The government’s temporary intervention in fuel pricing has reduced the contribution of taxes and levies on inland 95 octane petrol from more than 30% to 18%.

This relief was introduced when Brent crude surged past $100 per barrel because of the US-Iran conflict and continues to hover near $110. The outlook for the oil price depends largely on how long ships will be prevented from moving through the Strait of Hormuz.

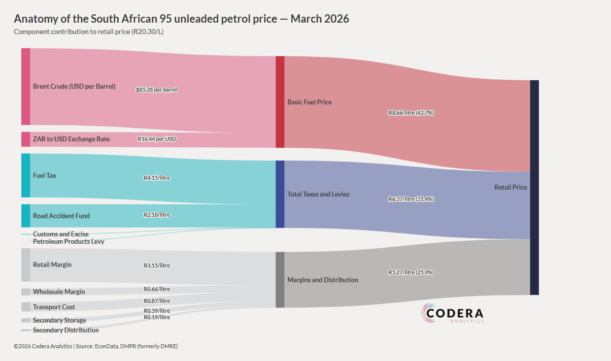

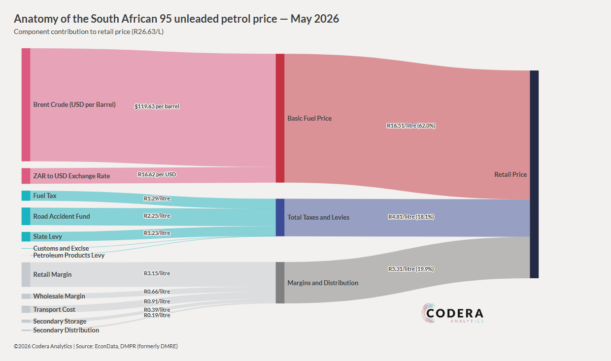

Codera Analytics data scientist Jan-Hendrik Pretorius published their petrol price projections last week, showing the impact of taxes and levies on the pump price of fuel.

The prediction is that a prolonged closure of the Strait of Hormuz could push up the price to $160 per barrel. The general fuel levy was cut by R3 per litre for petrol and R3.93 for diesel until 2 June.

Although skyrocketing global oil prices remain the main driver of the dramatic increase in the petrol price, government taxes undoubtably play a dominant role.

Oil price shocks

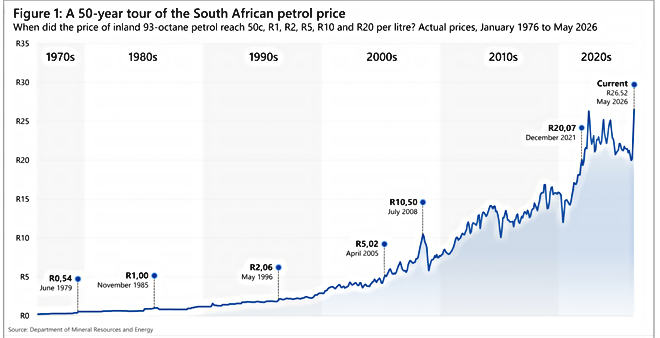

During the financial crisis in 2008, oil prices spiked to around $147 per barrel and the rand traded at R7.60 to the dollar. The petrol price was about R11.50.

In 2022, when the Russia-Ukraine war erupted, the oil price traded above $100 and the rand/dollar exchange rate was around R16.50, close to the current level. However, the petrol price is now almost 22% higher at R26.63.

Maarten Ackerman, chief economist at Citadel, says the comparison between the current situation and the Russia-Ukraine situation is not simply a matter of the oil price and the rand/dollar exchange rate.

This time, he says, many other dynamics are playing out in terms of freight and transport costs. For example, the Russia-Ukraine conflict did not affect 20% of global supply.

“As a result of that, freight costs did not increase sixfold, as they did this time around, and Russian oil eventually did make it into other markets,” explains Ackerman.

“This time around, we are sitting with a supply shock of 20% of global supply, having a significant impact not only on the oil price but also on freight costs.”

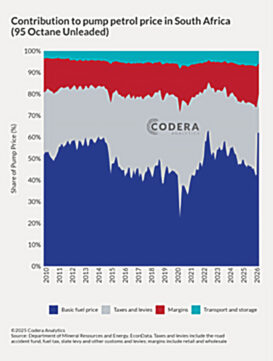

Fuel levies in South Africa make up about a third of the final pump price, Ackerman said referring to the Codera analysis of the pump price. The blue presents the basic fuel price and the grey the taxes and levies.

The basic fuel price today is basically the same as in 2022 when the Russia-Ukraine war started. However, this time around the government is providing significant relief through cutting taxes, not permanently, but for a couple of weeks or months, to provide some buffer.

Were it not for that, the petrol price would have been significantly higher.

Fuel levies

Dawie Klopper, investment economist at PSG, says the fuel levy is like value-added tax. It is an indirect tax. Everybody pays it somehow.

Absent the fuel levy, the government will need additional revenue to make up for the loss. In the 2024/25 tax year, the South African Revenue Service collected almost R80 billion from the fuel levy. In the 2025/26 tax year, this increased to more than R83bn.

National Treasury said in a statement the fuel levy relief measure is designed to be revenue neutral. It will be funded through a combination of higher-than-expected tax revenue and underspending and will not have an impact on the 2026 Budget.

The government again promised a review of the fuel price formula whose conclusion will determine how prices are regulated going forward.

Klopper says the alternative to fuel taxes could be to cut government expenditure by reducing the size of the public sector and cutting salaries. But that will not happen.

South African motorists are not alone. Fuel taxes in Europe and Organisation for Economic Co-operation and Development countries can easily make up between 40% and 60% of fuel prices at the pump. The average in Europe is between 50% and 52% compared with our 31% (without the current relief).

Future risk

As the oil price remains above $100, inflation expectations are rising again, says Ackerman. The risks are clear for South Africa. The country has increased its dependence on Middle Eastern fuel. At the same time, the rand has weakened, meaning South Africa faces a double shock from higher oil prices and currency pressure.

“This increases inflation risk and could delay the benefits of recent policy reform,” Ackerman adds.

Amanda Visser is a freelance journalist who specialises in tax and has written about trade law, competition law, and regulatory issues.

Disclaimer: The views expressed in this article are those of the writer and are not necessarily shared by Moonstone Information Refinery or its sister companies.