Membership of Discovery Health Medical Scheme (DHMS) fell by 1.05% between 2023 and 2024, while beneficiaries slipped more sharply, at 1.9%, according to the scheme’s integrated report for the year to the end of December 2024.

At the end of 2024, the scheme counted 1 359 379 principal members, down by 14 485 compared with the end of 2023. The number of beneficiaries declined by 53 038 lives to 2 735 204.

Last year was the second consecutive year in which DHMS experienced a decline in members and beneficiaries. It lost 1 680 members between 2022 and 2023, and 22 750 beneficiaries over the same period. This is in contrast to the increase between 2021 and 2022 – the scheme gained 45 031 members and 52 652 beneficiaries over that period.

DHMS remains the largest open medical scheme in South Africa, with a market share of 58%.

Deon Kotze, the chief commercial officer at Discovery Health, told Moonstone that the loss of members of the KeyCare series of plans was the main reason for the scheme’s overall decline in membership last year.

The three KeyCare plans are entry-level network-based plans, providing hospital cover through designated providers. KeyCare accounted for 12.6% of DHMS’s beneficiaries last year, compared with 13.8% in 2023.

“Excluding KeyCare, the scheme achieved membership growth in 2024. The Smart series – offering high-quality, affordable benefits – grew by more than 17%, and together with the Saver series, now comprises more than 60% of total membership,” Kotze said.

He said the membership base remains stable, with more than 95% of members retaining their plans year-on-year. Notably, 2.89% of members upgraded to higher-tier plans, while 2.23% opted for lower-tier options.

In addition to KeyCare, DHMS offered 15 “main” benefit options in 2024, which were grouped into the following series:

- Executive (one plan). The most expensive plan, providing all-inclusive benefits. Only 0.5% of DHMS beneficiaries belonged to the Executive plan last year – unchanged from 2023.

- Comprehensive (two plans) Like the Executive plan, it offers full private hospital cover. It includes a medical savings account (MSA) and a limited above-threshold benefit (ATB) for day-to-day expenses. The Comprehensive series accounted for 6.7% of beneficiaries in 2024, down from 7.8% in 2023.

- Priority (two plans). A more affordable version of the Comprehensive plans, with limitations on the hospital and day-to-day benefits. As in 2023, the Priority series accounted for 5.6% of beneficiaries.

- Saver (three plans). Unlimited cover at private hospitals. There is no ATB, so once the MSA is depleted, members must pay day-to-day expenses out-of-pocket. The Saver series accounted for 53.2% of the scheme’s beneficiaries, compared to 52.1% in 2023.

- Core (three plans). Unlimited cover at private hospitals, but there is no MSA or day-to-day benefits. The series accounted for 12.9% of the scheme’s beneficiaries in 2024, slightly less than 13% in 2023.

- Smart (two plans). Unlimited hospital cover, but with restrictions to a network of hospitals. There are limited day-to-day benefits, often with co-payments or network requirements. The Smart series’ share of beneficiaries increased from 7.2% to 8.5%.

Shifts across benefit options

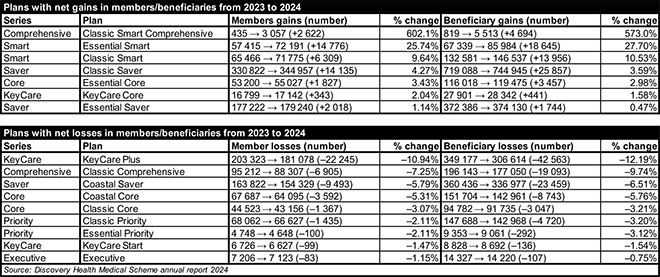

Of the 16 main plans in 2024, seven recorded net member and beneficiary gains, while nine saw declines. Growing plans included Essential Smart, Classic Saver, and Classic Smart. KeyCare Plus and Coastal Saver lost the most lives.

Classic Smart Comprehensive saw a massive increase of 602% members, whereas membership of Classic Comprehensive declined by 7.25%.

Kotze said the growth in Classic Smart Comprehensive was primarily because of the closure of Essential Comprehensive, Essential Delta Comprehensive, and Classic Delta Comprehensive at the end of 2023. “Many of these members selected Classic Smart Comprehensive, given its strong value proposition.”

Essential Delta Comprehensive and Classic Delta Comprehensive were efficiency discounted options. An EDO offers the same level of benefits as a main option, but the contributions are lower because members are restricted to using certain healthcare providers. The inclusion of “Delta” in the name of a DHMS plan indicates it is an EDO.

The decline in Classic Comprehensive was linked to the closure of Classic Delta Comprehensive, which were grouped together in reporting, Kotze said.

Membership of the Smart series plans grew last year – particularly Essential Smart, where membership increased by 26%.

“The growth in the Smart series, and especially Essential Smart, reflects demand for cost-effective, innovative cover. The Smart series, with efficient networks and digitally enabled care, provides quality care, convenience, and affordability,” Kotze said.

In 2025, DHMS added Active Smart to the series – targeting the young professional market. At R1 350 per principal member per month, Discovery Health said Active Smart is the most affordable option in the open medical scheme market.

KeyCare Plus experienced the biggest membership loss (–11%) last year, while KeyCare Start also saw a slight decline in membership.

“In addition to broader economic pressures, the decline in membership reflects several market dynamics – most notably, a reduction in employer subsidies and fewer mandates for medical scheme membership. Increasingly, employers are offering employees a choice between exempted health insurance products and traditional medical schemes,” Kotze said.

“Despite these shifts, KeyCare continues to provide cover to more than 300 000 beneficiaries. This equates to more beneficiaries than most other open medical schemes in South Africa and highlights the sustained demand for affordable medical scheme options and access to private healthcare.”

DHMS has expanded its KeyCare Start Regional plan, which is an EDO, to include additional regions and has introduced a new income band.

Kotze said the KeyCare Start and KeyCare Start Regional plans remain the most affordable within the KeyCare range. “For members outside these network areas, KeyCare Core offers the lowest-cost hospital cover – its growth reflecting strong demand for accessible, lower-cost private healthcare solutions.”

The average age the scheme’s members increased from 37 years to 37.59 years in 2024, and the proportion of pensioner members from 12.32% to 13%. DHMS has an older age profile than the industry average. According to the Council for Medical Schemes’ statistics, the average member age was 34 years in 2023, and the pensioner ratio was 9.4%.

Claims and cost containment measures

DHMS received gross contributions of R94.6 billion (2023: R88.8bn) in 2024.

Net claims increased by 7.48% to R70.5 billion (2023: R65.6bn) last year, with utilisation returning to pre-Covid-19 levels. The gross claims ratio decreased to 90.24% (2023: 92.47%) because the 2023 contribution increases were deferred to April 2023.

Claims accounted for 89.7% (2023: 90.8%) of the scheme’s expenses, while 7.37% (7.41) was spent on administration, 2.52% (2.56%) on managed-care services, and 2.3% (2.4%) on financial adviser and scheme expenses.

Cardiovascular disease accounted for the highest proportion of the scheme’s overall claims cost. It was followed by tumours, musculoskeletal, and gastrointestinal claims. “Mental health disease prevalence has increased in line with other conditions, not relative to them, and has a significant impact on the cost of other existing conditions,” DHMS said.

Michelle Norton, the chairperson of the scheme’s board of trustees, said the impact of chronic disease both on members’ health and the scheme’s financial health are significantly compounded by co-morbid conditions.

“Our data illustrate that a substantial proportion of members are living with more than one chronic condition, with cardiovascular disease, diabetes, cancer, and mental health conditions frequently co-existing. Notably, members with both chronic conditions and mental health disorders experience the highest health needs, with per-life claims costs nearly 3.8 times higher than those without chronic illnesses.

“Similarly, hospital admission rates increase markedly as chronic conditions and mental health disorders accumulate, reaching 3.7 times the rate of members without overlapping chronic conditions,” Norton said in the annual report.

To address rising healthcare costs and improve patient outcomes, she said DHMS has implemented various initiatives focused on efficiency, prevention, and alternative care models.

The scheme is pursuing value-based contracts with healthcare providers, linking payment to patient health outcomes rather than service volume. Additionally, it has implemented co-ordinated care programmes for chronic conditions to enhance efficiency and clinical outcomes.

To improve accessibility and reduce costs, DHMS offers short-stay hospital options, home-care alternatives to hospitalisation, and digital platforms for virtual consultations.

DHMS introduced Virtual Urgent Care at the end of 2023. This benefit has facilitated more than 4 700 urgent virtual consultations by the end of January 2025.

The Hospital at Home programme provides hospital-level treatment at home. The scheme aims to expand its reach.

Recognising the importance of prevention, the scheme introduced Personal Health Pathways, a software application that leverages machine learning and AI to provide personalised health recommendations aimed at reducing disease incidence.

Norton said the scheme’s Mental Healthcare Programme and Depression Risk Reduction Programme have demonstrated their effectiveness: members enrolled in the Mental Healthcare Programme have 24% lower hospital admissions than members not on the programme. Members using the internet-based Cognitive Behavioural Therapy programme have shown significant clinical improvement.

Financial performance

For the year, DHMS delivered a negative insurance service result, before accounting for amounts attributable to future members (reserves), of R350 million (2023: negative R2.252bn). The scheme generated investment income of R2.828bn (2023: R2.418bn). The total comprehensive income for the year, including investment income and realised gains on investments, before reserves, was R2.896bn (2023: loss of R183m).

Insurance liability to future members increased to R31.6bn (2023: R28.7bn), taking the solvency level to 31.01% (2023: 30.6%), exceeding the 25% required by the Medical Schemes Act.

The scheme received a AAA credit rating for the 25th consecutive year from Global Credit Rating Company. This is the highest possible rating for medical schemes.

“The board of trustees believe that, despite challenging market conditions characterised by difficult economic conditions impacting the growth of schemes, the scheme ended 2024 in a strong financial position and remains well placed to meet members’ needs for the foreseeable future,” the report said.