The threshold at which businesses must register as a VAT vendor will increase from a taxable turnover of R1 million to R2.3m.

The threshold has not been adjusted since 2009, and it has been estimated that if the threshold had been adjusted for inflation, it would be in the region of R2.2m.

The voluntary VAT registration threshold will increase from R50 000 to R120 000. A vendor that makes taxable supplies of more than R120 000 but not more than R2.3m a year can apply for voluntary registration.

The adjustments will take effect on 1 April 2026.

If a business does not exceed the increased compulsory registration threshold as at 1 April 2026, it may apply to deregister for VAT in terms of section 24(1) of the VAT Act, according to law firm Cliffe Dekker Hofmeyr.

Relief for small and micro-businesses

National Treasury proposes lowering the threshold for small business corporations’ income tax to R99 000 from R100 350 in the 2025/26 tax year.

Small businesses with a taxable income of R99 000 to R365 000 will pay a 7% tax rate above R99 001.

The rates for the other income bands remain the same. The rate for small businesses with a taxable income of R365 001 to R550 000 is 21% of taxable income above R365 000. Businesses whose taxable income exceeds R550 001 pay tax at a rate of 27% of taxable income above R550 000.

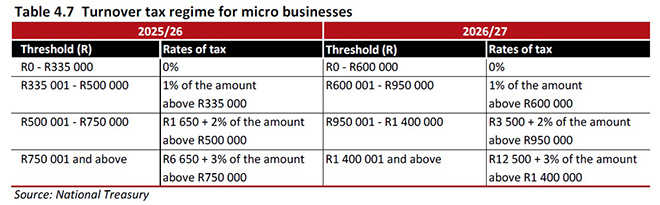

National Treasury has also proposed adjusting the turnover tax regime for micro-businesses. The threshold increases from R335 000 to R600 000, while the turnover bands have been adjusted significantly, as set out in the table below.