Suicide-related insurance claims surged by 62% in 2024 compared with the average over the previous five years, according to new data from Discovery Life.

During a recent webinar exploring the company’s 2024 claims experience, Discovery shone a stark spotlight on South Africa’s worsening mental health crisis.

In 2024, Discovery Life paid out a total of R9.1 billion in claims across group risk and individual life policies. Life cover remained the most significant component, with payouts reaching more than R3.4bn. This was followed by the severe illness benefit, which totalled R1.54bn, and the capital disability benefit at R933 million. The income continuation benefit saw R673m in claims, while the health plan protector paid out R133m.

Other benefits, such as the global education protector and the funeral benefit, accounted for R67m and R31m, respectively. Overhead expense benefits also amounted to R31m.

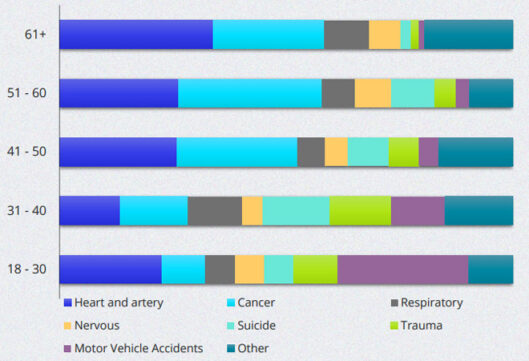

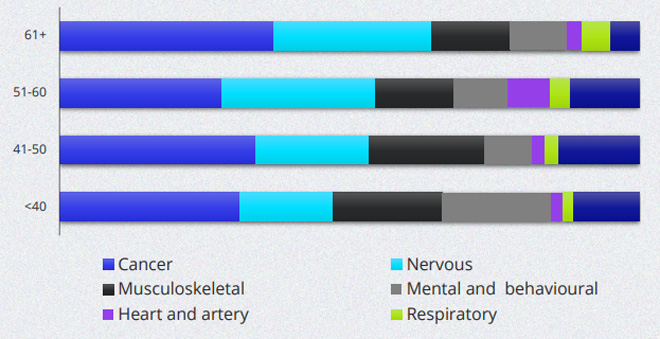

An analysis of life cover claims across age groups showed distinct health trends. Among policyholders aged 61 and older, heart- and artery-related conditions were the most common cause of claims, accounting for 34% of the total.

For those in their 50s, cancer was the leading cause, responsible for 32% of claims. The same was true for clients in their 40s, where cancer accounted for 27% of claims, and among those aged 31 to 40, cancer made up 15%.

In contrast, motor vehicle accidents were the most prevalent cause of life cover claims among those aged 18 to 30, making up 29% of this group’s claims.

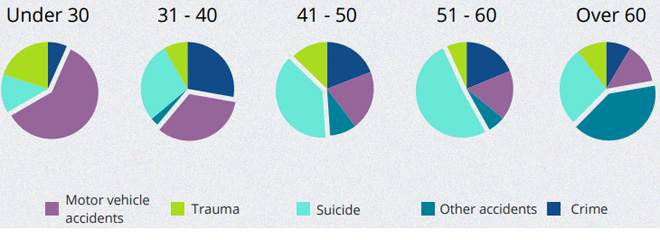

Concerningly, one in five death claims were due to unnatural causes. Suicide was the leading cause, accounting for 35% of these claims – well ahead of motor vehicle accidents (23%), crime (17%), other accidents (15%), and trauma (10%).

The trend was particularly pronounced among policyholders aged 41 to 60, where suicide made up nearly half (45%) of all unnatural death claims.

Dr Maritha van der Walt, the chief medical officer at Discovery Life, described the findings as “very sad and concerning”. She said most claimants were older men, although the youngest was a 35-year-old woman – a medical professional with underlying psychiatric conditions.

“Sixty-three percent of the claimants were registered on DHMS (Discovery Health Medical Scheme) for depression, anxiety, bipolar, mood disorders, and so on,” she said.

Van der Walt explained that in some cases, additional health issues appeared to play a role in the tragic outcome. These included conditions such as intractable pain, late-stage cancer, and chronic neurological disorders.

She added that although some contributing factors may be difficult to track, financial stress was likely a significant influence – particularly among older individuals.

“It could be the aftermath of Covid where people lost jobs and income and livelihood and so on, and, of course, family members, but financial reasons seem to play a role in the older age group, and that is, of course, very difficult to address,” she said.

Van der Walt said these numbers reflect real lives lost, and families left behind in grief.

“We must remember that it is a treatable condition. Depression is totally treatable. There are many medications on the market, but it’s got to be a holistic approach with psychological support, maybe occupational therapy and social support, and so on.”

She said it was crucial to remove the stigma around mental illness and ensure people are directed to the right support.

“What is interesting on the pharmacological fields is that there is now the concept of pharmacogenomics where blood tests can be done on a patient, and that can give us an indication of which antidepressant will work better, so that will be a more individualised choice and hopefully more effective in a much shorter time.”

Gareth Friedlander, the deputy chief executive of Discovery Life, said there is an opportunity to improve early detection and intervention by integrating financial and medical data.

“It will take time for us to really understand that with credibility, but certainly, the amount of data coming through [a] bank that can then be overlaid onto all of the other health and wellness- and medical claims-related data is going to be a powerful, hopefully, predictor of risk in the mental wellness space that will help us with earlier detection and intervention.”

Another notable statistic from Discovery’s claims data showed that among policyholders under the age of 30, 60% of unnatural death claims were the result of motor vehicle accidents.

Cancer’s rising toll – why screening is critical

Cancer was the highest cause of death for women, the most common severe illness for both women and men, and the most common cause of disability among both women and men.

Melanoma has emerged as the third-highest contributor to claim payouts under Discovery Life’s severe illness benefit, highlighting the increasing impact of skin cancer across the population.

Sylvia Steyn, the head of claims and servicing at Discovery Life, said melanoma affects people of all ages – including teenagers and those in their early 20s – and occurs in both men and women. Early diagnosis is critical, she emphasised, which is why Discovery’s early cancer benefit includes cover for melanoma in situ (Stage 0 cancer).

“That means it’s there, but it’s not invading the underlying tissues, and that means that it is curable,” she explained.

Van der Walt urged individuals to monitor skin changes closely.

“Any mole that is changing – in size, in edge, in colour – or bleeding, any kind of change or immune skin lesion, please have it looked at so that we can rather diagnose and treat at an early stage.”

While the prognosis for Stage 3 and 4 malignant melanomas – particularly those with brain metastases – was once bleak, she noted that immunotherapy has transformed the outlook.

“A good percentage of these cancers, unfortunately not 100%, but many people will have a very positive response to immunotherapy, and the outlook is very much better than before.”

However, these treatments come at a high cost, with a single treatment cycle potentially exceeding R1m.

Cancer is a Prescribed Minimum Benefit, but because of the high treatment costs, there will be co-payments, which is why the severe illness benefit is necessary.

She added that melanoma is also known for its “long tail” – the possibility of recurrence years after the initial diagnosis. “And that is why you need a cancer benefit among your severe illness that will cover your relapses as well.”

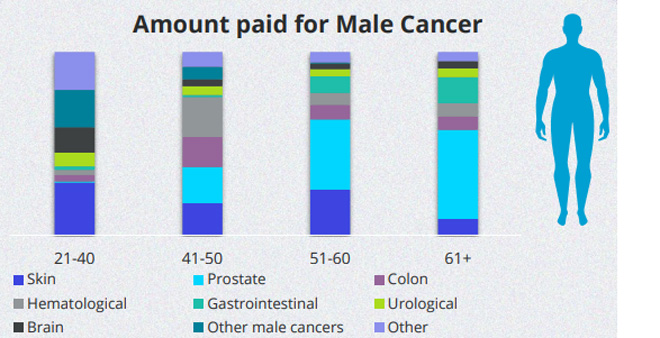

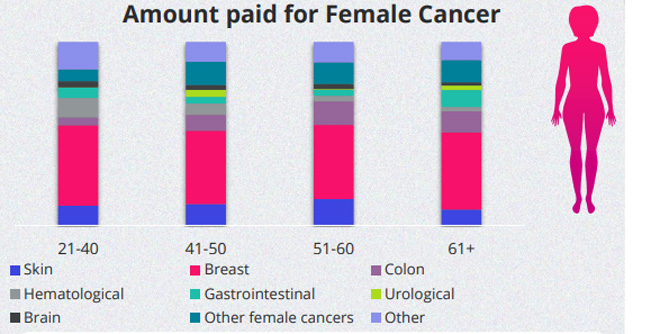

A closer look at the severe illness benefit, particularly cancer-related claims, offers further insight into gender-specific risks.

Among men, prostate cancer was the most common diagnosis, representing 35% of male cancer claims.

For women, breast cancer was the most prevalent, making up 41% of cancer claims.

Steyn highlighted that beyond its high prevalence, what stood out about breast cancer was its occurrence across all age groups – from very young individuals to those over 60. “Which just brings home the importance of early screening,” she said.

The Discovery Group invests significantly in encouraging and supporting clients to carry out regular health screening. Compared to 2020, the 2024 data show significant increases in screening for common cancers, with mammograms up 14%, colorectal cancer screening 29% higher and 19% more prostate exams.

Thanks to the increase in screening rates, there has been a 62% increase in early-stage cancer claims compared to 2020’s claims on illness cover.

“As a proportion of all cancer claims, lower severity claims continue to have an upward trajectory, showing that these cancers continue to be detected earlier. While Stage 3 and 4 cancers have remained relatively stable over that time, it’s in the disability claims for Stage 4 cancers where we’re seeing incredible benefits of screening, with those claims dropping 16% since last year,” said Van der Walt.

Capital disability benefit

Cancer was the leading cause of disability claims across all age groups in 2024, according to Discovery Life’s claims data, with nervous system conditions such as strokes ranking second. The figures confirm the wide-reaching impact of cancer on working-age individuals and the importance of robust disability cover.

Discovery Life’s 2024 claims data under its Income Continuation Benefit further highlighted the growing need for long-term income protection. A total of R673m was paid out during the year, with a projected R3.4bn still expected to be paid to existing claimants.

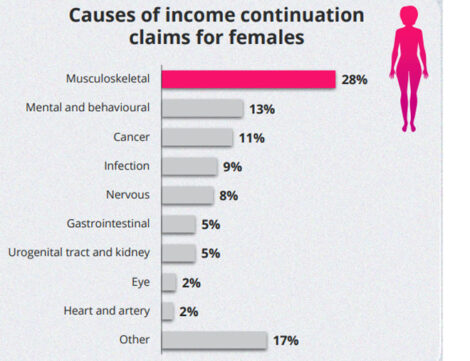

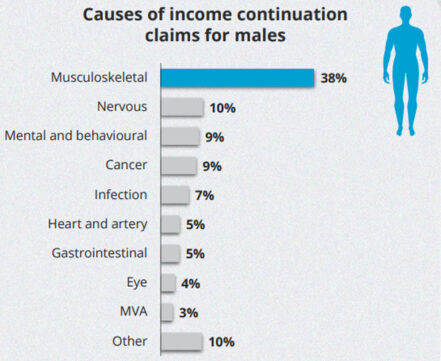

Musculoskeletal conditions were the most common reason for income protection claims, accounting for 28% of claims by women and 38% by men. These conditions include back, joint, and muscular disorders.

Notably, 30% of Discovery’s claimants were classified as permanently disabled, making up 71% of the total payout value. This highlights the financial strain that long-term disability can place on individuals and the crucial role of sustained income support.

A breakdown of claimants by age further illustrates how the likelihood of permanent disability rises over time:

- Ages 30 and under: 81% temporary, 19% permanent

- Ages 31 to 40: 75% temporary, 25% permanent

- Ages 41 to 50: 66% temporary, 34% permanent

- Ages 51 to 60: 63% temporary, 37% permanent

- Over 60: 76% temporary, 24% permanent

Discovery Life paid out R128 million in Converted Severe Illness claims – benefits that kick in when a client’s disability cover expires and automatically converts to illness cover, providing continued protection later in life.

Friedlander underscored the importance of this feature. “Illness cover and features like our automatic disability benefit conversion are crucial to ensuring clients have illness protection at older ages.

“This is very relevant, considering that 28% of severe illness claims are made by clients over 60. Ten years ago, this age group accounted for 11% of our illness claims and five years ago it was 20%.”

He acknowledged that it’s natural for claims to rise as clients age, but said the pace of the increase is faster than expected – reinforcing the need to secure illness cover early.

“Cover that isn’t always accessible or financially viable at those ages, so it is crucial to get this form of cover when you’re young,” notes Friedlander.

I lost my dear friend Johan in Jan 2025 to suicide age 68. We worked together for 18years. I myself age 57 have considered the option after like Johan we are let down by weak leadership in the respective corporates we served for so many years. We are discarded like unwanted dogs after serving our employees for most of our lives. It is OK writing these articles, what I do not see is any action or changes in behaviour.