Investors are entering a more stable macro-economic environment but one that is structurally more complex and less forgiving of passive positioning, according to Discovery Invest’s 2026 Market Outlook, which was released last week.

The report, Market Outlook: Navigating Mega Forces in a Fragmented World, developed with the BlackRock Investment Institute (BII) and Ninety One, presents 2026 not as a continuation of the 2025 rally, but as a year in which long-term structural forces – artificial intelligence, geopolitical fragmentation, demographic divergence, and supply-chain rewiring – will increasingly shape outcomes alongside traditional business cycles.

Its central thesis is that investors are operating in a “business unusual” regime where broad beta exposure may no longer deliver the diversification or return profile it once did.

The report says South Africa is entering 2026 on firmer ground than it has in several years, with improved fiscal credibility, easing energy constraints, and attractive relative valuations strengthening the domestic investment case.

Steadier macro base, but not a return to normal

The global economy enters 2026 on firmer footing. Growth expectations around or above 3%, alongside easing inflation, create what the report terms a “Goldilocks” environment. Monetary policy in major economies is gradually loosening, anchoring expectations and improving visibility.

In the United States, inflation measured by the Personal Consumption Expenditure Index is expected to trend towards about 2.5% year-on-year by late 2026, while growth remained robust into late 2025, with third-quarter GDP at an annualised 4.4%.

Europe has avoided recession, inflation is moving closer to the European Central Bank’s 2% target, and Germany’s fiscal expansion could add roughly one percentage point to GDP over 2026/27.

China presents a more complicated picture: headline growth near 5%, but persistent disinflation, with CPI expected to remain below 1%, and the GDP deflator negative for 10 consecutive quarters.

Ninety One frames the key investment question for the next 12 to 18 months as whether growth or inflation dominates return dynamics. Its base case is that growth will lead.

Historically, growth-led environments tend to see equities and bonds negatively correlated, restoring bonds’ role as portfolio diversifiers. In inflation-led regimes, those correlations often turn positive, reducing diversification benefits.

However, the report cautions that 2026 is unlikely to replicate the broad, concentrated gains of 2025. Returns may be more dispersed and increasingly driven by valuation discipline and active positioning rather than broad market momentum.

AI: transformative engine, concentrated exposure

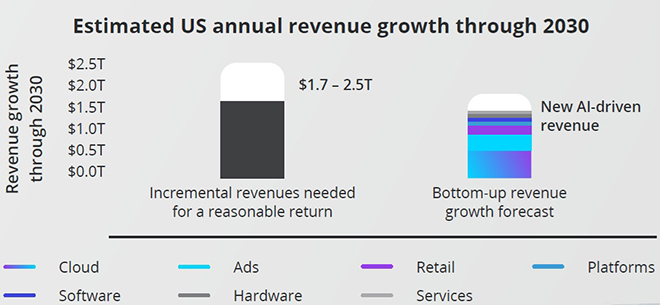

External estimates suggest between US$5 trillion and US$8 trillion in corporate AI-related capital expenditure over the next decade.

Hyperscalers’ race towards Artificial General Intelligence is driving an unprecedented investment cycle.

The report interrogates the return assumptions underpinning this spending. BII analysis suggests that for such investment to generate reasonable returns, revenue growth in the technology sector would need to accelerate meaningfully. If the sector’s share of global revenues rises from 25% to 35%, this could imply roughly US$400 billion in additional annual revenue.

The report presents this as illustrative revenue rather than a formal forecast, highlighting the scale of earnings expansion required to justify current capital expenditure trajectories.

Neither BII nor Ninety One characterises current conditions as a speculative “super bubble”. Instead, they suggest that any cooling in the theme would more likely result in a constructive correction that resets valuations without undermining the long-term opportunity.

At the same time, the report notes that AI capex is now deeply interconnected across supply chains, cloud infrastructure, hardware ecosystems, and data centres. As a result, a slowdown in the investment cycle could transmit more widely through markets than in previous technology cycles.

This concentration dynamic feeds into what the report calls a “diversification mirage” – portfolios may appear diversified across sectors and regions yet remain exposed to the same AI-driven return drivers.

Geopolitical fragmentation as a macro force

Globalisation, the report argues, is being rewired rather than reversed.

The US continues to prioritise domestic production and strategic independence, while emerging markets are strengthening regional alliances.

Trade flows, industrial policy, and capital allocation are increasingly shaped by resilience considerations. Country risk assessment therefore requires greater emphasis on institutional strength and policy credibility.

The report identifies the US midterm elections as a potential inflection point for tariff and fiscal policy.

South Africa: improved anchors, conditional upside

Within emerging markets, South Africa is presented as relatively well positioned.

Improved fiscal discipline, easing energy constraints. and attractive real yields have strengthened its relative appeal.

The country’s removal from the Financial Action Task Force grey list and a sovereign credit upgrade by S&P Global Ratings are cited as milestones that have improved institutional credibility.

Inflation is approaching the South African Reserve Bank’s 3% target, with real rates materially positive, potentially creating room for policy easing in 2026.

The political backdrop remains a variable. The Government of National Unity is described as imperfect but having restored a degree of predictability. The outcome of the municipal elections will test that stability, and reform momentum remains critical to sustaining investor confidence.

Valuations remain supportive

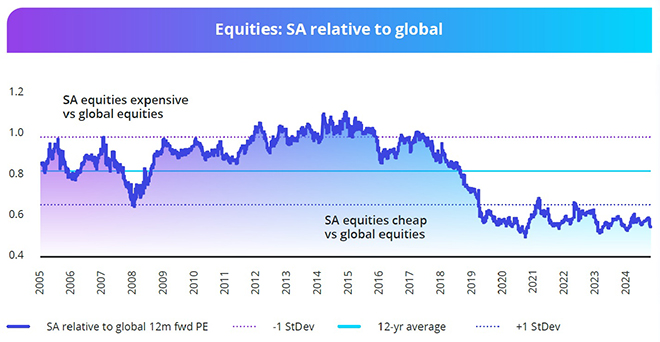

Despite strong performance in 2025 – with the FTSE/JSE All Share Index returning 22% excluding resource stocks – South African equities continue to trade below their 12-year forward price-to-earnings average and at a meaningful discount to global markets.

This valuation differential is relevant when viewed against global market concentration. As US equity markets have become increasingly driven by a narrow group of large technology companies, South Africa’s discount offers exposure to a broader earnings base at comparatively lower multiples.

Ninety One maintains a favourable view on domestic financials, precious-metal producers, and selected industrials. Financials may benefit from rate normalisation and improved credit conditions; precious-metal producers provide geopolitical and inflation hedging characteristics; and industrials stand to gain if domestic reform momentum continues.

Local fixed income well positioned

With real yields in South Africa still attractive and the potential for gradual monetary easing, longer-dated bonds could benefit if yields compress.

Improving sovereign credit dynamics across emerging markets – illustrated by rising net upgrades among higher-yielding sovereigns – reinforce the broader case for emerging markets.

However, the global rate-cutting cycle is expected to be shallower and less synchronised than in prior cycles, and tariff-related pressures could sustain pockets of inflation. Careful calibration across duration and credit exposures remains important.

Three risks for 2026

Despite a more stable macro base, the report flags three overarching risks:

- A slowdown in the AI investment cycle.

- Geopolitical volatility and shifting US policy.

- Potential pockets of financial stress in leveraged segments of the system.

Across these risks, the report suggests that structural interconnections could allow shocks to transmit more broadly than in earlier cycles.

The bottom line: diversification with intent

The report concludes that 2026 will likely be “tougher than 2025” – not necessarily because growth falters, but because easy, concentrated gains may be behind investors.

Its prescription is “diversification with intent”: exposure across regions, asset classes and strategies, aligned with long-term structural forces, combined with the flexibility to adjust as conditions evolve

For South African investors, relatively attractive domestic valuations and a firmer rand are framed as creating an opportunity to blend local assets with global and emerging market exposure.

If the report’s analysis proves correct, 2026 will not simply reward staying invested – it will test how portfolios are constructed, how risks are defined, and whether diversification is structural rather than superficial.

Disclaimer: The information in this article does not constitute investment or financial planning advice.

How is technology driving innovation and transforming modern industries?