The National Financial Ombud Scheme (NFO) recovered R442.99 million for consumers in 2025, while handling more complaints across its divisions and reducing the average time to close cases to 85 working days.

The NFO last week released its second annual report since its recognition as an industry ombud scheme on 1 March 2024.

The NFO now consists of three divisions: Banking and Credit, Life Insurance, and Non-life Insurance. Banking and Credit were separate divisions until July 2025.

The Scheme’s latest data shows where consumer pressure is building most sharply: digital banking fraud, rejected funeral-benefit claims, and continued disputes over exclusions in motor and homeowners’ insurance. In Banking, fraud remained the single biggest complaint category, while in Life Insurance, funeral benefits continued to dominate complaints. In Non-life Insurance, motor and homeowners’ cover generated the largest share of disputes.

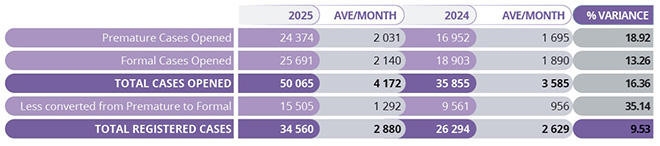

The NFO opened 50 065 cases in 2025, an increase of 16.36% compared with 2024, and closed 34 277, an increase of 2.01%.

Of the cases closed across the scheme’s divisions, only 19% were decided in favour of the consumer. This is in line with last year’s percentage.

The NFO said it recovered R442 994 504.11 for consumers in 2025, compared with R328 550 212.58 in 2024.

The recoveries by division were:

- Life: R299 629 812.82

- Non-life: R82 888 820.70

- Banking: R53 002 204.18

- Credit: R7 473 666.41

In Banking, the recovery figure was heavily shaped by fraud-related matters. The NFO said about 60% of the more than R53m awarded to banking customers was linked to fraud cases. It said many of the matters in which awards were made involved findings that banks had failed to act quickly enough once they became aware of fraudulent activity.

A key qualification in this year’s report is that the 2024 report covered March to December only, rather than a full 12-month period, so direct year-on-year comparisons should be treated with caution.

Because the 2024 figures do not cover a full year, the report uses report uses monthly averages for the most meaningful year-on-year trend analysis.

Cases opened and overall trends

Premature cases opened increased from 1 695.20 a month in 2024 to 2 031.17 cases on average in 2025, representing a 20% increase, while formal cases opened rose from 1 890.30 to 2 140.92 a month, a 13% increase.

A premature case refers to a complaint submitted to the NFO before the consumer has given the provider a reasonable opportunity to resolve it internally. The ombud sends these complaints to the provider. If the provider fails to resolve the issue, or fails to respond, the matter can then proceed as a formal case.

The total number of cases opened increased from an average of 3 585.50 a month in 2024 to 4 174.92 in 2025, which is a 16% growth in overall case openings.

The NFO highlighted the increase in cases converted from premature to formal, which rose significantly from an average of 956.10 a month in 2024 to 1 292.08 in 2025, an increase of 35.14%.

The report said this increase might be the result of improved case progression, stronger screening processes, or more matters meeting the criteria for formal investigation.

Despite the higher number of total cases opened, the average number of total registered cases increased more moderately, from 2 629.4 a month in 2024 to 2 891.5 in 2025, a 9.97% increase.

Cases opened by division

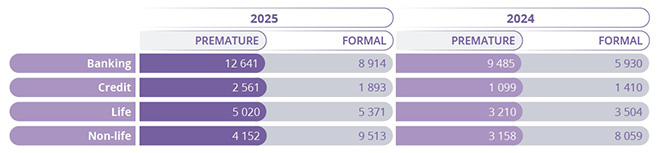

When case openings are broken down by division, Credit saw the most dramatic increase in early-stage complaints. Premature cases increased from an average of 100.9 a month in 2024 to 213.42 in 2025, representing an increase of more than 100%. Formal cases rose from 141 to 157.75 a month, an increase of about 11.9%.

The growth in cases was not driven only by traditional lending disputes. The division also saw a noticeable increase in fraud-related complaints, particularly card-not-present transactions linked to vishing scams and the unauthorised use of card details and one-time passwords. Credit complaints also raised concerns about poor affordability checks, credit refusals, and unfair debt collection.

The Life Division also experienced a significant increase in premature and formal cases. Premature cases grew by about 31.2%, from 321 a month in 2024 to 421.17 in 2025, while formal cases increased by about 27.7%, from 350.4 to 447.58 a month.

The Banking Division maintained its position as the largest driver of case volumes.

There was a significant increase of 25.4% in formal cases, from an average of 593 cases a month to 742.83. Premature cases increased by about 11%, from 948.5 cases a month in 2024 to 1 051.17 in 2025.

Fraud remained the highest category of banking complaints. The NFO said complaints involving unauthorised transactions, account hijackings, and social-engineering scams had risen sharply as more consumers turned to digital banking. It added that fraudsters were increasingly exploiting online channels to persuade customers to disclose sensitive information or approve fraudulent payments.

Of the 14 685 cases registered by the Banking Division, the majority related to the country’s major retail banks. The release said Standard Bank recorded the highest number of complaints at 2 975, followed by First National Bank (2 705), Capitec (2 641), Nedbank (2 482), and Absa (2 234).

The Non-life Division continued to have the highest number of formal cases per month among the divisions. This was despite a decline of about 1.6% in formal cases, from 805.9 a month in 2024 to 792.75 in 2025.

Premature cases increased by about 9.6%, from 315.8 a month in 2024 to 346 in 2025.

Cases closed and closure trends

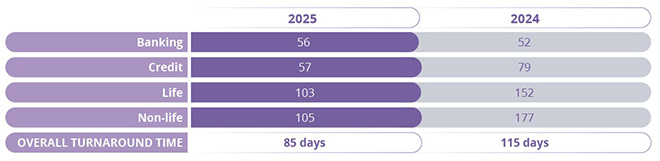

The report says formal closures increased by 4.5%, and the average time to close cases improved from 115 working days in 2024 to 85 working days in 2025.

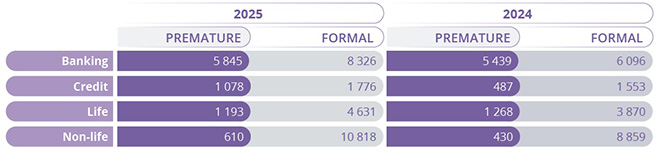

At divisional level, Banking closed 14 171 cases, Non-life 11 428, Life 5 824, and Credit 2 854.

In Life, the report says total cases finalised declined by 2.6%, but formal cases finalised increased by 17.4%.

In Banking, cases closed increased from 11 535 in 2024 to 14 171 in 2025, while Credit closures increased from 2 040 to 2 854.

In Non-life, the division ended the year with 2% fewer registered complaints and 3% more resolved complaints compared with 2024. The division’s average turnaround time improved to 105 working days, from 117 days at the beginning of the year, which it attributed to increased staff capacity earlier in the year and fewer newly registered complaints in the second half.

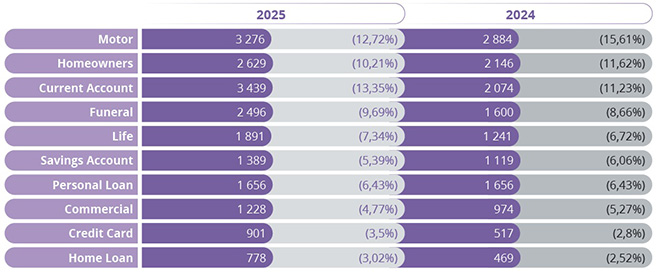

Product categories driving complaints

The main complaint categories by product were motor vehicle insurance, homeowners’ insurance, funeral cover, current accounts, personal loans, and credit cards.

Motor insurance was the leading Non-life category at 35.4%, followed by homeowners’ insurance at 27.5%, and commercial insurance at 12.1%.

Within motor insurance, accident claims accounted for 70% of vehicle disputes, while theft and hijack claims made up 8%. The main reasons for complaint in this category were rejected claims based on exclusions for driving under the influence, followed by alleged lack of due care or recklessness.

Within homeowners’ insurance, acts of nature accounted for 42% of complaints, followed by burst water apparatus, such as geysers, at 15%. The biggest flashpoints were rejected claims based on exclusions for gradual deterioration, lack of maintenance or wear and tear, followed by disputes over defective design, construction, or materials.

Within the Life division, funeral benefits accounted for 46.23% of formal cases closed, followed by life policies at 33.92%, and disability at 7.43%.

Declined claims were the main cause of complaint for funeral benefits (50%) and disability benefits (79%), while poor communication or service (40%) was the main cause for complaints on life policies.

Findings for and against complainants

The findings in favour of complainants differed significantly across divisions:

- Credit, 37%

- Life, 27%

- Banking, 17%

- Non-life, 11%

Consumer satisfaction scores were highest in the divisions with the highest proportion of findings in favour of complainants.

The report records 76% satisfaction in Credit, 72% in Life, 64% in Banking and 42% in Non-life. These divisional percentages take into account only surveys that were successfully returned to the NFO.

The report says this trend suggests that complainants’ perception of fairness and success in their cases significantly influences their overall satisfaction with the NFO process. Although other factors such as service quality, communication, and case handling time contribute to satisfaction levels, the likelihood of a favourable outcome remains one of the most impactful drivers of positive survey responses.