“Naught for your comfort” is an apt summary of Budget 2.0 for the average taxpayer and consumer.

Instead of a two-percentage-point increase in the VAT rate this year, as proposed by the Budget withdrawn on 19 February, the government wants to increase the rate of VAT by 0.5 percentage points each year over two fiscal years. This will result in the VAT rate reaching 16% in 2026/27.

The first VAT increase will take effect on 1 May this year and the second on 1 April 2026.

As in Budget 1.0, the basket of VAT zero-rated food items – currently, 21 items – will be expanded in an attempt to mitigate the impact of the rate hikes on lower-income households.

From 1 May, the revised basket of zero-rated items will also include tinned or canned vegetables, dairy liquid blends, and a variety of meat products (sheep, poultry, goat, and swine).

According to National Treasury’s Budget Review, the government will raise R13.5 billion from the VAT increase in 2025/26, although it will “forfeit” R2bn as a result of zero-rating the additional items.

Interestingly, when he delivered his Budget Speech on Wednesday afternoon, Finance Minister Enoch Godongwana deviated from the printed copy of the speech, which was handed out to the media a few hours earlier.

When delivering the speech, he inserted the following immediately after announcing the two proposed VAT hikes: “Should the spending reduce and other measures we’re embarking on yield enough extra revenue, we will re-assess the need to embark on the second half-a-percent-point increase to VAT.”

Not only is this addition not in the printed version, but the Budget Review does not state that the second increase might not be implemented.

The second-largest party in the Government of National Unity, the Democratic Alliance, has said it is opposed to any increase in the VAT rate.

In a media briefing before delivering his Budget Speech, Godongwana was asked whether he thought the DA would accept the Budget, considering the VAT increase.

Godongwana queried whether the DA is opposed to a VAT increase per se, or whether something else is at play. “Sometimes it’s useful to call a spade a spade,” he said.

The minister said the DA has recently “lost a lot of battles” – referencing the Basic Education Laws Amendment Act, the NHI Act, and the Expropriation Act – which has created “tensions within the party”, and they “want to win something”.

He said the DA will accept the VAT increase if “other things are addressed, some of which are outside the Budget”.

Godongwana said he is under no illusions there won’t be opposition to the Budget, but the good thing is that “it’s tabling” this afternoon (Wednesday). Thereafter, the parties will start negotiating with each other.

Although some parties’ initial response to the Budget may be vehement opposition to one or another proposal, the minister said he is confident that most of them will eventually support the Budget.

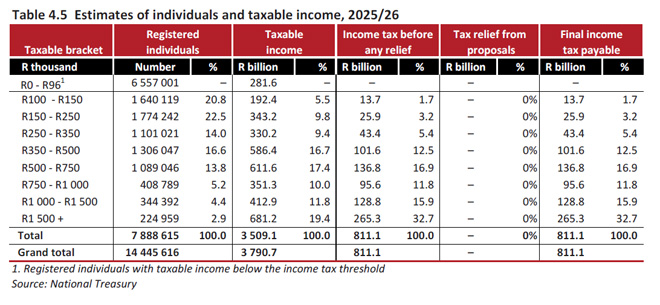

The tax proposals in the Budget are designed to raise R28bn in additional revenue in 2025/26, taking gross tax revenue to R2.006 trillion.

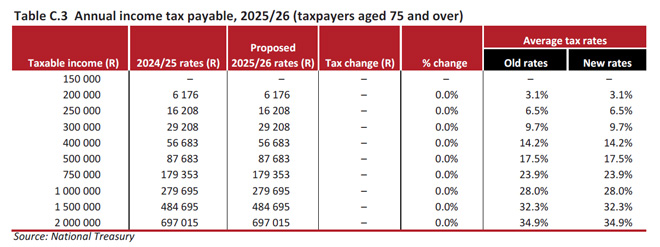

Personal income tax

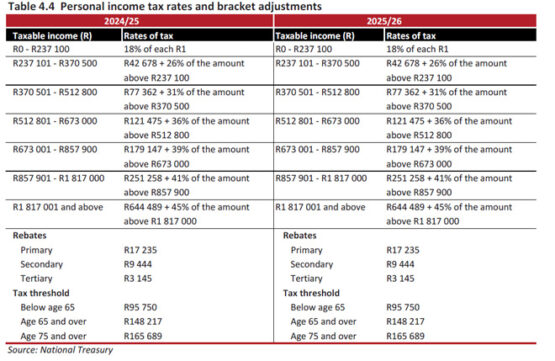

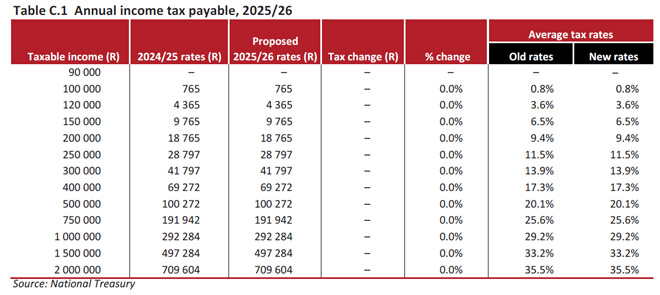

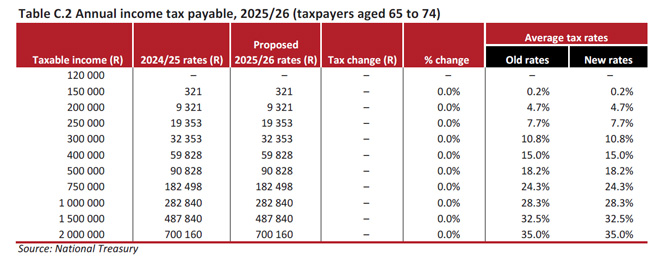

In a blow for payers of personal income tax (PIT), the tax brackets and rebates will not be adjusted for inflation in 2025/26.

This is the second consecutive year in which the PIT brackets have not been adjusted to combat “bracket creep”, the term used to describe what happens if the income bands are not fully adjusted to account for inflation-linked salary or wage increases. Taxpayers whose salaries are adjusted in line with inflation may be pushed into a higher tax bracket and pay relatively more in income tax.

The previous version of the Budget proposed adjusting the tax brackets to provide some relief from the two-percentage-point VAT increase. The proposal was to adjust fully for inflation the two bottom income tax brackets and all the rebates, while the remaining brackets were to be adjusted partially.

Jurgen Eckmann, a wealth manager at Consult by Momentum, says the absence of the inflation-linked adjustment means that personal income taxpayers will ultimately take home less – particularly if their salary increase pushes them into a new tax bracket. If the tax brackets had been adjusted, taxpayers would still pay more in tax, but it would be in line with their increase.

Eckmann provides an example of someone who earns R30 875 a month before tax (R370 500 a year) to illustrate the impact. If she receives a 7% annual increase from her employer, this will shift her into a new tax bracket. Without Treasury providing for this and adjusting the brackets, this person – who now earns R33 078.75 a month before tax – will pay R83 419 in annual income tax, which is almost R10 000 more in tax than she would have paid the previous year (R73 726). So, although her net salary will have increased by 5.65%, her tax bill will have jumped by 13.15%.

The decision to scrap the inflation-linked adjustment means the PIT tables for 2025/26 are the same as they were in 2025/25.

According to the Budget Review, the government will raise R18bn in 2025/26 by not adjusting the PIT brackets.

The Budget Review pencils in raising R19.067bn in 2026/27 and R20.234bn in 2027/28 if the PIT brackets are not adjusted for inflation – a grim reminder that another two years without adjustments cannot be ruled out.

Medical tax credits

As was in the case in Budget 1.0, the medical tax credits will not be adjusted for inflation. They will remain at R364 per month for the first two beneficiaries and at R246 per month for the remaining beneficiaries.

The Budget Review says not adjusting the medical credits will raise R1.5bn in 2025/26. The Review indicates that the credits may not be adjusted in 2026/27 and in 2027/28.

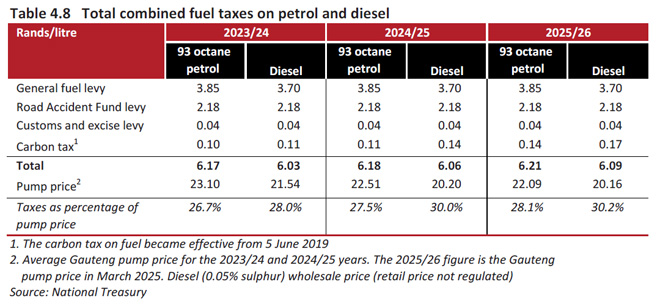

Fuel levies

Another proposal that has been retained in Budget 2.0 is not to increase the fuel levies. This means the general fuel levy, the Road Accident Fund levy, and the customs and excise levy on petrol and diesel will not change. These levies have not been increased since 2022.

But the carbon tax on fuel will increase slightly, from 0.11 cents to 0.14 cents on 93 octane and from 0.14 cents to 0.17 cents on diesel.

The government will “forfeit” R4bn in 2025/26 by not increasing the general fuel levy.

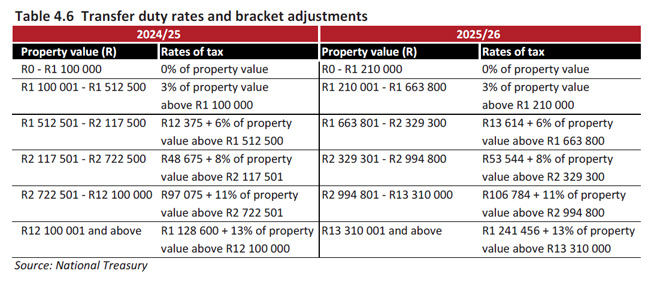

Transfer duty on property transactions

Another welcome proposal that has been carried forward to the revised Budget is increasing the value bands for the duties that are paid when a property is sold. The price brackets will be adjusted by 10% on 1 April. The transfer duty tax rates will remain unchanged.

The adjustment to the brackets will result in transfer duty kicking in from R1.21 million instead of R1.1m.

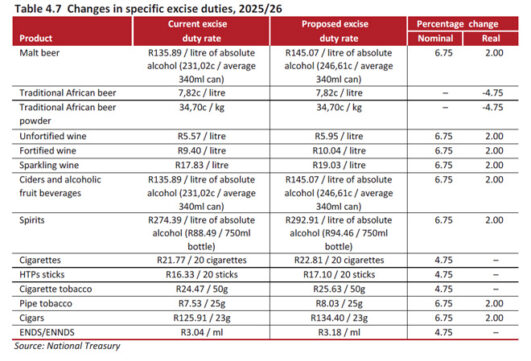

Excise duties on alcohol and tobacco

The updated Budget proposes above-inflation increases in the excise duties on alcohol and tobacco products. However, the increases are lower than those announced in Budget 1.0.

The excise duties on alcoholic beverages will increase by 6.75% instead of 6.83%.

The duties on cigarettes, cigarette tobacco, and vaping, formally called electronic nicotine delivery systems (ENDS) and non-nicotine delivery systems (ENNDS) will increase by 4.75% instead of 4.83%.

The proposed increase for pipe tobacco and cigars is 6.75% instead of 6.83%.

The government plans to raise R1bn in revenue in R2025/26 by increasing the duties on alcohol and tobacco.

No changes to these taxes

The Budget does not propose changes to the following:

- capital gains tax (CGT);

- dividends tax;

- donations tax;

- estate duty;

- the thresholds for the exemption on interest income;

- tax-free investments; and

- the tax treatment of contributions to retirement funds.

Tax on foreign pensions

The Budget contains bad news for foreign nationals who decide to retire in South Africa and for South African expatriates who return home after working abroad.

Currently, foreign retirement lump sums, pensions, and annuities received by South African tax residents are exempt from taxation.

The Budget Review says the current treatment of foreign retirement funds may result in double non-taxation, particularly where South Africa is granted the taxing right by treaty.

“It is proposed that changes be made to the rules that currently exempt lump sums, pensions, and annuities received by South African residents from foreign retirement funds for previous employment outside South Africa, with amendments in the current legislative cycle.”

No wealth tax

The Budget does not propose introducing a “wealth tax”, despite speculation in some quarters that this could be implemented to compensate, in part, for not increasing the VAT rate by two percentage points.

Regarding a wealth tax, the Budget Review merely states what is already known: the South African Revenue Service is collecting and analysing wealth-related data through its High-Net-Worth Individuals Unit, but a final decision has not yet been made on the proposal.

No increase in the ‘sugar tax’

An inflationary increase in the health promotion levy – better known as the “sugar tax” – was due to take effect from 1 April. The government proposes to cancel this increase to allow the sugar industry more time to restructure in response to regional competition, the Budget Review says.

Ad valorem excise duties on smartphones

Budget 2.0 also retains the proposal that, from 1 April, the 9% ad valorem excise duty on smartphones will apply only to smartphones with a price of more than R2 500 at the time of export to South Africa.

Tax revenue estimates

In the Budget Review published on 19 February, National Treasury expected revenue of R1.843 trillion in 2024/25, which was R19.3bn less than projected at the time of the 2024 Budget. In this month’s revised Budget, Treasury has estimated tax revenue of R1.846 trillion for 2024/25, which is R16.7bn less than projected in last year’s Budget.

So, where did the additional R2.6bn come from? Not from PIT receipts. The revised PIT estimate for 2024/25 is R732.3bn, which lower than February’s estimate of R734.2bn.

However, Treasury expects to collect more from companies, with the corporate income tax estimate adjusted upwards from R314.6bn to R316.4bn.

It expects more revenue from domestic taxes on goods and services, at R623bn instead of R625bn, although VAT receipts are now slightly lower at R459.8bn compared to R459.9bn. Treasury also expects slightly more revenue from taxes from international trade and transactions, at R79.1bn to R79.2bn.

In February, Treasury said tax receipts contracted by 2.3% in the first 10 months of 2024/25 compared with the same period in the previous year. Now, Treasury says tax receipts contracted by 1% in the first 11 months of 2024/25 compared with the same period in the previous year.

Our government is failing us. I think it time to go back to apartheid these black leaders are greedy 🙆♂️

Sifiso in apartheid you are a slave. Critical thinking is a solution top most problems not gullible utterances like you just did.

Sifiso, no-one wants to swop one bad system for another. We just need a system that looks after every citizen. It should be based on ubuntu, and not on nepotism or skin colour. You cannot heal a racial divide if there are laws that encourage racial denigration.

Also, our constitution lacks one component which is crucial for human dignity, and that is the right to gainful employment, then we don’t need racially charged laws that only serves to divide our people.

i think they should start cutting benefits of the ones in in parliment ..because these people in the highest are not affected really like the every day workers class …

I hate to say this but the worse thing that could have ever happened to South Africa was democracy! I said what I said and I stand by it!! How do you comprehend uneducated, ill-advised people running a country?? Can barely speak a full sentence in English, I’m sure the maths is not mathing and here they are raising billions only to line their own pockets. I am DISGUSTED!!!!