South Africa’s long-term insurance industry has crossed a significant financial threshold, with assets under management exceeding R5 trillion for the first time – a milestone that underscores both market momentum and the sector’s underlying capital strength.

Buoyed by strong equity market performance, life insurers that are members of the Association for Savings and Investment South Africa (ASISA) ended 2025 with R5.2 trillion in assets under management, according to industry statistics released on 31 March 2026.

At the same time, the industry’s reach continued to expand. ASISA members managed 46.2 million risk and savings policies at the end of December 2025, up 4% from 44.4 million a year earlier.

Despite this growth, the data points to a complex operating environment – one where rising policy lapses and a persistent insurance gap continue to pose structural challenges.

Strong balance sheets, rising obligations

Life insurers paid out R626 billion in claims and benefits in 2025, covering events such as death, disability and retirement. This includes payouts from life, disability, critical illness and income protection policies, as well as annuities, underwritten pension fund benefits and endowment policies.

From a prudential perspective, the industry remains well-capitalised.

Gareth Friedlander, a member of the ASISA Life and Risk Board Committee, says the long-term insurance industry remains financially strong. ASISA statistics show that, collectively, life insurers held R380.5 billion in reserves at the end of December 2025, against the Prudential Authority’s Solvency Capital Requirement (SCR) of R222.9 billion, resulting in a healthy average SCR cover ratio of 1.71 (or 1.71 times the legal requirement).

Friedlander explains that the SCR is calibrated under the Solvency Assessment and Management (SAM) regulatory framework to ensure that insurers can meet their obligations to policyholders should a 1-in-200-year risk event occur.

“When insurers exceed the required SCR, it means that they have enough capital to survive an event even more catastrophic than the 1-in-200-year risk event.”

According to Friedlander, individual life insurers set their SCR cover ratio targets annually, depending on their risk appetites, strategies and business models.

“When life insurers aggressively pursue capital efficiency by deploying resources to increase their return on capital, they tend to target SCR cover ratios towards the lower end of their risk appetite ranges.”

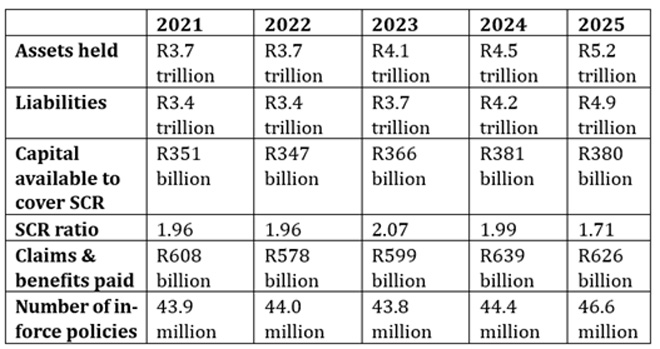

Industry snapshot: 2021–2025

The data shows a steady expansion of the life insurance sector over the five-year period, with assets under management rising from R3.7 trillion in 2021 to R5.2 trillion in 2025, alongside a corresponding increase in liabilities from R3.4 trillion to R4.9 trillion.

Capital available to meet the Solvency Capital Requirement remained broadly stable, edging up from R351 billion in 2021 to R380 billion in 2025, although the SCR cover ratio declined from a peak of 2.07 in 2023 to 1.71 in 2025, indicating a moderation in capital buffers as balance sheets expanded.

Claims and benefits paid fluctuated but remained elevated, reaching R626 billion in 2025, while the number of in-force policies showed gradual growth, increasing from 43.9 million in 2021 to 46.6 million in 2025, reflecting continued expansion in policyholder reach.

Risk cover expands – but lapses rise

In 2025, consumers took out 10.8 million new individual recurring premium risk policies, up 3.8% from 10.4 million in 2024. This included 6.2 million funeral policies, 1.9 million credit life policies, and 2.7 million life, disability, critical illness and income protection policies.

However, this growth is being partially offset by a renewed increase in policy lapses.

Some 8.7 million risk policies lapsed in 2025, compared with 8.2 million in 2024, 8.3 million in 2023, and 8.3 million in 2022. A lapse occurs when the policyholder stops paying premiums on a risk policy, resulting in no fund value.

“Policy lapses are always concerning. Unless lapsed policies are replaced with new policies, lapses widen South Africa’s sizeable insurance gap, leaving more families financially vulnerable should their breadwinner die or become disabled.”

The scale of this gap remains material. The 2025 ASISA Life and Disability Insurance Gap Study found that South Africa’s 16.1 million formally employed income earners had enough life and disability cover at the end of December 2024 to meet only 39% of their families’ income needs in the event of death or disability.

Savings behaviour shows mixed signals

On the savings side, new individual recurring premium savings policies – including endowments and retirement annuities – declined by 5.5%, from 568 586 in 2024 to 537 203 in 2025.

Encouragingly, however, the downward trend in policy surrenders continued.

Policyholders surrendered 458 848 recurring premium savings policies in 2025, compared to 521 736 in 2024, 563 326 in 2023, and 585 265 in 2022. Policy surrenders occur when policyholders stop paying premiums and withdraw the fund value before maturity.

New single premium savings policies moved in the opposite direction, increasing by 5.1% from 207 744 in 2024 to 218 276 in 2025.