Excess contributions to retirement funds are increasingly becoming one of the most discussed retirement planning issues among investors and their financial advisers. Many are asking whether excess contributions should be intentionally engineered into a retirement plan to improve tax efficiency and long-term outcomes.

One of the appeals of excess contributions for retirees is that they can offset tax on living annuity drawdowns, sometimes eliminating income tax entirely for a period of years.

During a recent webinar, Wynand van der Berg, a business analyst in Allan Gray’s retail product development team, said although excess contributions can be a retirement planning powerful tool, their impact is highly context specific. What works brilliantly for one investor can underperform – sometimes significantly – for another with a different portfolio mix, income need, or tax position.

To make his point, Van der Berg introduced “Investor X” – a recently retired individual with a mix of retirement annuity savings and discretionary platform investments – and examined three competing strategies side by side.

The three strategies

Option 1. 100% into a living annuity. The discretionary investments are liquidated, and the proceeds are invested in a retirement annuity. This creates a pool of excess contributions that can offset tax on future living annuity withdrawals. All drawdowns come from the living annuity and benefit from the excess contribution offset.

Option 1 is the baseline for the comparison because the analysis focuses on excess contributions. Whatever net cash flow Investor X receives in Option 1, he wants to receive the same net cash flow in Option 2 and Option 3.

Option 2. Maintain the existing structure. Retire only the existing RA to a living annuity. The discretionary platform account is untouched. Drawdowns are split between the living annuity and the discretionary account.

Option 3. Discretionary savings moved to an endowment. Disinvest the discretionary platform account, reinvest the net proceeds into an endowment policy, alongside a living annuity from the RA.

Modelling framework and key assumptions

To illustrate the outcomes, the presentation applied a set of consistent modelling assumptions:

- Total investment return of 10% a year (7.6% capital growth, remainder distributions).

- 20-year projection period, after which the investor dies, and his beneficiaries take 100% of the proceeds in cash.

- All distributions are reinvested net of the relevant tax (product-level tax for endowments or the investor’s marginal rate).

- Moving from the discretionary platform account triggers a capital gain of 40%.

- The investment into the RA or the endowment is net of the capital gain tax.

- No lump-sum withdrawal has been taken at retirement.

- Maximum executor’s fees are applied (3.5% + VAT = 4.025%).

- Withdrawals occur annually and are sized to produce identical net cash flow to the investor across all three options.

- Appropriate marginal tax rates apply dynamically because withdrawals affect taxable income.

- Estate duty and capital gains tax are applied per current legislation.

Van der Berg emphasised that small changes to the underlying assumptions can materially alter the outcomes.

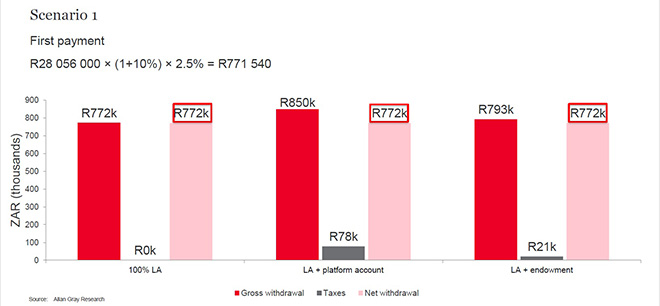

Scenario 1. Portfolio dominated by discretionary savings

This case tests what happens when most of the assets are outside a retirement fund, which, as Van der Berg noted, is highly unusual.

Investor X has R30 million in total assets, consisting of R27m in discretionary investments and R3 million in RA assets.

If Investor X chooses either Option 1 (converting the discretionary assets into a living annuity) or Option 3 (moving the discretionary assets into an endowment), the discretionary portfolio must first be liquidated. Given the assumed 40% capital gain, this disposal triggers approximately R2m in CGT, calculated using a 45% marginal tax rate.

Net of CGT, the starting investment value for Options 1 and 3 is about R28m, compared with R30m if the investor retains the existing structure under Option 2.

Under Option 1, converting the discretionary portfolio into a living annuity generates approximately R24.6m in excess contributions. At a 2.5% drawdown rate, these excess contributions would offset taxable withdrawals for roughly 18 years. During this period, the withdrawals from the living annuity are effectively shielded from income tax because they are offset by the excess contribution balance.

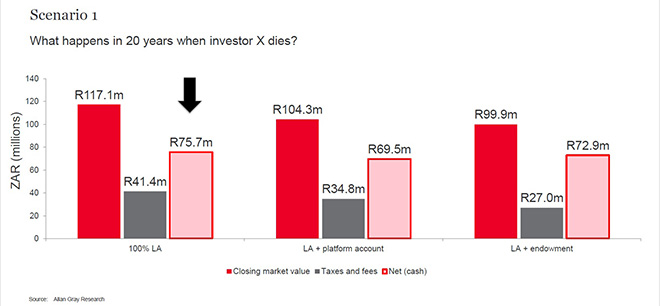

The modelling projects each option forward for 20 years using the assumed 10% annual investment return.

Despite the initial CGT cost, Option 1 produces both the highest closing market value and the highest net value to beneficiaries after accounting for taxes.

This seems to suggest that using excess contributions is always the preferred retirement strategy, but Van der Berg said this outcome is highly dependent on the assumptions made. Different assumptions could easily lead to different outcomes.

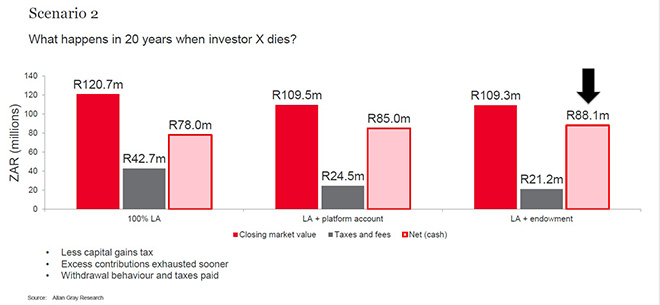

Scenario 2. Balanced retirement and discretionary assets

The investor again has R30m in total assets, but the composition is now R15m in retirement savings and R15m in discretionary investments.

The investor again assumes a 2.5% drawdown rate in retirement.

If the discretionary investments are converted under Options 1 or 3, the disposal triggers approximately R1m in CGT, reflecting the smaller discretionary portfolio relative to Scenario 1.

After paying CGT, the starting value for Options 1 and 3 is about R29m, while Option 2 retains the full R30m.

Under Option 1, Investor X will accumulate approximately R13.5m in excess contributions.

Because Investor X already has a larger pool of retirement savings, withdrawals from the living annuity occur from a larger base. As a result, the excess contribution pool is depleted more quickly. In this scenario, the excess contributions last approximately 12 years, compared with 18 years in Scenario 1.

When the portfolio is projected forward over the 20-year horizon, the results change significantly.

Although Option 1 still produces the highest closing market value, Option 3 (combination of a living annuity and an endowment) produces the highest net value to beneficiaries after accounting for taxes and fees.

Two factors explain this shift, said Van der Berg. First, the CGT cost of restructuring the portfolio is lower, leaving more capital available for compounding. Second, the excess contributions are exhausted sooner, which reduces the long-term tax advantage of Option 1.

In addition, the investor’s marginal tax rate in this scenario is assumed to be above 30%, which means that the endowment’s flat internal tax rate of 30% becomes relatively favourable.

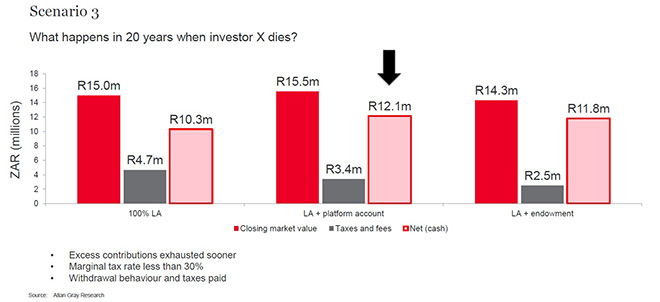

Scenario 3. Smaller portfolio with higher withdrawals

The third scenario considers an investor with R6m in total assets, split equally between retirement and discretionary savings.

Because the portfolio is smaller, Investor X assumes that a 5% drawdown rate will be required to sustain his lifestyle.

If discretionary assets are converted under Options 1 or 3, the disposal triggers approximately R150 000 in CGT. This leaves a starting investment value of about R5.85m for Options 1 and 3, compared with R6m under Option 2.

If the investor chooses Option 1, converting discretionary assets into retirement vehicles would generate approximately R2.4m in excess contributions.

However, at a 5% drawdown rate, these excess contributions are exhausted far more quickly – lasting only about seven years.

When the portfolio is projected over the same 20-year horizon, the results change again.

In this scenario, Option 2 produces both the highest closing market value (R15.5m) and the highest net value to beneficiaries (R12.1m).

Option 3, which includes an endowment, performs slightly worse, while Option 1 – the excess contribution strategy – produces the weakest outcome.

The reason is that the excess contribution pool is depleted relatively quickly, limiting the tax benefit. In addition, the investor’s marginal tax rate in this scenario is below the endowment’s internal tax rate of 30%, removing the tax advantage of the endowment structure.

Three critical factors

Van der Berg distilled the decision down to three quantifiable drivers that advisers should assess for every client:

- Drawdown percentage on the living annuity. The higher the required drawdown, the faster excess contributions are exhausted. The longer they last, the stronger Option 1 becomes.

- Size of existing retirement savings. A larger pre-existing RA balance accelerates the use of any new excess contributions, shortening their effective life.

- Overall portfolio size and resulting marginal tax rate. Larger portfolios push investors into higher tax brackets. When the marginal rate exceeds the endowment’s flat 30% rate, the endowment becomes attractive once excess contributions are depleted. Smaller portfolios often favour the discretionary platform.

Additional considerations beyond the numbers

Several important factors fell outside the quantitative model but remain crucial for holistic advice:

- Executor’s fees are negotiable. The analysis assumed the statutory maximum; a lower negotiated fee would improve the relative attractiveness of Option 2 in every scenario.

- The investment time horizon matters enormously. A shorter or longer life expectancy would alter the compounding benefit of upfront CGT versus tax savings.

- Liquidity and access rules differ markedly. Living annuities are capped at a 17.5% maximum drawdown; discretionary and endowment accounts generally offer greater flexibility in emergencies.

- Regulation 28 applies to new contributions made to accumulate excess capacity. This may constrain asset allocation and potentially affect long-term returns compared with an unconstrained discretionary account.

- Section 37C of the Pension Funds Act introduces estate planning complexity. On premature death, retirement fund death benefits (including living annuity assets) may be paid to dependants rather than strictly following a nominated beneficiary, whereas discretionary and endowment assets pass directly according to the will or nomination.

Concluding thoughts

Van der Berg closed the session by reinforcing the central message he had woven throughout: excess contributions are a valuable tool, but never a default strategy. Their effectiveness depends critically on the interplay of drawdown rate, existing retirement savings, portfolio size, marginal tax bracket, and time horizon.

He cautioned against the temptation to treat excess contributions as a universal tax “hack”. In some realistic client situations – particularly those with high drawdown needs, modest portfolios, or lower marginal tax rates – moving discretionary savings into an RA to create excess contributions can reduce the net amount ultimately received by beneficiaries. In other cases, an endowment wrapper, or simply retaining the existing discretionary structure, proves superior.

His final advice to advisers was clear and practical: run the numbers for each client using their actual portfolio composition, required drawdown, tax position, and estate objectives. Only then can you determine whether deliberately accumulating excess contributions will genuinely optimise the long-term outcome – or whether another approach will deliver a better net result for both the client in retirement and their heirs.

Disclaimer: This article is a general summary of the webinar and does not constitute financial, tax, or investment advice. Investors should consult their financial adviser and tax practitioner for advice tailored to their personal circumstances.