South Africa’s public finances have long been defined by a simple but stubborn arithmetic: when the government spends more than it collects, it borrows. For years, that borrowing snowballed into rising debt, rising interest costs, and shrinking fiscal room to fund growth. The 2026 Budget suggests that equation may finally be shifting.

In the Budget Speech on 25 February, Finance Minister Enoch Godongwana said: “For the first time in 17 years, debt will stabilise and it will continue to fall in the coming years. The budget deficit has narrowed significantly, and debt-service costs are also falling.”

That statement signals what National Treasury regards as a structural turning point rather than a temporary reprieve.

What South Africa owes – and to whom

South Africa’s gross loan debt is projected to reach R6.12 trillion in 2025/26, rising to R6.94 trillion by 2028/29. Net debt – which subtracts government cash balances – will increase from R5.91 trillion to R6.84 trillion over the same period.

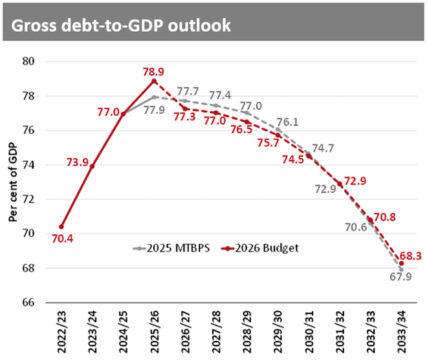

Those figures appear daunting, but sustainability is measured less by nominal debt than by debt relative to economic output. On that metric, the ratio is projected to stabilise at 78.9% of GDP in 2025/26 and decline to 76.5% by 2028/29.

The government borrows from three main sources:

- Domestic long-term lenders: retirement funds, insurers, banks, and institutional investors via government bonds. Domestic long-term borrowing is estimated at R387.9 billion in 2025/26 and will average R324.2bn over the next three years.

- Domestic short-term lenders: Treasury bills and borrowing from the Corporation for Public Deposits provide liquidity support. Net Treasury bill issuance is estimated at R40.7bn.

- Foreign lenders: Foreign-currency borrowing accounts for about 20.6% of total borrowing in 2025/26, projected to average 17.4% over the medium term. The government raised US$3.5bn in global markets and expects to raise about US$13.2bn from international institutions and capital markets.

National Treasury emphasises that foreign-currency debt will average only 10.5% of total debt, well below its 15% risk benchmark, limiting exchange-rate exposure.

Why debt rose so sharply – and why that trend is changing

Debt expanded rapidly over the past decade because deficits persisted while growth lagged. Interest costs compounded the problem. In 2025/26 alone, debt-service costs amount to R432.4bn, exceeding spending on basic education, health, or community development.

Recently, however, several fiscal indicators have begun improving simultaneously:

- The 2025/26 deficit is R12.4bn lower than projected last year.

- Debt redemptions were R12.2bn lower because of bond-switch operations.

- Revenue collections are projected to be R28.8bn higher than expected.

- Debt-service costs were revised down by R5.7bn for 2025/26.

Treasury attributes these shifts partly to improved macroeconomic conditions – including lower inflation, stronger bond yields, and a firmer rand – which have reduced borrowing costs and financing pressures.

The strategy: stabilise first, reduce later

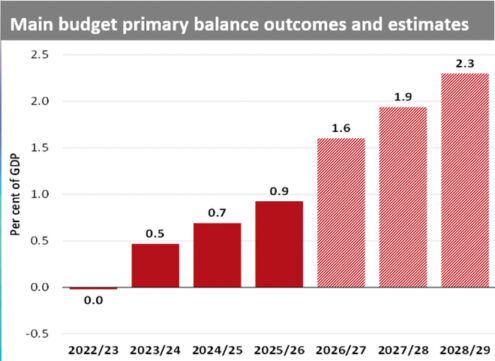

Fiscal consolidation now hinges on generating a primary surplus – where revenue exceeds spending before interest costs. The government expects to achieve a primary surplus of 0.9% of GDP this year and increase it steadily.

Treasury states: “Over the next three years, government has anchored fiscal policy with the primary budget surplus. With the continued increase in the surplus over the coming years, government debt will be on sustainable path.”

That approach matters because a sustained primary surplus gradually shrinks debt ratios even if total debt levels continue rising in nominal terms.

Surplus momentum strengthens the fiscal anchor

Treasury’s latest projections suggest that anchor is gaining traction. The main budget deficit and primary surplus for 2025/26 have both improved modestly, supported by stronger revenue collection, although partly offset by higher non-interest expenditure.

Debt-service costs over the medium term have been revised down by R10.6bn, reflecting improved bond yields, a stronger rand, and lower inflation and interest rates.

Most significantly, the main budget primary surplus is projected to rise from 1.6% of GDP in 2026/27 to 2.3% by 2028/29 – a trajectory that strengthens the credibility of the debt-stabilisation path.

Why borrowing is still rising – even as debt outlook improves

At first glance, continued borrowing may seem inconsistent with fiscal improvement. Treasury’s explanation is tactical: the government is borrowing opportunistically while interest rates are favourable.

Officials indicate that cheaper market rates allow the state to raise funds now at lower cost, build cash buffers, and refinance future obligations more cheaply. Cash balances are projected at R209bn in 2025/26, far above earlier estimates, helping to smooth liquidity pressures and partially finance future borrowing needs.

The gross borrowing requirement for 2025/26 is R563.4bn, down from R588.2bn projected previously. As a share of GDP, borrowing needs are expected to decline from 7.3% to about 5.5% over the medium term.

Markets are signalling renewed confidence

Several indicators suggest investors are reassessing South Africa’s risk profile:

- The country secured its first sovereign credit rating upgrade in 16 years from S&P Global Ratings.

- The yield curve strengthened by about 2.4 percentage points since the 2025 Budget.

- A December 2025 global bond issuance was oversubscribed.

- South Africa exited the Financial Action Task Force’s grey list.

S&P said the upgrade reflected an improving growth and fiscal trajectory and noted that the government is on track to record its third consecutive primary surplus while contingent liabilities from state-owned companies are easing.

National Treasury Director-General Dr Duncan Pieterse indicated that engagement with rating agencies has shifted from routine consultation to a more assertive approach, with Treasury scrutinising their models and assumptions to ensure that South Africa’s fiscal outlook is assessed on accurate and transparent data.

The hidden risk: guarantees and state-owned enterprises

Not all fiscal risks sit on the balance sheet. Government guarantees to state-owned entities and infrastructure programmes are projected to rise from R513.1bn to R661bn between March 2025 and March 2026.

Exposure – the actual value at risk – is expected to reach R453.6bn, with Eskom accounting for 73.6% and Transnet 17.3%. Although Eskom’s exposure is declining because of debt-relief measures, these guarantees remain a significant fiscal vulnerability.

The real turning point

The most consequential shift is not the absolute level of debt but its trajectory. Treasury states: “Government debt as a share of economic output is expected to reach its peak in the current fiscal year and will decline over the next few years. This is an important turning point, because as debt decreases, so do debt-service.”

Growth in debt-service costs is projected to slow to 3.7% annually, down from 7.4% previously. For the first time this decade, these costs will grow more slowly than overall expenditure.

What this could mean for the future

Lower debt ratios and borrowing costs have tangible implications:

- More fiscal room for infrastructure and social spending;

- Reduced vulnerability to global rate shocks;

- Lower investor risk premiums;

- Stronger currency stability; and

- Greater policy autonomy.

Godongwana framed the stakes in sovereign terms: “With the health of our public finances comes a greater degree of economic freedom and sovereignty. It is this sovereignty that gradually frees us from over-reliance on external debt. It shields us from the inherent uncertainties of global finance and global politics.”

So – is the fiscal house finally in order?

Not yet. Debt remains high, state-owned enterprise risks persist, and growth must accelerate for improvement to endure. But for the first time in nearly two decades, deficits, borrowing costs, ratings signals, and investor demand are all moving in the right direction at once.

The signs are there. The question now is whether policy discipline and economic reforms can sustain the momentum long enough to lock in the turnaround.