To account for the impact of inflation, this year’s Budget introduced changes to the tax tables for retirement fund cash lump sums taken before and at retirement. Carrie Norden discusses how you can account for these increases when calculating the tax-free amounts available to you when accessing your retirement fund.

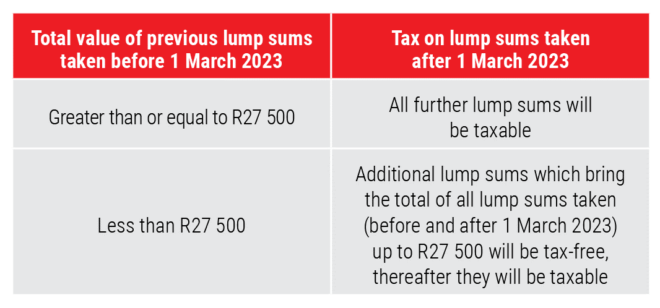

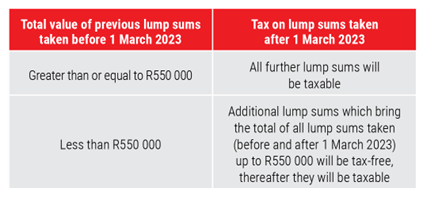

From 1 March 2023, the tax-free amount that can be taken as a lump sum pay-out from a retirement fund increased by 10%, from R25 000 to R27 500 before retirement, and from R500 000 to R550 000 at retirement. (The previous and current tax tables are at the end of this article.) These tables were last amended in 2014.

But just because the tax-free amounts have increased, it does not necessarily mean that R50 000 or R2 500 of your next lump sum taken from 1 March 2023 will be tax-free – the R550 000 and R27 500 “lifetime” caps apply, as shown in Table 1 and Table 2 and discussed below.

Table 1: Changes to the taxation of retirement fund lump sums – before retirement

Table 2: Changes to the taxation of retirement fund lump sums – at retirement

The amounts have changed; the rules around withdrawals are the same

You can take a once-off withdrawal from your pension or provident fund if you leave your employer, or from a preservation fund before retirement.

You may also withdraw from a retirement annuity (RA) and preservation fund in certain circumstances, such as leaving the country and ceasing to be a South African tax resident for an uninterrupted period of at least three years from 1 March 2021.

You may also access a cash lump sum from your retirement fund when you retire, and your beneficiaries may choose to access cash from your retirement savings on your death.

Remember, the tax-free amount available is once-off

According to the South African Revenue Service (Sars), taxpayers are responsible for understanding the tax consequences of their decision to withdraw from a retirement fund before the instruction is submitted to their retirement fund administrator.

It is therefore important to get to grips with the tax calculation before accessing your retirement fund. Key to this is understanding how amounts you may have received in the past, such as a severance benefit from your employer, may impact your tax liability on your planned cash withdrawal.

And remember, once you submit your instruction to your retirement fund administrator, the amount of the cash lump sum indicated on your exit form is seen as belonging to you, for tax purposes, which means that the instruction cannot be reversed or amended, even if the administrator has not yet applied for the tax directive.

When a retirement fund member or beneficiary takes a cash lump sum from a retirement fund, the prevailing retirement fund lump-sum tax tables determine the amount of tax to be paid. A portion of this amount is tax-free, as discussed above. This tax-free amount is a “once-in-a-lifetime” benefit, irrespective of the number of retirement funds to which a taxpayer belongs. It is reduced by any taxable lump sums received previously.

All the lump-sum benefits that were previously received by, or that accrued to, the taxpayer (in other words, to which they became entitled) on or after the following dates, are added together to calculate how much tax is owed on the current lump sum being received, applying the current tax tables.

The following lump sums are considered in this calculation:

- Retirement fund lump-sum retirement benefits that were received by, or that accrued to, the taxpayer on or after 1 October 2007 (changes made to the tax laws became effective on this date). This includes lump sums received from a retirement fund on retrenchment (provided certain criteria are met), at retirement and on death, as well as permissible lump-sum withdrawals from a living annuity.

- Retirement fund lump-sum withdrawal benefits that were received by, or that accrued to, the taxpayer on or after 1 March 2009 (changes made to the tax laws became effective on this date).

- Severance benefits (cash payments from an employer to an employee on the loss or termination of employment, as defined in the Income Tax Act) that were received by, or that accrued to, the taxpayer on or after 1 March 2011 (changes made to the tax laws became effective on this date).

To confirm which taxable lump sums you received previously, you can contact Sars or use the functionality available on eFiling.

Examples

The following examples show how a taxpayer would be impacted by the change in the retirement fund lump-sum tax tables where that taxpayer received a lump sum before the tax tables changed on 1 March 2023.

Calculation 1

Mr A is retiring and has two RA accounts. He retired from RA 1 before 1 March 2023 and took a cash lump sum of R500 000, receiving the full R500 000 tax-free. After 1 March 2023, Mr A decided he also wants to retire from RA 2 and would like to take a cash lump sum of R200 000.

R50 000 of the R200 000 lump sum taken will be tax-free, and R150 000 will be taxable. This is because the total value of Mr A’s previous retirement lump sums taken before 1 March 2023 was less than R550 000 (at R500 000), and he has R50 000 tax-free remaining. The tax on the R200 000 he chooses to take now would be calculated as follows:

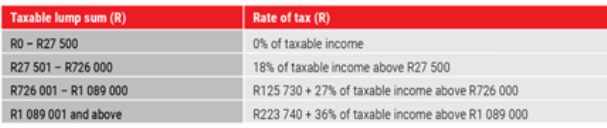

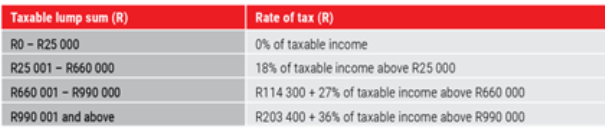

Step 1: Calculate the tax on the total lump sums taken (previous and current) by applying the retirement lump-sum tax table – at retirement – from 1 March 2023 (Table 4).

Total lump sums taken (current and previous) = R500 000 + R200 000 = R700 000

Tax on total lump sums taken (current and previous) = (R700 000 – R550 000) x 18% = R27 000

Step 2: Calculate the tax on the previous lump sum taken by applying the retirement lump-sum tax table – at retirement – from 1 March 2023 (Table 4).

This step is important and tricky to understand, because it applies the hypothetical tax that Mr A would have paid on the previous taxable lump sum using the current tax table, and not the actual tax that Mr A paid using the tax table prevailing when the previous lump sum was received.

Tax on previous lump sum taken (R500 000) = R0 (the amount falls within the R550 000 tax-free portion)

Step 3: Calculate the tax on the current lump sum taken (after 1 March 2023).

Tax on current lump sum taken (R200 000) = Tax on total lump sums less tax that would have been paid on previous lump sum (using the current tax table)

= R27 000 – R0

= R27 000

Mr A will therefore pay tax of R27 000 on the R200 000 retirement lump sum. He will receive R50 000 of this tax-free because he has not yet fully utilised his new R550 000 lifetime tax-free allowance.

Calculation 2

If the facts were slightly different and Mr A’s previous taxable lump sum was R600 000 instead of R500 000, he would have already fully utilised his tax-free lifetime amount of R550 000, because his previous taxable lump sum exceeded the current tax-free amount.

The tax on the R200 000 second retirement lump sum he chooses to take after 1 March 2023 would be calculated as follows:

Step 1: Calculate the tax on the total lump sums taken (previous and current) by applying the retirement lump sum tax table – at retirement – from 1 March 2023 (Table 4).

Total lump sums taken = R600 000 + R200 000 = R800 000

Tax on total lump sums taken = R39 600 + (R800 000 – R770 000) x 27% = R47 700

Step 2: Calculate the tax on the previous lump sum taken by applying the retirement lump-sum tax table – at retirement – from 1 March 2023 (Table 4).

Tax on previous lump sum taken (R600 000) = (R600 000 – R550 000) x 18% = R9 000

Step 3: Calculate the tax on the current lump sum taken (post 1 March 2023).

Tax on current lump sum taken (R200 000) = Tax on total lump sums less tax that would have been paid on previous lump sum (using the current tax table)

= R47 700 – R9 000

= R38 700

Mr A will therefore pay tax of R38 700 on the R200 000 in this example, because he has already fully utilised his R550 000 lifetime tax-free amount, and the R200 000 is fully taxable.

In both these examples, Mr A received a cash lump sum on retirement before and after 1 March 2023, but the same principle and calculation method would apply if Mr A had previously withdrawn from a retirement fund before 1 March 2023, or if he had received a severance benefit from his employer.

In other words, the current tax due is calculated by applying the current retirement fund lump-sum tax table applicable to the current lump sum being taken (that is, either the tax table before or at retirement) to both the total lump sums taken (current and previous) and the previous taxable lump sums.

What to do with this information

It is important to understand the access you have to your retirement fund savings, as well as the calculations used, so that you do not run into an unexpected tax bill. If this feels overwhelming, you may wish to speak to a good, independent financial adviser or a tax consultant. As always, it is advisable not to dip into your retirement savings unless you really need to, given the impact this will have on the income you have left to sustain you in your retirement.

Tax tables

Table 3: Retirement fund lump-sum tax table – before retirement

From 1 March 2023:

Before 1 March 2023:

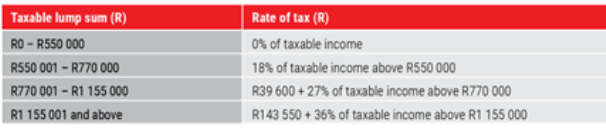

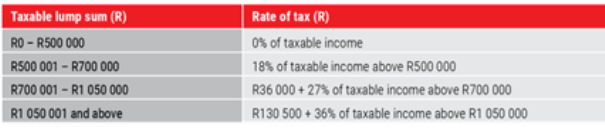

Table 4: Retirement fund lump-sum tax table – at retirement*

From 1 March 2023:

Before 1 March 2023:

*This tax table applies to retirement fund lump-sum benefits received on retirement, retrenchment, and death, as well as permissible lump-sum withdrawals from a living annuity. It also applies to severance benefits (cash payments from an employer to an employee on the loss or termination of employment, as defined in the Income Tax Act).

Carrie Norden is a senior tax specialist at Allan Gray.

Disclaimer: The information in this article does not constitute tax advice.