Private credit has become one of the cornerstones of finance, as, according to the BIS, private credit funds are managing more than $2.5 trillion today. But the sector is in a major crisis. Private credit funds are suffering withdrawals as the sell-off in SaaS (Software-as-a-Service) assets indicates that investors fear that AI agents and AI-built tools could bypass software products – AKA the SaaS apocalypse.

Business development companies (BDCs) are important private credit investment vehicles, representing about a fifth of the US private credit market, offering investors access to direct lending for smaller and private medium-sized companies. As aptly summarised by Grimes & Company, BDCs are essentially private credit portfolios in a liquid stock wrapper.

BDCs are roiled by the SaaS sell-off because of their significant exposure to the software industry. Market sources indicate that more than a quarter of their portfolios are in vested in software, technology, and related businesses.

Investing in individual BDCs as an investor can be complex. Although the income streams are highly attractive, they come with risks and constraints, such as substantial capital commitments and illiquid lock-up periods. Investing in BDC exchange-traded portfolios alleviates the liquidity risks because the ETFs invest in publicly traded BDCs.

The capitalization-weighted Cliffwater BDC Index (CWBDC), Bloomberg quote (CWBC:IND), which measures the performance of lending-oriented, exchange-traded BDCs, is an excellent benchmark for the industry.

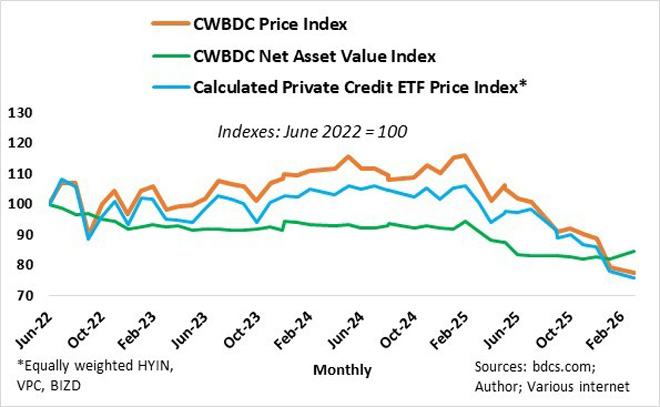

The CWBDC is down 33% compared with a year ago, echoed by a 29% drawdown in an equally weighted Private Equity ETF Index consisting of WisdomTree Private Credit and Alternative Income Fund (HYIN), Virtus Private Credit ETF (VPC), and VanEck BDC Income ETF.

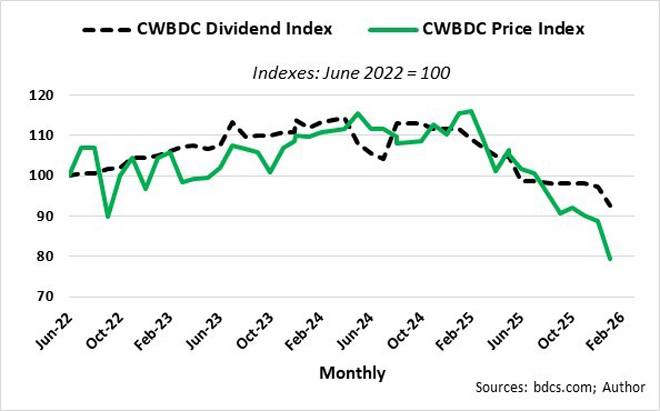

The CWBDC currently offers a dividend yield (trailing 12 months) of 12.25% and is trading at a 23% discount to net asset value (NAV). Many commentators view the current levels as a mispricing of the assets and an opportunity.

My analysis indicates there is more than meets the eye.

From June 2022 to February 2025, the CWBDC’s NAV declined by about 5%, while the price index increased by 16% over the same period. The rot had already set in post-February last year when both the price and the NAV indexes contracted by nearly 12% from February to July.

But what drives the prices?

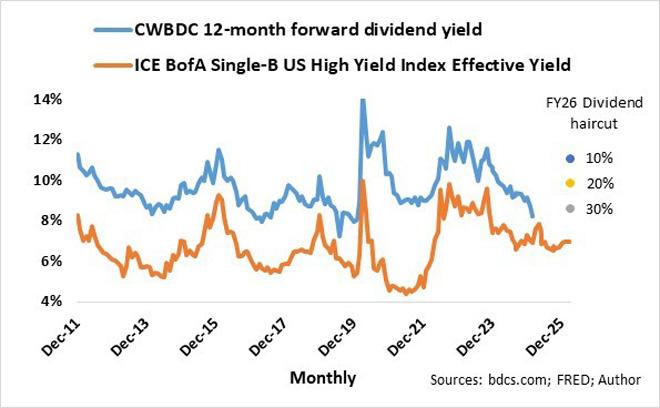

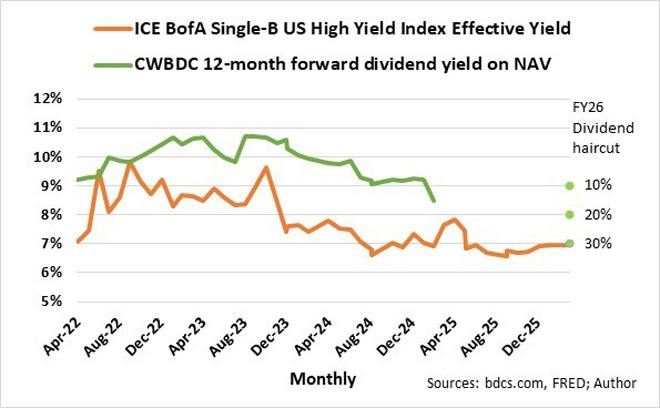

The CWBDC’s 12-month forward dividend yield is highly correlated with the ICE BofA Single-B US High Yield Effective Yield (which tracks the performance of US dollar-denominated corporate debt rated below investment grade), and the spread ranges between 200 and 400 basis points.

It is apparent that up to February last year, the market did not anticipate the 15% cut in dividends in the ensuing 12 months.

With hindsight, at the end of February last year, the yield gap between the CWBDC and the ICE BofA Single-B US High Yield Effective Yield closed to a near record low of 100 basis points.

It is evident that the sell-off in BDCs was not flagging the trouble ahead for the private credit markets but at the time merely reflected the worsening state of the industry via dividend cuts.

Going forward, I doubt any analyst or commentator would attempt to forecast dividends for the industry and specifically for the CWBDC the year ahead. The storm in the private debt markets is raging and ongoing. With that in mind, I assumed three scenarios for haircuts in dividends over the next 12 months for the CWBDC: 10%, 20%, and 30%.

- A 10% cut indicates a forward dividend yield of 11% and a yield gap between the CWBDC and the ICE BofA Single-B US High Yield Effective Yield of about 4% – therefore at the upper end of the historical range and undervalued.

- A 20% cut indicates a forward dividend yield of 10% and a yield gap between the CWBDC and the ICE BofA Single-B US High Yield Effective Yield of about 3% – therefore at the average of the historical range and fair value.

- A 30% cut indicates a forward dividend yield of 9% and a yield gap between the CWBDC and the ICE BofA Single-B US High Yield Effective Yield of about 2% – therefore at the lower end of the historical range and overvalued.

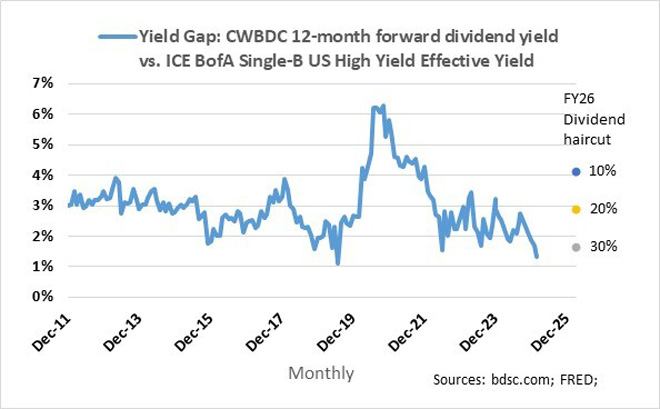

Most concerning to me is the NAV. Despite all that has happened in the private debt markets, such as defaulting on loans, liquidity problems, and possible bankruptcies, the NAV of the CWBDC is virtually unchanged since August last year. Surely, there are probably reasons for the unchanged NAV, but the forward yields raise a red flag for me as potential investor.

Over the past few years, the average yield gap between the 12-month forward dividend yield based on the NAV and the ICE BofA Single-B US High Yield Effective Yield was about 200 basis points.

The three scenarios for divided haircuts over the next 12 months for the CWBDC result in the following yield gap between the 12-month forward dividend yield based on the NAV and the ICE BofA Single-B US High Yield Effective Yield:

- 10% haircut: 200 basis points,

- 20% haircut: 100 basis points, and

- 30% haircut: zero basis points.

It does seem there is room for further downward adjustments in the NAVs of BDCs, specifically after Larry Ellison, chairman and chief technology officer of Oracle Corporation, said during an earnings call recently: “We have these coding tools now that allow us to build a comprehensive set of software, agent-based software to automate a complete ecosystem like healthcare or financial services. That’s why we think we’re a disruptor. That’s why we think the SaaS apocalypse applies to others, but not to us.”

That is why I shy away from BDCs at this stage.

Ryk de Klerk is an independent investment analyst.

Disclaimer: The views expressed in this article are those of the writer and are not necessarily shared by Moonstone Information Refinery or its sister companies. The information in this article does not constitute investment or financial planning advice that is appropriate for every individual’s needs and circumstances.