of R4.469bn (+34.1%).

The improvement in profitability was supported by stronger investment earnings and a better net insurance outcome: SASRIA reported an increase of 26% in net investment income to R1.267bn and 48.9% increase in the net insurance result to R2.949bn, alongside a 55.4% fall in net insurance expenses to R592m.

On the balance sheet, SASRIA reported an increase of 27.1% in total assets to R20.914bn, total liabilities of R2.302bn, and total equity of about R18.6bn at 31 March 2025, with assets under management of R16.557bn (+25.7%) and reinsurance contract assets of R1.583bn (+38%).

However, Tyikwe said SASRIA’s post-2021 profits have not yet fully offset the total losses from the July 2021 unrest, with reserve rebuilding continuing through retained earnings and pricing changes.

SASRIA’s presentation recorded it has historically paid R11.1bn in dividends and R4.6bn in income tax to the government.

Tyikwe told the committee that about R16bn had previously been withdrawn from SASRIA, and if those funds had remained invested, they could have grown to an estimated R55bn, materially strengthening SASRIA’s ability to absorb the July 2021 losses.

He added that National Treasury has agreed not to request dividends until SASRIA reaches its R30bn reserve target.

SCR doesn’t fully reflect capital requirement

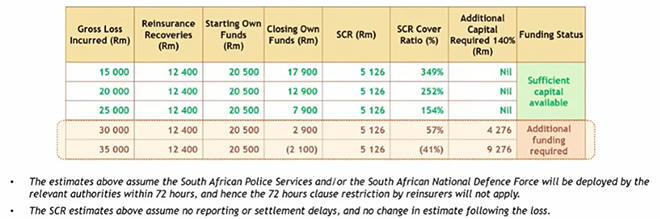

SASRIA reported a Solvency Capital Requirement (SCR) ratio of 400% as at 31 December 2025, above its internal target of 230%, with available capital of R21.6bn at the same date.

Tyikwe highlighted what he described as a key lesson from the July 2021 shock: SASRIA had an SCR of about 350% going into the unrest yet still became insolvent when the scale of losses overwhelmed its capital base.

He described SASRIA’s business as low-frequency but high-severity and told the committee the SCR “is really not a true reflection” of the capital SASRIA needs to prepare for a catastrophe event like July 2021.

SASRIA’s data underlined the point: its presentation cited a modelled probable maximum loss of R12bn (2021) against actual claims of about R32bn, and it reported a 10-year average loss ratio of 30.3% excluding July 2021, rising to above 1 000% if the 2021 losses are included.

On the 2021 event itself, Tyikwe said SASRIA received 17 571 claims with total losses of about R32bn, and losses escalated quickly: by the fourth day of unrest, claims had climbed to about R14bn.

He said a key modelling gap before July 2021 was the extent of the breakdown in policing and public-order responses, which SASRIA said contributed to the escalation and spread of losses. SASRIA has since incorporated assumptions about possible failures in security responses into future scenarios.

SASRIA said the July 2021 claims experience drove its SCR ratio below zero and resulted in a R22bn government injection, after which SASRIA implemented premium increases, revised reinsurance structures, and withdrew its wrap cover product at the time.

In April this year, SASRIA reintroduced its wrap cover as an excess-of-loss layer above the R500m primary limit with an additional R500m limit.

Read: SASRIA reintroduces wrap cover with reduced limit

Full reinsurance secured

Tyikwe said SASRIA’s reinsurance buying has strengthened over the past three years and reported that reinsurance capital purchased rose from R5.9bn (2024/25) to R10.1bn (2025/26), with a projected increase to R12.4bn (2026/27).

He said SASRIA has been able to secure full reinsurance for 2026/27, the first time in the past three years it has achieved this.

SASRIA struggled to obtain reinsurance for 2024/25 because reinsurers are sensitive to election periods, and the May 2024 national and provincial elections were one of the factors affecting market appetite and terms.

On the size of a shock it can withstand, Tyikwe said SASRIA can currently deal with an event of up to about R25bn, based on its own funds and reinsurance arrangements.

Premium increases and affordability

SASRIA projected GWP of R6.4bn by 31 March 2026, reflecting premium increases implemented in 2022 and a further 25% weighted average premium increase in October 2025.

ANC MP Tidimalo Legwase asked how much of SASRIA’s improved profitability is attributable to premium increases versus improved underwriting and raised affordability concerns for SMMEs and municipalities.

SASRIA board chairperson Nolwandle Mgoqi said SASRIA is pursuing more risk-based pricing, with increased differentiation by sector and geography, but is balancing affordability and sustainability rather than relying only on premium increases.

She cautioned that sustained premium growth well above inflation – particularly at double-digit levels – could become unaffordable in a low-growth economy.

Taxpayer backstop?

Democratic Alliance MP Joseph Britz pressed the insurer on whether it could withstand another large, multi-provincial unrest event without returning to National Treasury, arguing that the 2021 losses had already exceeded SASRIA’s long-term reserve ambitions and effectively left taxpayers as the backstop.

Mgoqi responded that SASRIA’s position is “significantly stronger” after rebuilding capital through retained earnings, pricing adjustments, and strengthened reinsurance arrangements, but she cautioned that no insurer operating in this environment could absorb a prolonged nationwide unrest event without some level of external support.

She said SASRIA operates with a sovereign guarantee because it insures risks private markets cannot absorb, making the fiscus the ultimate backstop in extreme scenarios even while SASRIA works to reduce reliance through capital accumulation, improved underwriting practices, and expanded risk-transfer mechanisms.

Operational readiness

SASRIA told the committee that July 2021 revealed operational constraints: it had to process around 20 000 claims, compared with a typical annual volume of about 3 000, and noted that many of its processes were manual.

Tyikwe said SASRIA is investing in technology to automate linkages with agent insurers so it can handle a future major event more effectively. SASRIA has made “significant progress” in obtaining policyholder-level data, including where policyholders are located and what risks are covered – data it said was previously retained by agent insurers.

On July 2021 claims closure, Tyikwe told MPs that only 44 claims remain outstanding with a combined value of about R105m, with some linked to legal disputes and complex settlement processes.

Questions about irregular and fruitless expenditure

DA MP Paul Swart noted SASRIA’s clean audit outcomes but raised concerns about recurring irregular and fruitless expenditure, including irregular expenditure linked to asset management fees paid under expired contracts.

Swart also pointed to a spike in irregular expenditure to R16.83m in 2023/24 and questioned whether internal controls and consequence management were adequate.

Mgoqi said the board has strengthened procurement controls and compliance oversight, and said the irregular expenditure reflected procurement process deviations rather than fraud, while acknowledging that a clean audit should not obscure governance risks.