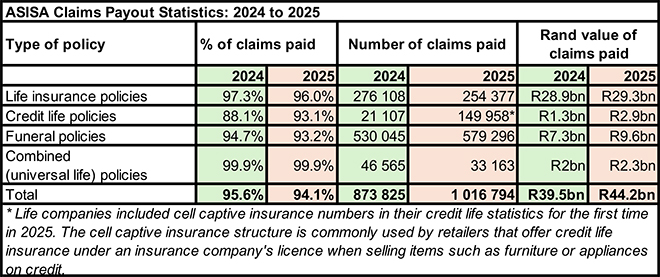

Life insurance members of the Association for Savings and Investment South Africa (ASISA) settled 94.1% of death claims under individual life, credit life, funeral, and universal life policies in 2025, paying beneficiaries R44.2 billion in benefits. In 2024, 95.6% of death claims were paid to a value of R39.5bn.

Gareth Friedlander, a member of the ASISA Life and Risk Board Committee, says that for the past five years, the average claims payout rate for life and funeral policies remained steady between 94% and 96%.

“Policyholders and their beneficiaries should be able to trust that their policies will pay when a life-changing event occurs. We therefore publish the annual average claims payout rate for ASISA members to provide consumers with the peace of mind that life companies will pay valid claims provided the terms and conditions were met, and the policyholder was honest during the application process,” Friedlander said.

ASISA published the death claims payout statistics for 2025 on 10 June 2026. They show that life insurers processed 1 080 930 death claims, of which 1 016 794 were paid, with the balance declined for reasons such as dishonesty, fraud, or contractual exclusions within the first two years from when the policy was taken out.

Friedlander said the highest average claims payout percentage is typically achieved for life insurance policies (including the old universal life policies) because they require some form of risk screening, such as health assessments and lifestyle questions, before the applicant’s life is insured.

Life insurance policies can offer life cover worth millions of rands, and the underwriting process reduces the risk of fraud and non-disclosure at the application stage. When a claim against a life insurance policy is declined, it is most often due to material non-disclosure.

Withholding material information from a life insurer during the underwriting process is dishonest, and a life insurance company is, therefore, fully within its rights not to pay out a claim and declare your policy void should it come to light that you were dishonest or that you failed to disclose important details when you took out your policy. This could have devastating financial consequences for your beneficiaries.

In 2025, 96% of claims against life policies were paid, and 99.9% of claims against universal life policies were paid.

Funeral insurance policies

Funeral insurance policies are designed to pay out quickly and without hassle when an insured family member dies, and they typically do not require blood tests or medical examinations. Funeral policies are also restricted in terms of the maximum cover they can provide.

Since there are no underwriting requirements for funeral insurance, it is often tempting for people to buy funeral cover only once they have developed a serious illness and are expecting to die as a result. To prevent this, funeral cover usually imposes a waiting period of six months for deaths due to natural causes. The main reasons for declining claims against funeral policies are waiting periods, fraud, and unpaid premiums.

The payout rate for funeral policies tends to be slightly lower than for life policies and averaged 93.2% in 2025.

Credit life policies

Credit life policies are designed to cover loans should the policyholder die before the debt has been settled, for example, a home loan or vehicle finance. The payout by a credit life insurance policy decreases as the outstanding loan amount decreases, and once the debt has been repaid, the cover ends. Since premiums are included in the monthly loan repayment, a default on the repayment means no premiums are paid to the life insurer, and the cover therefore lapses.

Friedlander said that claims against credit life policies are most commonly declined because the cover lapsed due to non-payment of premiums or the outstanding loan balance had been settled. The average claims payout rate for credit life policies was 93.1% in 2025.