The demarcation between health insurance and medical schemes has a long history, going back as far as 2000 after the enactment of the Medical Schemes Act no. 131 of 1998.

The basis of the demarcation debate was the fact that certain health insurance products were deemed to infringe on and compete unfairly with medical schemes, without being subject to the same regulatory requirements.

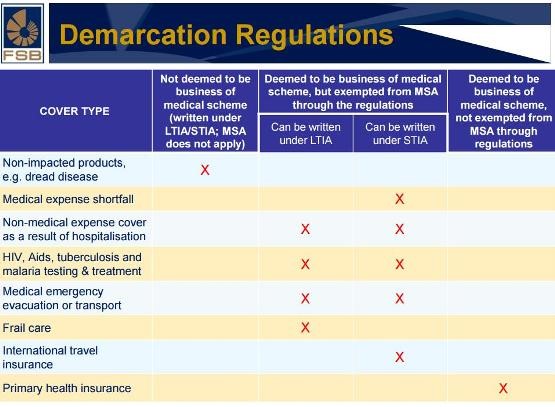

This culminated into various versions of draft regulations for health insurance products to ensure a clearer role of each product while remaining competitive and educating consumers on the complementary role of such products in their health portfolio.

The final Demarcation Regulations (DR) was signed into law on 23 December 2016, with all new policies having to comply from 1 April 2017. Existing policies have to comply after 1 January 2018.

What about Gap Cover?

As far as Gap Cover, as a Short-term Health Insurance product goes, the new regulations confirmed that this product is still necessary and will remain, albeit with a few changes.

The ever increasing cost of services provided by medical professionals, along with the fact that the cost of such services are to date unregulated, caused medical scheme members to experience an increasing “self-payment” shortfall of medical expenses. These out-of-pocket costs occur as medical schemes implement more and more restrictive practices such as doctors’ networks and managed care to ensure containment of benefits paid for services delivered. A Gap Cover policy addresses the resultant shortfalls.

The increased use of co-payments, charged by medical schemes as a condition for payment/delivery of pre-determined services to members, has further increased the burden of personal expenses of members. These co-payments can be insured via a Co-payment benefit, allowing for cover of an insured event at a defined cost.

What are the changes affecting Gap Cover policies?

The three most significant changes brought about by the new demarcation regulations are:

- Maximum Benefit Capped

The capping of the aggregated benefit at R150 000 per beneficiary per annum should not be deemed as restrictive at all, especially given the historical claims for Gap Cover products in the market. The defined benefit is in fact in the interest of the member, and more specifically aimed at “containing” excessive charges by medical professionals for services rendered.The “per beneficiary” approach vs a “per policy” approach furthermore aligns much better with the known benefit structure and practices of medical schemes. Collective benefits of a four member family are therefore more realistic and practical than previously quoted “uncapped” benefit levels by some providers in the market.

Capping the annual benefit level at R150 000 furthermore equalises the playing field for Gap Cover providers in the interest of the consumer. Price and access becomes a key differentiator.

- No discrimination based on age

In line with the requirement that medical schemes were obliged not to discriminate on the basis of age, Gap Cover policies now also have to subscribe to open enrolment for all age groups to support the objective of social solidarity. - Underwriting Gap Cover contracts as group

Another Demarcation Regulation change is differentiated pricing on a “per group” basis, which allow for open enrolment and avoids anti-selective practices in the market.

Underwriting Gap Cover contracts for Groups

No provider of Gap Cover can decline an applicant, irrespective of age, BUT is allowed to charge a higher premium for new applicants above a certain age. The regulations allow for differentiated pricing i.e. a more expensive premium for the same benefits based on the age of an applicant. The condition for the above is that it applies to all applicants over a specific age and NOT any one individual.

Prescribed Minimum Benefits

A burning issue for complementary health cover products have always been the implications of covering PMBs (prescribed minimum benefits). With the new regulations, Gap Cover insurers will only cover the difference between total costs of a relevant health service and the amount a person’s medical scheme has paid. The intent of the regulations is clearly to ensure PMBs are covered by Medical Schemes and not by Gap Cover products.

In addition to this, costs or expenses that are not covered by a medical scheme may not be covered by health insurance policies.

In summary, Optivest supports the above changes in the regulations and see more opportunity for relevant health advice to members of medical schemes in the market.

Member education and relevant advice on their health portfolio becomes ever more important in the financial planning process.

For more information, mail to contact@optivest.co.za or visit www.optivest.co.za.

Article written by: By: Marcel du Toit, CEO Optivest Health Solutions