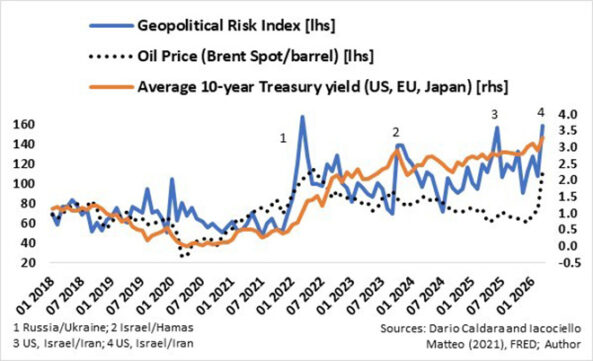

Global financial markets are increasingly under pressure as the war in the Middle East intensifies. The Geopolitical Risk Index, a widely cited, news-based measure of adverse geopolitical events and the risks they pose, is again at extremely high levels, similar to those at the onset of Russia’s invasion of Ukraine in 2022, the onset of the Israel-Hamas war in 2023, and the US/Israel bombing of Iran’s nuclear facilities in 2025.

The Index was developed by economists Dario Caldara and Matteo Iacoviello (both at the Federal Reserve Board). Their 2021 paper, “Measuring Geopolitical Risk”, published in the American Economic Review, presents the index and analyses its effects since 1900.

Global stock market volatility is in crisis territory, with both the CBOE Volatility Index for the S&P500 and the Nikkei Volatility Index above 30.

The massive spending and financing by the hyperscalers, announced in the third and fourth quarters of last year, continues to exert downward pressure on hyperscalers’ debt instruments and increased yield spreads. The increased geopolitical risk, together with the surge in the oil price, is pushing bond yields higher, with a knock-on effect of pushing the cost of equity in financial models higher.

This has undoubtedly caused havoc in private credit and equity funds. Redemption pressures have increased, but strict limits on withdrawals are, according to MarketWatch, “leading to reports of trapped capital”.

With the risk-off cycle firmly under way, the big question is where we are in the cycle.

Although the pull back of global stock market indexes seems mild compared with fear indexes (or volatility indexes) at similar levels in the past, it masks major movements.

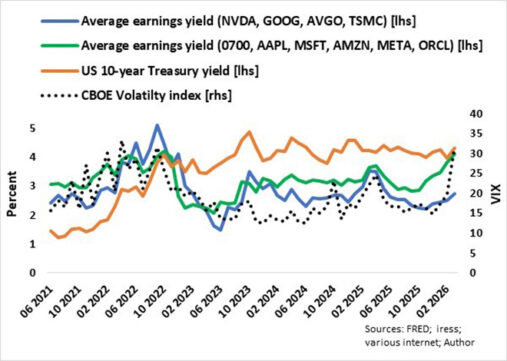

I separated 10 major global tech companies into two groups based on historical earnings yield (inverse of PE). The first group (first tier), with the lower earnings yields (higher PE ratios), consists of Nvidia, Alphabet, Broadcom, and TSMC (Taiwan Semiconductor Manufacturing Company), while the second tier consists of Tencent (0700), Apple, Microsoft, Amazon, META, and Oracle.

The liquidity squeeze emanating from private credit vehicles probably resulted in investors seeking liquidity and hedging via publicly traded stocks and funds, adding to the average de-rating of about 35% of the second-tier tech group since the end of September last year.

The second-tier tech group is now revisiting its five-year high earnings yield (five-year low PE ratio) and is for the first time since December 2022 trading equal to US 10-year Treasury yields. There is a risk that the second tier’s earnings yield could overshoot the US 10-year Treasury yield, though.

In comparison, the first-tier tech group is currently trading at the average earnings yield since February 2023, while the yield spread between the first-tier’s earnings yield and US 10-year Treasuries is like the average spread since end 2022. The first tier’s earnings yield is still 20% lower than the worst levels in October 2023 and April 2025.

It does seem that the second-tier group could be near the top of the risk-off cycle, while the first-tier group is midway there and very vulnerable if the current geopolitical situation persists for longer or even deteriorates, as the fear factor (VIX) will stay higher for longer and even spike further. The same for global stock markets.

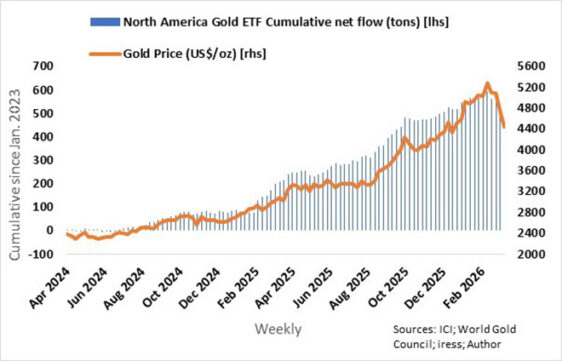

Gold’s behaviour since the onset of the current war has left some investors and commentators arguing that gold has lost its safe-haven status. It is quite normal for gold to retreat when it is perceived that stock market volatility is peaking. It is especially true after the near-parabolic surge in gold since September last year caused by bouts of significant short-covering by commercial traders, North American Gold ETF inflows, and a probable cornering of the silver market.

Read: Silver: We saw the hysteria, will panic follow?

North American Gold ETFs have seen outflows of more than 70 tons of gold since the end of February this year, or nearly 11% of their cumulative net inflows since January 2023.

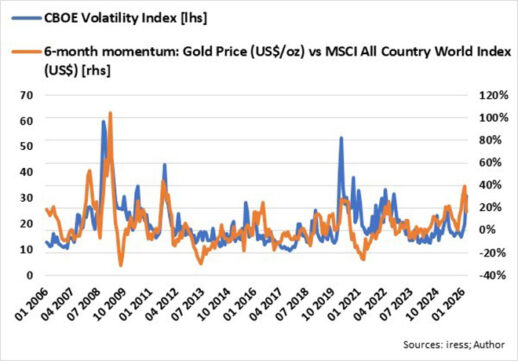

The fact that the gold price took a hammering in the absence of new net short-positions by commercial traders on COMEX seems to indicate that gold’s outperformance relative to global stocks (MSCI All Country World Index) is over for now, thereby indicating a possible peak in the risk-off cycle, at least for now.

The risk-off cycle is peaking. I have turned bullish because the risk-off cycle is peaking and stock markets globally offer reasonable value again. Investors’ mettle will be tested, though, as the swings can be wild.

Ryk de Klerk is an independent investment analyst.

Disclaimer: The views expressed in this article are those of the writer and are not necessarily shared by Moonstone Information Refinery or its sister companies. The information in this article does not constitute investment or financial planning advice that is appropriate for every individual’s needs and circumstances.