The Tax Administration Amendment Act of 2026, which came into law on 1 April, contains positive amendments, such as the ability to apply for a suspension of payment for an estimated assessment.

However, the most consequential change concerns the bona fide inadvertent error defence when understatement penalties are applied. It is now available only if the understatement is “substantial”.

“The bona fide inadvertent error defence has not disappeared, but it has been repositioned and materially narrowed,” says Joon Chong, tax partner at Webber Wentzel.

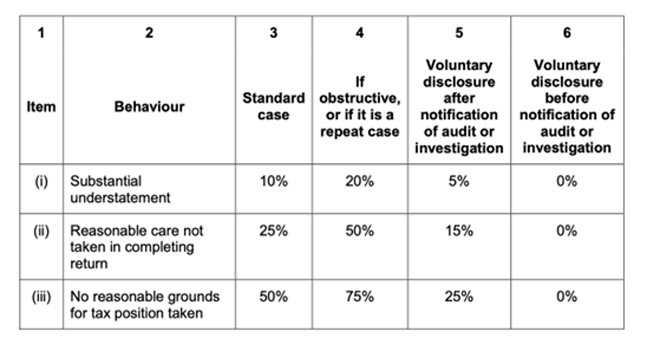

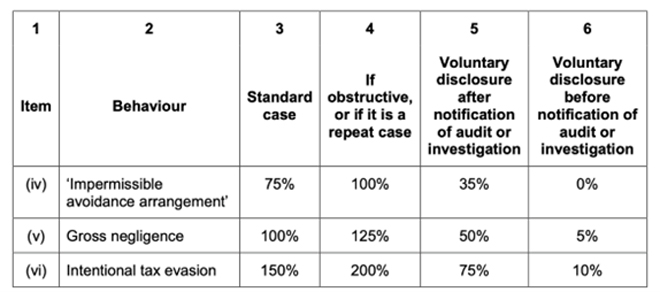

A substantial understatement penalty is triggered by an objective quantum threshold and carries a 10% penalty in standard cases.

Nico Theron, founder of Unicus Tax Specialists, says the South African Revenue Service always argued that a bona fide inadvertent error could not be the gatekeeper to the understatement penalty regime.

Theron explains that the bona fide inadvertent error defence has now effectively been removed as a gatekeeper and added as a ground for remittance. The penalty will be remitted if the taxpayer is not guilty of any of the behaviours in the table and the understatement is not substantial.

If the taxpayer is not guilty of any of the behaviours in the table, but the understatement is substantial (the greater of 5% of the tax chargeable or refundable or R1 million), the bona fide inadvertent error comes into play.

There are two routes to avoid the penalty. The one is the bona fide inadvertent error defence. The other is a legal opinion from an independent registered tax practitioner on all the facts on which the taxpayer adopted a tax position.

Chong says it is notable that the first route – the bona fide inadvertent error defence – is not prefaced by “SARS is satisfied that”. “It is framed as an objective jurisdictional fact. If the understatement results from a bona fide inadvertent error, remission is mandatory,” she adds.

The second route is expressly subject to “SARS is satisfied that”. It requires the taxpayer to have made full disclosure to SARS of the arrangement that gave rise to the prejudice to the fiscus, by no later than the date the relevant return was due.

“In addition, the taxpayer must have been in possession of an opinion by an independent registered tax practitioner, also issued by no later than the return due date, confirming that the taxpayer’s position is more likely than not to be upheld if the matter proceeds to court.”

Estimated assessments

The amendment pertaining to estimated assessments addresses a “practical injustice” in the current framework, says Chong.

The Tax Administration Act allows SARS to issue an estimated assessment if a taxpayer fails to submit a return; submits a return or relevant material that is incorrect or inadequate; or fails to respond to requests for relevant material, even after multiple reminders. The estimated assessment is then based on SARS’s calculations of the tax liability.

“SARS can attach bank accounts and garnish salaries before the taxpayer has had any opportunity to show that the estimate is excessive or incorrect,” says Chong.

Mike Teuchert, tax partner at Forvis Mazars, explains that an estimated assessment differs from a revised assessment. The taxpayer can immediately object to a revised assessment and apply for a suspension of payment, halting the collection process.

However, with an estimated assessment, particularly once it becomes final, SARS will collect the tax even though the taxpayer wants to dispute it, he adds. This can be done by SARS attaching bank accounts or garnishing salaries.

However, the amendment to the Tax Administration Act now allows taxpayers who intend to request, or who request, a reduced assessment to apply for suspension of payment while SARS considers the request, adds Chong.

Theron gives an example where millions of rands flow through an account. The taxpayer neglects to respond to requests for information and SARS issues an estimated assessment of R10.

While the taxpayer gathers information that will satisfy SARS that the assessment is not correct, SARS can attach the bank account and collect R10m. “This is disastrous for many taxpayers,” he says.

At least the amendment now allows the taxpayer to request a suspension of payment while he submits a request for a reduced assessment.

Chong adds that the relief remains discretionary, and the familiar factors – risk of dissipation, compliance history, fraud, irreparable hardship, and tendered security – continue to apply.

“The amendment confirms, however, that the suspension mechanism is available in this category of cases. That confirmation closes a gap that has caused real hardship in practice,” she concludes.

Amanda Visser is a freelance journalist who specialises in tax and has written about trade law, competition law, and regulatory issues.

Disclaimer: The views expressed in this article are those of the writer and are not necessarily shared by Moonstone Information Refinery or its sister companies. The information in this article is a general guide and should not be used as a substitute for professional tax advice.