The Financial Intelligence Centre (FIC) has issued final guidance on how specified accountable institutions must complete and submit the 2026 Risk and Compliance Return (RCR) under Directive 11 of 2026, while confirming that the underlying reporting framework and filing deadlines remain largely unchanged from the draft guidance published in March.

Public Compliance Communication (PCC) 60 was issued on 12 June 2026 as the final version of Draft PCC 125, following a consultation period that ran from 31 March to 24 April 2026.

Directive 11 requires specified accountable institutions to submit the 2026 RCR to the FIC. PCC 60 is the FIC’s final guidance on the format and manner of completing and submitting those returns.

The guidance states that returns must be completed based on an institution’s understanding of its money-laundering, terrorist-financing, and proliferation-financing risks, and the risk-based controls it has implemented in terms of the Financial Intelligence Centre Act (FICA).

The FIC says consultation comments were received from a range of stakeholders, including industry associations, estate agents, legal practitioners, and crypto asset service providers (CASPs).

The Consultation Feedback Note indicates that the final guidance incorporated comments where appropriate. However, PCC 60 leaves the overall reporting framework unchanged.

PCC 60 also makes clear that FIC guidance is “authoritative in nature” and must be considered when interpreting FICA and assessing compliance with obligations imposed under it. The document states that enforcement action may arise where an accountable institution has not complied with the Act in areas covered by the Centre’s guidance, unless the institution can demonstrate that it complied with the relevant obligation in an equivalent manner.

Directive 11 applies to the following accountable institutions listed in Schedule 1 to FICA:

- Item 1 – Legal practitioners

- Item 2 – Trust and company service providers

- Item 3 – Estate agents

- Item 9 – Gambling institutions

- Item 11 – Credit providers (excluding banks, mutual banks, and co-operative banks acting as credit providers)

- Item 14 – South African Postbank Limited

- Item 20 – Dealers in high-value goods

- Item 21 – South African Mint Company (limited scope)

- Item 22 – CASPs

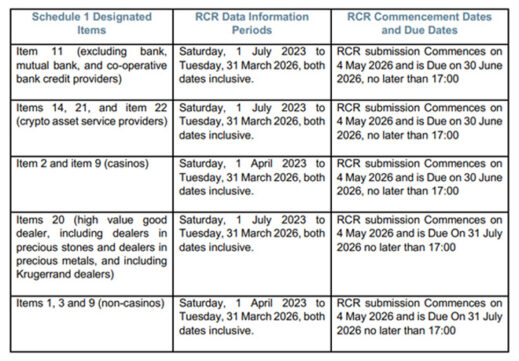

The 2026 RCR must be completed across three distinct reporting years or periods, depending on the Schedule 1 category into which the accountable institution falls.

For institutions falling under items 1, 2, 3, and 9, the return must cover three separate years: 1 April 2023 to 31 March 2024, 1 April 2024 to 31 March 2025, and 1 April 2025 to 31 March 2026.

For institutions falling under items 11, 14, 20, 21, and 22, the return must cover three separate periods: 1 July 2023 to 31 March 2024, 1 April 2024 to 31 March 2025, and 1 April 2025 to 31 March 2026.

PCC 60 states that the return may be submitted only once the institution has completed the required information for all three applicable years or periods.

The guidance reiterates that a separate 2026 RCR must be submitted in respect of each accountable institution, and that each submission must reflect that institution’s unique organisation identity number (Org ID).

Only institutions that have successfully registered with the Centre on the goAML registration and reporting platform and have obtained an Org ID may submit an RCR online.

PCC 60 further states that only one RCR submission is permitted for each Org ID, regardless of the number of branches or subsidiaries associated with that institution.

Institutions operating through branch networks are generally required to submit a single consolidated return covering the activities of head office and all branches on an enterprise-wide basis. PCC 60 explains, however, that where a branch office is structured as a separate legal entity, that entity constitutes a separate accountable institution in its own right, must register separately with the Centre, and must submit its own RCR.

The guidance also states that franchise networks made up of separate legal entities are not treated as branch networks, and each franchisee must register separately and submit its own return.

The final guidance also repeats an important point for institutions that conduct more than one designated activity under Schedule 1. Where an institution operates across more than one Schedule 1 item, it must submit a separate 2026 RCR for each designated business activity and the associated Org ID.

PCC 60 illustrates this with the example of a legal practitioner that is registered under item 1 for legal services but also provides trust services and company services under item 2. In that scenario, the practitioner may hold multiple goAML registration profiles and multiple Org ID numbers and would be required to submit a separate RCR for each of those designated activities.

Clarification for newly registered and newly operating institutions

One of the clarifications added after consultation concerns accountable institutions that registered late with the FIC or commenced business only partway through the reporting cycle.

The Consultation Feedback Note records that commentators questioned whether newly registered or newly operating institutions would be expected to provide information covering the entire three-year reporting period. It states that the Centre responded by adding an example to the final guidance.

PCC 60 explains that where an accountable institution registers with the Centre only in the final reporting year, but it had already commenced business during earlier years, it must still submit the return for all years during which the business was open and required to be registered. By contrast, where an institution both opens its business and registers with the Centre only in the final reporting year, it need submit the return only for that final year.

The guidance cautions institutions against falsely omitting years of registration or years during which the business was open, and it states that information submitted during the RCR process may be subject to inspection.

Another express clarification in PCC 60 is that third-party service providers may not submit the 2026 RCR on behalf of an accountable institution. The guidance states that the compliance officer, assisted by the compliance function, must submit the RCR, while ultimate responsibility for compliance remains with the board of directors, senior manager, or the person with the highest authority in the institution.

It also states that users must access the RCR platform using their existing goAML credentials and notes that the sharing of user credentials is prohibited under Directive 2 of 2014.

Submission process

PCC 60 urges institutions to download and review the sample RCR questionnaire in advance, gather and collate the required information for each reporting year or period, and prepare draft responses before completing the online return.

The guidance recommends that institutions work through the data period by period and proceed to complete the online form only once the necessary information has been prepared. It also states that the data may be saved during completion, allowing the questionnaire to be completed over multiple sessions if necessary.

Once submitted, however, the 2026 RCR cannot be changed on goAML. PCC 60 states that returns may not be retracted or withdrawn after submission. Where an accountable institution discovers that it has submitted an incorrect return, it must submit a written compliance query to the Centre through the FIC’s compliance query channel.

Click here to visit the FIC’s RCR page.

The guidance emphasises that accountable institutions remain responsible for ensuring that the information submitted is adequate, accurate, and complete before final submission.

Directive 11 states that a specified accountable institution that fails to comply with the Directive is non-compliant and is subject to an administrative sanction in accordance with section 62E of FICA. PCC 60 similarly warns that non-compliance with Directive 11 may result in administrative sanctions being applied by the Centre.

2026 RCR deadlines

With consultation now concluded and PCC 60 in force, the immediate focus for affected institutions is compliance with the submission timetable, as set out in Directive 11.

- Returns are due by 5pm on 30 June 2026 for institutions classified under items 2, 9 (casinos), 11 (excluding banks, mutual banks and co-operative bank credit providers), 14, 21, and 22.

- Returns are due by 5pm on 31 July 2026 for institutions classified under items 1, 3, 9 (non-casinos), and 20.