“It takes money to make money,” as the saying goes, and Sanlam certainly has plenty of it. In its 2024 annual results released last week, the group – the largest non-banking financial services provider on the African continent, with a strong niche presence in Asia – reported yet another year of strong operational performance, highlighted by impressive earnings growth and robust new business.

The numbers paint a picture of resilience. The net result from financial services (NRFFS) increased by 14%, reaching more than R14 billion, with a more significant 25% growth when including a one-off reinsurance recapture fee.

The group’s performance across all business lines was solid, bolstered by higher investment returns on its shareholder capital portfolio and a reduction in corporate project expenses, driving a 24% increase in net operational earnings (or 34% when factoring in the reinsurance recapture fee).

Sanlam’s new business performance also remained strong. Group new business volumes grew by 6%, reaching R420bn, largely driven by solid inflows in the South African asset management business.

Life and general insurance performed well, with life insurance new business volumes increasing by 3% on a present value of new business premiums basis (PVNBP).

Although there was a slight dip in life annuity sales in the latter half of the year, Sanlam noted this was expected given the high base from the previous period and the reduction in bond yields. A large corporate single-premium inflow in the fourth quarter of 2023 was also not repeated.

The group’s net value of new covered business (VNB) increased by 2%, reaching R2.9bn. This was in spite of structural corporate changes, such as the sale of Sanlam Namibia and the termination of the Capitec joint venture, as well as currency depreciations within its Pan Africa portfolio.

Notably, the group achieved a new business margin of 2.81%.

Sanlam’s group equity value per share stands at R81.23, with a return on group equity value (RoGEV) per share of 20.3%, exceeding its target.

The adjusted RoGEV per share of 18% surpassed the group’s hurdle rate of 15.6%, further illustrating its strong financial health.

On the dividend front, Sanlam declared a normal dividend of 445 cents per share, an 11% increase compared to 2023.

The group’s solvency cover ratio remains robust at 168%, comfortably within its target range.

The group’s discretionary capital balance increased to R4.1bn on 31 December 2024 from R2.7bn at 31 December 2023.

According to Sanlam’s integrated report for 2024, this increase is mainly due to the partial sale of the group’s shareholding in Shriram Finance Limited (SFL), the integration of Sanlam Namibia into SanlamAllianz and the reinsurance recapture fee.

In April 2024, Sanlam reduced its stake in Shriram from 10.2% to 9.5% as part of a strategy to reallocate capital, increasing its stakes in Shriram General Insurance Co (SGIC) and Shriram Life Insurance Co (SLIC).

The report further states that discretionary capital was reduced by the outlay associated with the offer to buy out minority shareholders in Sanlam Maroc, as part of the broader SanlamAllianz transaction, acquiring a 25% shareholding in African Rainbow Capital Financial Services Holdings and purchasing 60% in NMS Insurance Services from MultiChoice.

“It is expected that once transactions in progress are completed that discretionary capital will be reduced to be consistent with our long-term target range,” the report stated.

According to Sanlam Group chief executive Paul Hanratty, the formation of SFL and the intermediate companies and structures has had an impact on the dividend.

“We were always very clear that we did expect in the first year or two to have a slowdown of dividend declarations up to the group, and we also said earlier we do expect the benefits of some of the integration to start coming through and that will help to underpin higher growth.”

He added that as some of the structural issues clear, there will be a better dividend flow.

“We will expect both dividend and profits to be positively impacted,” he said.

The power of three

Hanratty attributed the group’s earnings growth, shareholder value creation, and new business to the strength of its three core growth pillars: South Africa, African economies beyond South Africa, and India.

During a webinar on 6 March, Hanratty provided a brief breakdown of how each of these growth engines performed in 2024. He noted that South Africa delivered robust growth and returns.

“The life insurance business produced strong experience variances, improved persistency outcomes in the retail mass segment, and continued to produce excellent margins.”

He also highlighted the positive performance of Santam, which continued to improve its underwriting operations.

Read: Santam’s earnings surge despite troubling weather and vehicle claims

“Santam improved its operations overall, driving premium growth at the same time as improving the quality of the underlying business that’s been written.”

The investment business also showed strong growth, with assets under management continuing to rise, he said.

Hanratty pointed to the newly formed SanlamAllianz joint venture, which delivered results mostly within the guidance ranges provided to the market.

“The competitive position that Sanlam has in most of our markets has put us in a very strong position to generate good returns,” he said.

Turning to the Indian market, Hanratty shared that the business there continued to grow and perform well.

“The credit business grew strongly, and margins were excellent with good credit performance. Insurance businesses continued to grow strongly, although earnings out of India were impacted heavily by the investment and expanded distribution of the life insurer.”

He added, “It’s important to note that it reported earnings for the group. Growth was dampened by the reduction in the Shriram finance stake that we undertook during the course of the year.”

Pan Africa – SanlamAllianz

In 2023, Sanlam and Allianz formed a joint venture, creating the largest insurance group in Africa outside South Africa, offering services in 27 countries.

Read: It’s all systems go for Sanlam and Allianz’s pan-African joint venture

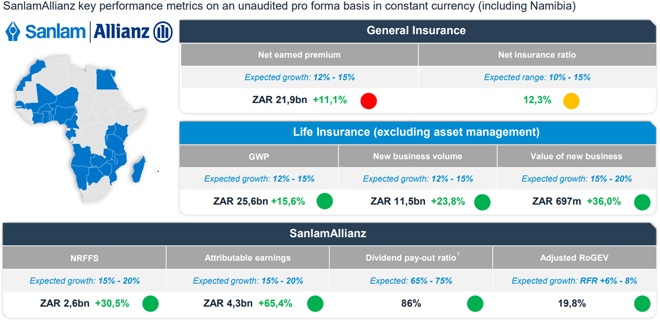

Heinie Werth, chief executive of SanlamAllianz, reported strong progress in 2024, with key integrations completed and financial performance improving: NRFFS rose by 26%, new business grew by 17%, and adjusted RoGEV hit 21.4%.

“Sanlam transferred its Nambian business into the joint venture, and Allianz has decided to exercise their option to increase its shareholding in the joint venture to 49%,” Sanlam stated.

Werth noted SanlamAllianz’s solid start, saying: “Just a reminder to everybody, SanlamAllianz is still a fairly new company. We are now a new group of companies, only 18 months old, and I have to say we’re off to a good start, not only in terms of our numbers, but also in terms of building a foundation for the future.”

The strategy remains focused on building that foundation with three key levers: “grow and optimise the businesses we have”, “support our businesses technically from the centre”, and “active portfolio management”.

He also highlighted the importance of continually reassessing the company’s position, stating, “Are we in the right countries? Are we in the right businesses? Where should we accelerate further expansion through structural growth? Or should we even exit countries where needed?”

For 2025, Werth emphasised focusing on the basics and delivering on budgets. “And again, it’s really just focusing on the basics of the business. It is, firstly, most important, we must deliver on our budgets.”

The company will also focus on integration, rebranding, and investing in culture.

“A big focus is being put on our people, investing in a culture that will help us to build the businesses for the future. It is about our systems. In the long term, we want to standardise and simplify our businesses. That will take quite a period of time, but we are well on our way.”

Maintaining a strong balance sheet will be crucial, he said.

“Quite often, people tend to focus on sales, distribution, and collection of premiums. But in the end, you need to make sure you’ve got an optimal balance sheet. Opportunities to invest in Africa in many markets are limited, and we have to ensure that our balance sheets remain strong and solid to support our businesses.”

On integration, Werth noted the completion of five integrations in 2024, with overlaps in 11 countries. The five countries are Côte d’Ivoire, Senegal, Ghana, Cameroon, and Madagascar.

“We are quite confident that Nigeria should happen in the next month or two,” he said.

In East Africa, approvals are still pending for Tanzania, Mauritius, Uganda, and Kenya.

“We are waiting for our regulatory approvals in these countries,” Werth added.

While the Moroccan integration will take longer, Werth confirmed that the company reached an agreement with authorities earlier in the year and is moving forward. “They accepted our proposals. The hold separate was lifted, and we are now looking at the best ways to execute on these actions.”

Werth concluded that all integrations and rebranding efforts, except perhaps for Morocco, should be completed by year-end.

“Overall, we are on track. In terms of the synergies we promised our shareholders, the integration cost, we are ahead of target, so it’s really coming out the way we planned.”