As US equities maintain their dominance, PSG Asset Management’s chief investment officer, John Gilchrist, cautions that investors could be heading into a more difficult decade.

Speaking at the PSG Outlook 2025 event on 28 January in Cape Town, Gilchrist (pictured) posed a key question: “History suggests a more challenging period lies ahead. Are you and your clients well positioned?”

Before delving into the historical context and its potential impact on the next 10 years, Gilchrist reflected on the current market outlook and positioning. He noted several red flags after reviewing various market commentaries, outlook presentations, surveys, and valuations.

“There’s a massive amount of consensus about what’s going to happen through 2025 and beyond,” he said. “And in particular, a lot of that consensus seems to be simply an extrapolation of what’s been happening in the recent past – with the S&P up 24% and 23% in back-to-back years.”

Gilchrist explained that this consensus appears to have led to overconfidence and even complacency, resulting in a significant concentration of investments in specific areas of the market.

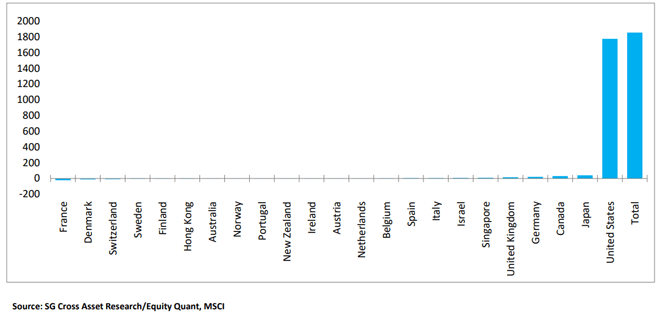

For example, looking at 2024 from a financial market perspective, he pointed out that global capital was largely supported by US equities, which now make up 74% of the MSCI World Index.

Digging deeper, Gilchrist noted that US equities were primarily driven by the Magnificent Seven stocks. Commonly referred to as the Mag Seven, these stocks represent seven of the most dominant and influential technology companies in the US stock market – Apple, Microsoft, Alphabet (parent company of Google), Amazon, Nvidia, Meta Platforms, and Tesla.

To put it into perspective, about 70% of the S&P 500’s 23% growth in 2024 was driven by these seven stocks, while in 2023, roughly 80% of the S&P’s 24% increase came from the same group. In total, global capital investment in US publicly traded bonds and equities from outside the US has reached about $32.5 trillion.

“What really concerns us is, if you have a look where that concentration is, it’s exactly in the areas that are most stretched from a valuation perspective,” he added.

Consensus

Gilchrist observed there is a significant consensus in the market regarding US exceptionalism, with the prevailing message that the US is dominating across the board and will continue to do so, making it the place to invest.

He noted that this assumption was already reflected in the markets before Donald Trump was sworn in for his second term as US president on 20 January. However, Gilchrist warned that nobody knows what policies Trump will implement, how he will go about it, or the unintended consequences of those policies. Yet, he observed, the market seems to operate under the assumption that the markets will serve as Trump’s primary constraint.

Recalling Trump’s first term, Gilchrist pointed out that Trump used the equity market as a barometer of his success. “The assumption seems to be he’s doing some negotiation tactics, but that he’s not going to do anything that jeopardises the equity market, because he’s a billionaire, and because he has got the backing of billionaires,” he said.

This, according to Gilchrist, has led to a level of complacency in the market, particularly because the potential unintended consequences of Trump’s policies remain unknown.

Gilchrist further explained that although Trump’s overall policy package may seem coherent, the sequencing risk associated with those policies and the pressures they may face from legal or practical challenges appear to be under-estimated.

“It ignores the potential for delays or challenges from a legal perspective or just a practical perspective, and assumes everything is implemented without unintended consequences,” he added.

Concentration

A chart depicting country contributions to the MSCI World 2024 price performance in basis points shows just how dominant the US market has been.

Gilchrist said concentration becomes particularly dangerous when it is in areas of the market where valuations are stretched. However, he explained that when applying the PSG investment process, PSG becomes particularly excited when it finds opportunities where earnings are low, ideally due to temporary factors, and where the valuation linked to those earnings is also low.

“Because then what can happen is those earnings and the valuation multiple on those earnings can also grow. That’s when you get exceptional returns. So that’s what we like to see,” he said.

Turning to the S&P 500, Gilchrist noted that earnings are currently high and expected to grow even faster. However, he cautioned that the price-to-earnings ratio for those anticipated earnings is at its highest point in years, not far from the levels seen during historic market peaks.

“This is the area of caution,” Gilchrist added. “Given our philosophy, we have concerns regarding overall US markets.”

US markets’ lost decade?

Gilchrist invited the audience to imagine the scenario of an investor in 2035 looking back at a decade of market returns, and what they could potentially see, based on long-term data patterns. Although these were not predictions, they offered the valuable perspective that things may turn out differently than many currently imagine.

One of the possibilities discussed was the prospect of another lost decade for US markets, similar to that seen from 2000 to 2010.

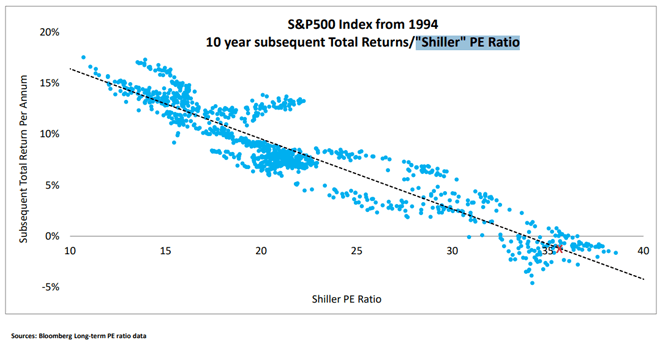

Explaining the methodology, Gilchrist referred to the Shiller PE Ratio, which has been calculated back to 1871.

“The Shiller PE or cyclically adjusted PE is the current share price divided by the last 10 years of earnings (adjusted for inflation). Historically, the higher the cyclically adjusted price-earnings, the lower the subsequent 10-year average return,” he noted in reference to the S&P 500 chart (shown above).

“And it’s a pretty strong relationship, and it makes sense, if you pay more for something, you’re likely to get a lower return.”

Gilchrist outlined the chart would seem to indicate that “Given the starting valuation, you’re looking at minus 2% from S&P per year for 10 years. Obviously, there’s a range within that, but there aren’t many historic data points above low single-digit returns given the current starting level. That’s what the long-term data would suggest.”

Weak US dollar?

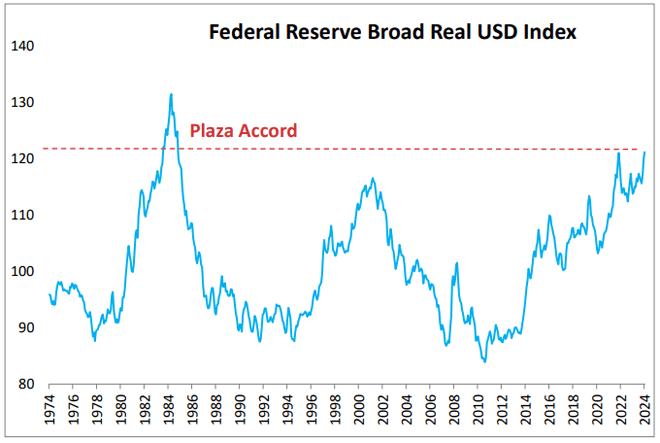

Presenting a chart from Bloomberg dating back to 1974, Gilchrist underscored two key points: the dollar is currently at its highest levels in 40 years, and there have been 15 years of exceptionally strong US dollar performance.

Gilchrist said what is interesting is that although Trump’s policies are generally seen to be supportive of the dollar, he has stated that he wants a weak dollar. Instead, Gilchrist says Trump might get his weaker dollar through a different mechanism.

Gilchrist observed, “One of the things that people just assume as a given is that the US has this exorbitant privilege as a reserve currency, and they can pretty much do what they want on the fiscal side. We don’t think that’s the case. We think the markets are going to start getting more and more cautious about the abuse of the fiscal situation.”

He pointed out that markets are not completely oblivious to this. Citing the 10-year US bond yield, Gilchrist explained, “From the time that Trump moved ahead in the polls in September, it moved from 3.8% up to 4.8%.”

Additionally, “The inflation breakeven moved from 2.1% to 2.4%, so there is some concern from a fiscal and inflation perspective.”

Putting the US fiscal situation into context, Gilchrist noted that the total US government debt stands at about $36 trillion, with nearly $30 trillion held by the public. The budget deficit is about $1.9 trillion. He said, “What the US needs to do is be able to attract $1.9 trillion every year and keep existing investors happy.”

In other words, Trump must maintain investor confidence to ensure continued investment in the US.

“And if you look at what underpins a strong dollar: fiscal prudence, monetary credibility – I think the monetary authorities in the US have taken a hit given their approach to transitory inflation, balance of payments – political stability, and military competence. All of those are potentially challenged.”

Volatile US bonds that don’t protect?

Gilchrist warned that history indicates investors may no longer experience the level of protection they’ve come to expect from US bonds.

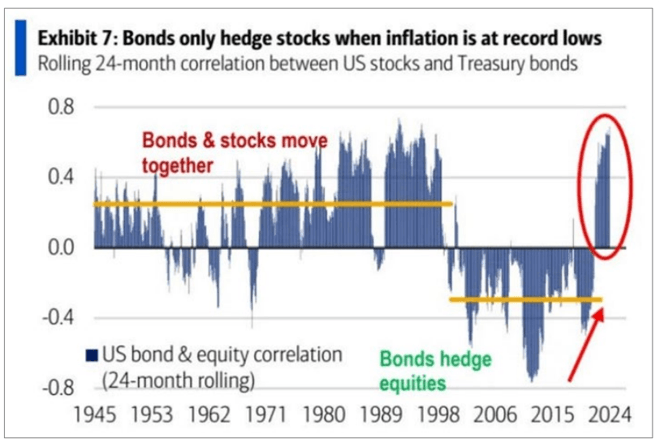

A chart from the Bank of America, spanning back to 1945, shows a 24-month rolling correlation between bonds and stocks. Bonds have only effectively hedged stocks from 2000 to 2021, with a positive correlation between equity and bonds as the longer-term norm.

He explained that while a 60/40 portfolio – 60% in equities (such as the S&P 500) and 40% in long bonds – has historically worked well, 2022 saw a complete reversal of this trend.

“Suddenly, equities and bonds both went down. And it was seen as just this anomaly related to the Ukraine war and issues with supply chains and energy spikes. But if we look deeper, supply shocks (including tariffs, trade wars, and reduced immigration), which we haven’t seen for a while, are exactly what causes the situation where you have slowing growth and increasing income inflation which can cause both equities and bonds to decline.”

He added, “So if we were to see a breakdown of this negative correlation, and moved back toward what we’ve historically seen, it would be quite something for the financial markets to evaluate.”

Final thoughts

Wrapping up, Gilchrist urged investors to diversify globally, noting that integrated portfolio management can help to balance local and offshore investments.

“Obviously, we are cautious about the US. We’re cautious about the large-cap shares in particular given valuations.”

He active management will be crucial going forward. “You are going to (have to) be selective with who you invest with.”

Gilchrist also highlighted opportunities beyond large-cap stocks.

Large-cap companies, typically those with a market capitalisation of $10 billion or more, have historically been a dominant focus.

He said investors need to question whether their manager can exploit opportunities outside of large caps.

Finally, he advised investors to seek true diversification, ensuring they incorporate differentiated managers into their solutions.