The amendments to the Companies Act, which took effect on 1 April, require companies to be more transparent about their ownership structures. The new disclosure requirements are a bolt-on to the Act’s existing disclosure obligations. This has resulted in an unnecessarily complicated disclosure regime, with different but overlapping disclosure requirements applicable to different categories of companies. In this article, Cari Cole-Morgan, the head of knowledge management at Werksmans Attorneys, and Julian van Niekerk, a director of the law firm, explain the disclosure regime that applies to private companies.

Beneficial interest vs beneficial ownership

The linchpin of the new disclosure regime is the concept of a “beneficial owner”.

A beneficial owner of a company is, in essence, an individual (a natural person) who, directly or indirectly:

- Ultimately owns that company; or

- Exercises effective control of that company.

The definition of beneficial owner goes on to list several ways in which an individual may ultimately own or effectively control a company. For instance, a beneficial owner includes someone who can exercise control of a company through a “chain of ownership or control” by controlling the holding company of that company. The list is not closed, so the definition is extremely wide.

To make sense of the new disclosure regime, it is necessary to distinguish the novel concept of a beneficial owner from the pre-existing notion of “beneficial interest”.

A beneficial interest in a private company’s securities is the right of a person (through ownership, agreement, relationship or otherwise) to:

- Participate in any distribution in respect of the company’s securities;

- Exercise (or cause to be exercised) rights attaching to the company’s securities; or

- Dispose (or direct the disposal) of the company’s securities, or any part of a distribution in respect of the securities.

In our view, a key difference between the concepts of beneficial ownership and beneficial interest is that the former requires one to look “up the chain”, whereas the latter does not necessarily do so.

This is best explained by way of example. Suppose private company A is wholly owned by private company B, which, in turn, is wholly owned by natural person John. It is clear that John is the beneficial owner of A. However, in our view, assuming that there are no special arrangements between the parties, the holder of beneficial interests in the securities of A is B, not John. This is because B holds all the beneficial interests in A’s shares in its own right as a legal person separate from John. John himself does not have any legally enforceable rights against A. The fact that John may, in his capacity as a shareholder of B, indirectly influence how B exercises its rights against A does not change this.

From regulated companies to affected companies

Before the amendments, a private company was subject to disclosure obligations only if it was classified as a “regulated company”.

According to the Act, a private company is a regulated company if, inter alia, more than 10% of the issued securities in the company have been transferred within 24 months “immediately before the date of an affected transaction or offer”.

In the context of determining disclosure obligations, this definition does not make sense, because there is no “affected transaction” or “offer” to speak of. In our view, the only intelligible reading of the definition for the purposes of the disclosure requirements (which effectively entails re-writing the definition) is that a private company is classified as a regulated company at a particular date if more than 10% of its securities were transferred within 24 months prior to that date. Even on this charitable reading, the classification of a private company as a regulated company remains a moving target, because the moment a private company passes the 24-month mark, it automatically reverts to being a non-regulated company.

Pursuant to the amendments, the disclosure obligations that apply to a private company are now mainly determined by reference to whether the company is an “affected company”.

An “affected company” is defined as:

- A regulated company; or

- A private company that is controlled by, or a subsidiary of, a regulated company.

Since the definition of “affected company” refers to “regulated company”, the latter definition and our reading of it referred to above remains relevant. The major difference post the amendments is that the uncertainty surrounding the classification of a company as a “regulated company” has been amplified across company groups.

Using our example above, suppose John sells 20% of B. This would, according to our reading, render B a regulated company for 24 months from the date of sale. However, the sale not only renders B an “affected company” (based on it being a regulated company), but also A (because it is a subsidiary of a regulated company). On the date of expiry of the 24-month period, therefore, both A and B will revert to the status of non-affected company. Such automatic switching of categories could, potentially, be difficult to keep track of in large company groups.

Disclosure requirements from 1 April

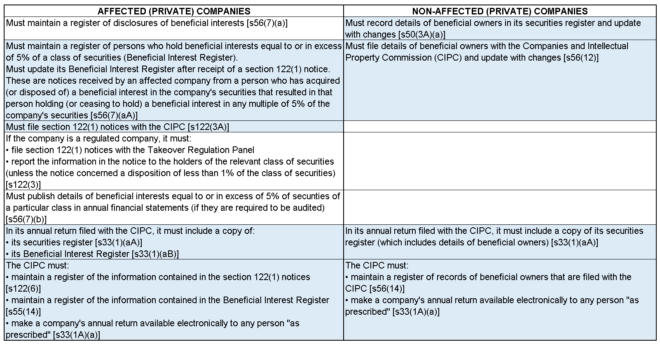

The disclosure requirements that apply from 1 April, as set out in the Act, are summarised in the table below. The new disclosure requirements are shaded in blue. As shown in the table below, the disclosure requirements applicable to non-affected companies are all new.

Regulations

The final regulations relating to the new transparency provisions were published and came into force on 24 May. These regulations are not a model of clarity. They appear to confuse the concepts of beneficial interest and beneficial ownership, as well as the disclosure requirements that apply in relation to affected versus non-affected companies. The information brochures and guidance note published by the Companies and Intellectual Property Commission (CIPC) are similarly unclear.

Conclusion

Despite the concerns regarding the new transparency provisions outlined above, we anticipate that compliance with the provisions should be relatively straightforward for private companies with simple shareholding structures that change infrequently.

However, the unnecessarily complicated disclosure regime contained in the Act, compounded by the regulations’ lack of clarity, are a cause for concern for directors of companies with complex shareholding structures.

The disclosure obligations described above are already in force, and the Act makes no provision for a grace period within which companies may become compliant.

Although no penalties have yet been specifically prescribed for non-compliance with the transparency provisions, a contravention of the Act may result in the issue of a compliance notice by the CIPC. Failure to comply with a compliance notice may result in a court-ordered administrative fine or a referral of the matter to the National Prosecuting Authority for prosecution as an offence.

Disclaimer: The views expressed in this article are those of the writers and are not necessarily shared by Moonstone Information Refinery or its sister companies. The information in this article does not constitute legal advice that is appropriate to every individual’s needs and circumstances.

Thank you for the informative article.