More than one in four of South Africa’s municipalities have been targeted by National Treasury’s decision to begin temporarily withholding their July 2026 Local Government Equitable Share (LGES) transfers. The 69 affected municipalities collectively owe R27.4 billion to Eskom, water boards, the South African Revenue Service, retirement funds, and other creditors.

A Moonstone analysis of Treasury’s accompanying debt schedule – which relates only to the municipalities affected by the intervention and excludes debts owed by municipalities that continue to receive their allocations – shows that just 10 municipalities account for nearly 79% of those arrears, with Matjhabeng Local Municipality (pictured) alone owing more than R9.5bn to a water board.

National Treasury announced on 7 July that it is withholding the July 2026 LGES transfers to the affected municipalities in terms of section 216(2) of the Constitution and section 38 of the Municipal Finance Management Act (MFMA).

Treasury described the move as a corrective measure to strengthen fiscal discipline and improve accountability, rather than a punitive one. It also notes that municipalities were notified in advance and given an opportunity to explain why their allocations should not be withheld before the decision was taken.

Among the key requirements is that municipalities must reduce their unauthorised, irregular, fruitless, and wasteful expenditure (UIFWE) balances by at least 25% against the position at 30 June 2026, measured by 30 September 2026, alongside a range of governance and financial management reforms.

The LGES is an unconditional allocation from nationally raised revenue that helps municipalities to fund basic services and their institutional responsibilities.

Treasury said it does not expect the temporary withholding to affect service delivery.

In a media statement issued on 7 July, the Portfolio Committee on Co-operative Governance and Traditional Affairs (COGTA) said it welcomed the intent behind National Treasury’s announcement.

The committee noted that equitable share transfers are critical to supporting municipalities in delivering basic services to communities. It urged affected municipalities urgently to comply with the conditions set by Treasury so that funds can be released and not translate into further hardship for communities.

COGTA’s chairperson, Dr Zweli Mkhize, said it is imperative that councillors and municipal managers feel the consequences of bad administration “because poor performance directly affects communities”.

“Action must now be directed at leaders who mismanage positions of responsibility by allowing financial and procurement irregularities to continue,” he said.

Debt concentrated in just 10 municipalities

The debt schedule accompanying Treasury’s media statement lists the municipalities affected by the withholding of their LGES allocations and details their outstanding debts to key creditors, using balances as at 30 April 2026 for most categories and 31 March 2026 for Eskom and water boards. The accompanying annexure sets out the conditions for the release of the withheld funds.

Moonstone’s analysis is limited to the 69 municipalities – just over a quarter of South Africa’s 257 municipalities – whose July 2026 LGES transfers have been temporarily withheld and does not include debts owed by municipalities that continue to receive their allocations.

An analysis found that just 10 municipalities account for more than R21.6bn of the R27.4bn reflected in Treasury’s schedule – nearly 79% of the total debt recorded for the municipalities affected by the intervention.

Matjhabeng’s position at the top of the list is unlikely to surprise Parliament’s Portfolio Committee on Water and Sanitation. Matjhabeng Local Municipality is in the Free State, within the Lejweleputswa District Municipality. Its administrative seat is Welkom, and it also includes the towns of Virginia, Odendaalsrus, Allanridge, Hennenman and Ventersburg.

In March, the committee described the municipality’s then nearly R9bn debt to the Vaal Central Water Board as “the worst recalcitrant behaviour” it had encountered and questioned whether the municipality was capable of honouring a repayment agreement. Treasury’s latest debt schedule places that figure at more than R9.5bn.

Not all municipalities on Treasury’s list appear because of outstanding creditor balances. For example, Theewaterskloof, Laingsburg, and Beaufort West in the Western Cape are included despite no monetary arrears being reflected in the accompanying debt schedule, showing that Treasury also assessed municipalities against governance, financial management, and compliance criteria, including UIFWE management, consequence management, and unfunded budgets.

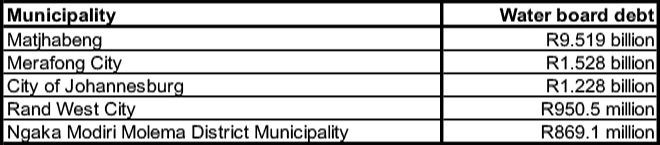

Water boards are the largest creditors

Water boards are the largest creditor category in Treasury’s debt schedule, with the affected municipalities owing them R15.7bn – more than half of the R27.4bn reflected in the analysis.

Matjhabeng alone accounts for more than R9.5bn of the R15.7bn owed to water boards by the municipalities included in Treasury’s intervention.

Almost all the recorded debt of Merafong City and Rand West City is owed to their respective water boards.

Johannesburg owes more than R1.2bn to a water board in addition to its substantial Eskom arrears.

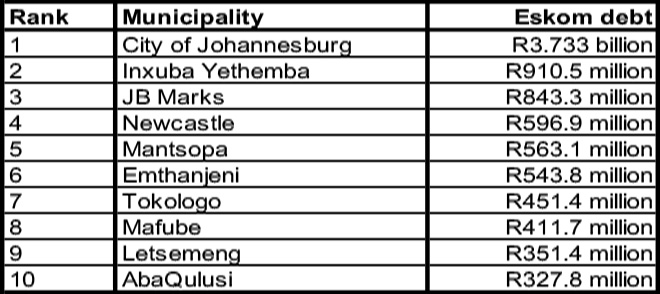

Johannesburg tops Eskom debt list

Eskom is the second-largest creditor in Treasury’s debt schedule, with the affected municipalities collectively owing the power utility almost R9.7bn.

The City of Johannesburg accounts for the largest share of that debt, with Eskom arrears of R3.733bn. It is followed by Inxuba Yethemba, JB Marks, and Newcastle.

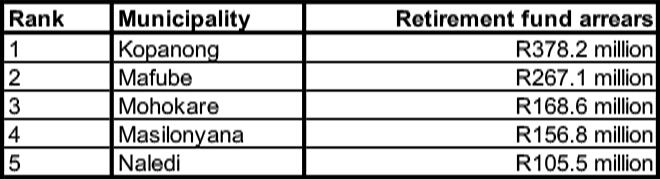

Retirement fund arrears top R1.4bn

After water boards and Eskom, retirement funds are the third-largest creditor category reflected in National Treasury’s debt schedule. The 69 municipalities collectively owe R1.429bn in unpaid retirement fund contributions.

Unpaid retirement fund contributions involve money deducted from employees’ salaries but not paid over to their retirement funds.

Together, these five municipalities account for just over R1.07bn, or just over 75%, of the retirement fund arrears reflected in Treasury’s debt schedule. Four of the five largest municipal retirement fund debtors are in the Free State, with Naledi in North West ranking fifth.

As Moonstone recently reported, the FSCA estimates total retirement fund arrears across all sectors at R8.33bn, despite recoveries of more than R1bn since it began publicly naming defaulting employers in 2023.

Read: Retirement fund arrears rise to R8.33bn despite R1bn in recoveries

The R1.429bn reflected in Treasury’s debt schedule relates only to the municipalities affected by the latest equitable share intervention and should not be confused with the Financial Sector Conduct Authority’s broader estimate, which covers employers across the economy.

The FSCA has identified municipal retirement fund arrears as an area of particular concern and has credited Treasury’s withholding of equitable share allocations from persistently non-compliant municipalities with improving payment behaviour in parts of the local government sector.

The debt extends beyond utilities and retirement funds. Collectively, the 69 municipalities also owe about R412.5 million to SARS and R143m to the Auditor-General of South Africa (AGSA), according to Treasury’s debt schedule.

Why Treasury intervened

The debt reflected in Treasury’s schedule is only one of the reasons National Treasury decided to temporarily withhold the July 2026 LGES transfers.

According to Treasury, the decision follows years of persistent and serious non-compliance with the MFMA, despite repeated guidance, engagement, and training aimed at improving municipal financial management.

Among the concerns identified by Treasury are municipalities that continue to adopt unfunded budgets, fail to investigate or process UIFWE as required by law, neglect to implement consequence management, and fall behind on statutory obligations, including payments to Eskom, water boards, and statutory bodies such as SARS, the AGSA, and the FSCA.

The emphasis on governance and accountability reflects concerns repeatedly raised by oversight bodies. Earlier this year, COGTA and the Standing Committee on Public Accounts (SCOPA) conducted a joint oversight visit to municipalities identified by the AGSA as distressed or dysfunctional after the 2023/24 local government audit outcomes showed that only 41 municipalities achieved clean audits, while 40 regressed and 13 failed to submit financial statements on time.

The concerns raised during those visits were reflected in AGSA’s latest Consolidated General Report on Local Government Audit Outcomes, which records R145.2bn in irregular expenditure incurred by municipalities since the 2021/22 financial year, including R40.1bn during 2024/25. Over the same period, municipalities disclosed R118.1bn in unauthorised expenditure and R24.1bn in fruitless and wasteful expenditure.

The report also found that 116 municipalities adopted unfunded budgets during 2024/25, up from 113 the previous year. By year-end, municipalities owed R3.4bn in interest to Eskom and R1.2bn in interest to water boards, while 48 municipalities had third-party deductions that had remained unpaid for more than a month.

The joint oversight visits were followed by a series of public committee hearings at which affected municipalities, provincial governments, and oversight institutions were required to account for poor audit outcomes, governance failures, and the implementation of corrective measures.

Read: SIU findings expose widening municipal governance failures

Responding to National Treasury’s decision, Mkhize said the withholding of funds confirmed the seriousness of the problems identified during the committee’s oversight work.

“All municipalities must realise that things cannot continue as usual when governance and financial prescripts are undermined,” Mkhize said.

Treasury’s latest intervention reflects a broader shift in its approach to failing municipalities. At the PSG Financial Services Annual Conference in May, Treasury Director-General Duncan Pieterse warned that municipal dysfunction had become one of the biggest threats to South Africa’s reform agenda, undermining economic growth, service delivery, and the financial sustainability of entities such as Eskom.

He indicated that municipalities unable to reform could increasingly lose operational control of key services, with stronger intervention becoming more likely.

Read: Treasury signals harder line on failing municipalities

What municipalities must do

The withholding of the LGES transfers is temporary, but municipalities will have to satisfy a series of conditions before the funds are released.

A key requirement is that municipalities reduce their UIFWE balances by at least 25% during the first quarter of the 2026/27 municipal financial year. Treasury also requires evidence that these reductions are supported by legally compliant investigations, council resolutions, and the documentation prescribed by the MFMA.

Municipalities must also demonstrate that lawfully appointed disciplinary boards are active and functioning, that allegations of financial misconduct have been referred for investigation, and that disciplinary, civil recovery and criminal processes have been initiated where appropriate.

Municipalities with outstanding debts to Eskom, water boards, retirement funds, and other third parties identified by Treasury must conclude signed repayment agreements with those creditors. Treasury says it will initially release only an amount equivalent to the agreed payment and will release the remaining balance only once municipalities provide evidence that the funds were used for the intended purpose.

Finally, municipalities that adopted unfunded adjustment budgets during the 2025/26 financial year must provide written commitments that they will not adopt unfunded budgets in future.

Treasury says the withheld allocations will be released only once municipalities have demonstrated that they have met the required conditions. In the case of outstanding debts, municipalities will also have to provide evidence that funds already released were used for their intended purpose before the balance of the allocation is paid.