Adopting an aggressive investment strategy in retirement seems counterintuitive. New actuarial modelling shows, however, that most living annuity investors need to consider higher equity exposure, together with lower drawdown rates, to avoid running out of money.

Applying a statistical process called “bootstrapping”, investment actuary Joao Frasco, a Fellow of the Actuarial Society of South Africa, simulated a wide range of investment returns drawn from 20-year historical data. According to Frasco, this approach creates a wide range of potential investment outcomes, including some that could have been much worse for investors than the actual returns observed over the past 20 years.

The purpose of the research was to investigate the probabilities of success for living annuity withdrawal rates ranging from 2.5% to 17.5% using different investment strategies, Frasco says.

He says the focus of the research was not to determine a “safe” outcome, but to show how the probabilities of success were influenced by choices of withdrawal rates and investment strategies over different periods and age groups.

Frasco produced thousands of simulations for a combination of variables for a living annuity investment. The aim was to understand the combination of withdrawal rate and investment strategy most likely to result in successful capital preservation over the time horizon appropriate for the pensioner.

The simulations were based on randomly drawn monthly real returns for the FTSE/JSE All Share Index (Alsi), as well as for an unnamed South African multi-asset high-equity fund (maximum 75% exposure to equities), a South African multi-asset low-equity fund (maximum 40% exposure to equities), and a South African interest-bearing short-term fund (no equity exposure). These four investment options were chosen to show the results along the investment risk spectrum available to South African investors.

Frasco notes that returns simulated for the unit trust funds are net of manager fees but do not reflect adviser or platform costs. No allowance has been made for fees for Alsi returns.

“To account for fees and taxes, investors and their advisers should increase the withdrawal rate by the corresponding percentage. If, for example, you wanted to make an allowance for a 0.5% adviser fee, you could simply increase the withdrawal rate by 0.5%.”

Probability of success

Frasco says his research covered periods up to 35 years to make it useful for people at the start of their retirement and periods as low as five years for the elderly.

“While withdrawal rates of 10% are generally unsustainable for most living annuity investors irrespective of the investment strategy, this is not necessarily true for someone in his or her 80s and in poor health.”

Frasco found that the only living annuity investors who could avoid market volatility completely by opting for an interest-bearing fund were those with a five-year investment horizon. He adds, however, that this situation would apply only to an investor with a very short life expectancy.

Probability of success: 5 years

Frasco notes that over a five-year period, irrespective of the drawdown rate selected, a living annuity invested in a SA interest-bearing fund will not run out of money. There is a very small chance, however, that a living annuity investment with high equity exposure could fail if the withdrawal rate is higher than 15% because there is a chance of consecutive negative returns over shorter investment periods.

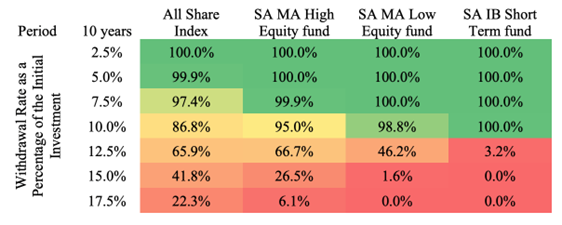

Probability of success: 10 years

According to Frasco, the outcomes change significantly if the investment period is extended to 10 years.

While the SA interest-bearing short-term fund has a 100% probability of success for withdrawal rates up to 10%, the success rate drops rapidly to only 3.2% for a withdrawal rate of 12.5%.

“A high-equity investment, on the other hand, is likely to deliver a much higher probability of success. At a withdrawal rate of 12.5%, a high-equity investment has a probability of success of between 86.8% and 95%. Investors would, however, have to stomach a fair amount of volatility, which is expected for high-equity investments.”

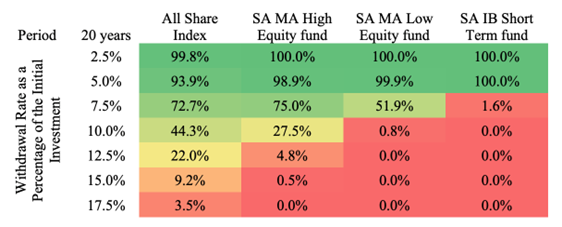

Probability of success: 20 years

Frasco explains that over 20 years, a withdrawal rate of up to 5% is unlikely to erode the living annuity capital, irrespective of the investment approach. He says this is why withdrawal rates below 5% are considered sustainable in most cases.

However, as soon as the withdrawal rate is increased to 7.5%, the likely success rate drops to a mere 1.6% if the capital is invested only in an interest-bearing fund, while a high equity exposure comes with a 75% probability of success.

“This points towards the need for equity exposure for most investors looking to draw income at rates above 5%,” Frasco says.

Probability of success: 25 years to 35 years

Frasco says periods up to 35 years were modelled for investors considering retiring and investing their capital in a living annuity at younger ages. He adds that the younger the investor, the more important the investment strategy because younger people have a longer life expectancy.

He says the highest probability of not running out of money for a living annuity investor with a time horizon of between 25 and 35 years would be maintaining a drawdown rate below 5%, with equity exposure of up to 75% (as offered by South African multi-asset high-equity funds).

What about mortality?

Frasco says he embarked on this research project mainly to provide financial advisers with the tools to have more meaningful retirement conversations with their clients.

“Being able to sit in front of a client, demonstrating how their decisions could impact their probability of a successful retirement, could change the conversation from merely protecting capital and avoiding risk to the need for taking the risk to improve the chances of success,” Frasco says.

The second part of his research, therefore, brings mortality assumptions into the picture, which is critically important when financial advisers discuss appropriate investment strategies with their clients. However, mortality assumptions add to the complexity of the outcome because they require taking a view on an individual’s mortality and how it may differ from the population on which mortality rates are based.

For example, says Frasco, since women typically live longer than men, the probability of success will be different for female clients and male clients even when all other assumptions are identical.

Disclaimer: The views expressed in this article are those of the Actuarial Society of South Africa and are not necessarily shared by Moonstone Information Refinery or its sister companies. The information in this article does not constitute investment or financial planning advice that is appropriate for every individual’s needs and circumstances.

Interesting. Since there is only a 50% (approximately since it is the mean, not the median) chance of dying within your life expectancy and a fair chance of living to at least double this, the period should be at least double your life expectancy. Thus, from this, we can conclude that for a life expectancy of 10 years or more (so need to provide for a period of 20 years or more) you should not draw more than 5% per annum, and if you need a higher income, then instead of increasing your drawdown rate, you should rather put a large portion in a life annuity instead of a living annuity , unless the life annuity rates are particularly low at that stage due to low long term interest rates. Secondly, when interest rates (particularly long term rates) are high, then a bond fund (SA IB Variable) would be better than the SA IB Short Term Fund, but this was not considered in the above article.