At last – after two years of no tax relief, the personal income tax (PIT) brackets and the medical tax credits will be adjusted in Budget 2026 to account for inflation. However, there will be increases to the taxes on fuel, albeit below projected inflation.

As is the norm, the excise duties alcohol and tobacco will increase, although speculation that these increases might far exceed inflation has proved incorrect.

The 2025 Budget and the 2025 Medium-term Budget Policy Statement provisionally included R20 billion in tax increases for the 2026 Budget, which was to be reconsidered if the South African Revenue Service could collect an additional R20bn in tax debt, National Treasury said in the Budget Review.

Although SARS is unlikely to meet its target, the government has withdrawn the proposed R20bn in tax increases for the 2026/26 tax year because of improving fiscal metrics and the potential negative impact on the economy from additional tax increases, Treasury said.

Personal income tax

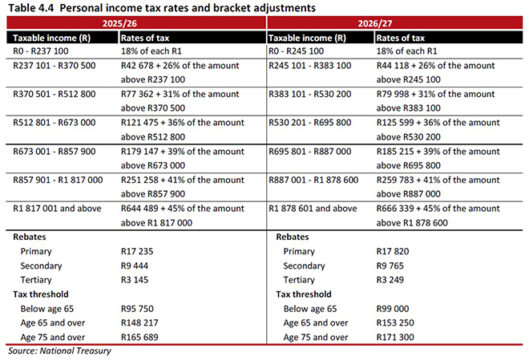

The PIT brackets and rebates for 2026/27 will be adjusted by 3.4%, “in line with expected inflation”, according to the Budget Review. The last tax year for which the brackets were adjusted for inflation was 2023/24.

“Bracket creep” describes what happens if the income bands are not fully adjusted to account for inflation-linked salary or wage increases. Taxpayers whose salaries are adjusted in line with inflation may be pushed into a higher tax bracket and pay relatively more in income tax.

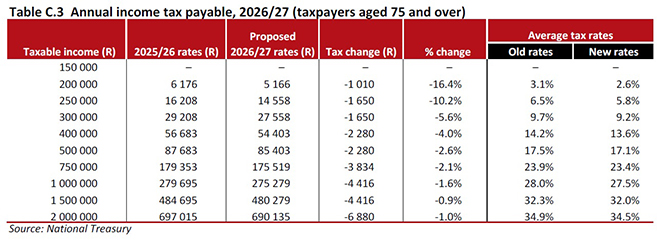

Treasury told Moontone it will forfeit R13.7bn in revenue because of the adjustments to the tax brackets and rebates in 2026/27.

As welcome as the adjustment is, it will not fully compensation taxpayers for the loss of purchasing power since March 2023. Treasury will still benefit from the past two years of bracket creep because the adjustment to the PIT brackets in the coming financial year will only take account of last year’s inflation.

The entry threshold for income tax rises from R95 750 to R99 000 for taxpayers under 65, from R148 217 to R153 250 for those aged 65 and over, and from R165 689 to R171 300 for taxpayers aged 75 and over.

The table below shows the amended tax brackets and thresholds for individual taxpayers.

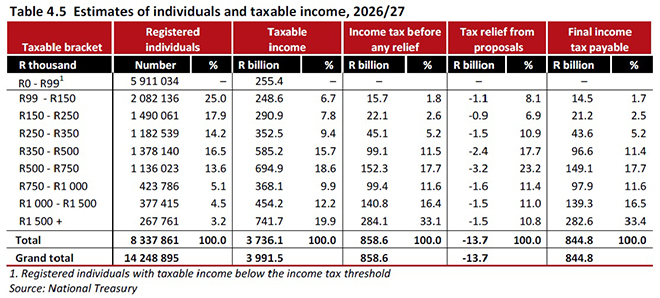

The table below shows the impact that the bracket adjustments will have on the different taxable income bands.

The Budget Review notes that the PIT system relies heavily on a narrow tax base. The top 13% of individual taxpayers pay more than 60% of PIT, and nearly half of PIT is paid by the 7.7% of taxpayers with taxable income above R1 million a year.

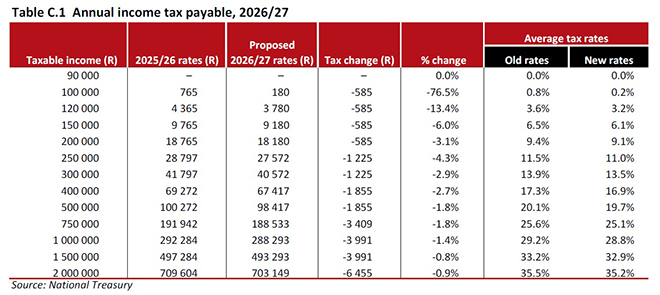

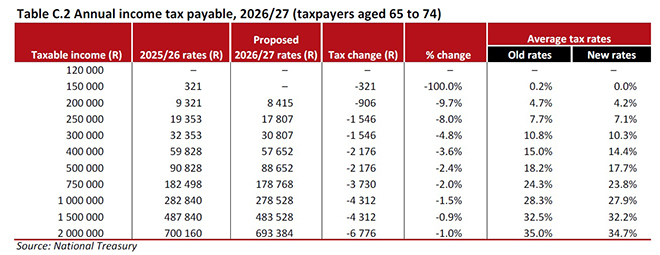

The tables below show how the tax rates for taxpayers under the age of 65, between 65 and 74 years, and over the age of 75, respectively, will change because of the adjustments to the income tax brackets and rebates.

Medical tax credits

The medical scheme fees tax credits will be increased. The credit for the first two beneficiaries will increase by R12, or 3.2%, from R364 a month to R376 a month. The credit for each additional beneficiary will increase by R8, or 3.1%, from R246 a month to R254 a month.

The adjustments to the medical tax credits will result in Treasury forfeiting R1.2bn in revenue in 2026/27.

Treasury provided R29.53bn in tax credits to medical scheme members in 2023/24, and R8bn more in tax credits for qualifying out-of-pocket healthcare expenditure, according to the Budget Review.

Treasury is proposing tax amendments that will extend the eligibility to include members of certain statutory medical schemes that do not fall under the Council for Medical Schemes. Members of these schemes are not eligible for the medical scheme fees tax credit under section 6A of the Income Tax Act. Treasury proposes that eligibility be extended to these members, provided their medical schemes adhere to the governance and solvency requirements of the Medical Schemes Act. It was not immediately clear to which schemes this would apply.

Fuel levies

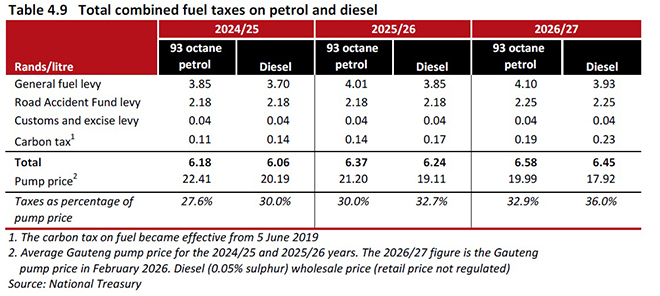

Three of the four taxes levied on fuel sold at the pumps will increase from 1 April.

The general fuel levy will increase by 9 cents on a litre of petrol, from R4.01 to R4.10, and by 8 cents on a litre of diesel, from R3.85 to R3.93.

The Road Accident Fund levy will increase by 7 cents a litre on both petrol and diesel, from R2.18 to R2.25.

The carbon tax on petrol will increase by 5 cents a litre, from 0.14 cents to 0.19 cents, and by 6 cents on diesel, from 17 cents to 23 cents.

The customs and excise levy on petrol and diesel will not be increased, remaining at 4 cents a litre.

The government says it will raise R2.13bn in 2026/27 from the increases in the general fuel levy and the carbon tax.

Excise duties on alcohol and tobacco

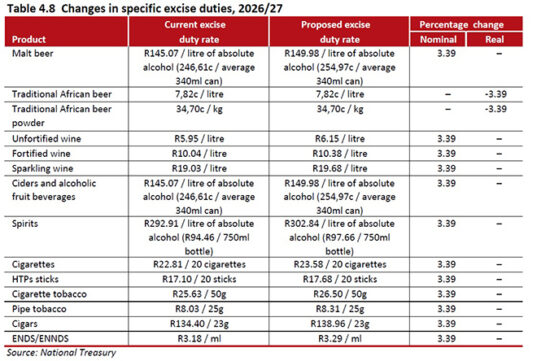

The government proposes to increase by 3.39% the excise duties on alcoholic beverages and on tobacco products. This includes excise duty on electronic nicotine and non-nicotine delivery systems (vaping).

From the 2027 Budget, excise duty adjustments will take effect on 1 April. The required legislative amendments will form part of the taxation laws amendment bills this year.

Revenue collections and outlook

National Treasury revised the gross tax revenue estimate for 2025/26 up by R21.3bn from the 2025 Budget estimate, despite lower-than-expected nominal GDP. The tax-to-GDP ratio is expected to increase from 25.1% in 2024/25 to 25.9% in 2025/26.

The R21.3bn includes a R15.3bn overshoot on value-added tax, a R7.8bn overrun on corporate income tax, and a surplus of R4.2bn on dividends tax.

Treasury attributes the higher net VAT collections to resilient household consumption expenditure and lower VAT refunds.

However, PIT and specific excise duty collections are expected to fall short of the projects in the 2025 Budget. PIT is running R6.2bn behind last year’s Budget estimates.

Gross tax revenues are expected to be R14.8bn lower in 2026/27 and R37.9bn lower in 2027/28, relative to the estimates outlined in last year’s Budget.

Provisional corporate tax collections have grown, except for the manufacturing sector.

Corporate profitability increased during 2025, with mining tax collections in December 2025 up by 29% compared with December 2024 because of high platinum group metals and gold prices.

Treasury said although the near-term benefit of the upswing in the prices of precious metals is positive for the revenue outlook, the gains are expected to be lower than in the previous period of high commodity prices (2020/21 to 2022/23) because a narrower set of commodities is benefiting from high prices. Coal and iron ore prices, for example, saw large increases in the previous commodity boom and contributed to higher revenue, but have remained relatively flat this time around.

Dividends tax collections were boosted by large once-off collections from the mining and retail sectors and a recovery in corporate profits.

Strong growth in collections from fuel importers drove overall fuel levy collections. Collections recovered in 2025/26 following a sharp drop in demand in the previous year, reflecting reduced diesel usage because of improved electricity supply.

PIT collections are projected to fall short of the estimates in the 2025 Budget by R6.2bn, reflecting subdued private sector wage growth.

Specific excise duties are also expected to underperform because cigarette and petroleum products receipts contracted over the first 10 months of 2025/26 compared with the same period in the previous year.

I think gepf pensioners should be excluded from tax, why? Becouse they are not benefiting from any grant from government ie old age grants, as well as basic grants, like water and electricity. That should be considered, we also elders in the same country and we were paying taxes since we were employed even now.

Totally agree

Do not tax pensioners. They have paid their due. All they have to live on is what they have managed to put away while working. Why penalize old people. It’s unfair. Brings unnecessary stress and uncertainty to an already frail generation.

I agree strongly with you.

For 40 years or more they pay taxes, pay a lot of money to have a pension and not to be a burden on the goverment when they go on pension and then the have to pay tax upon tax on their pension money. The goverment did not have to give them any grants, but the have to pay tax.

Not fair to still let the people who fund the goverment for years with their taxes, pay tax when they are old and on pension.

No tax for 80 years and older please

I agree that pensioners from 75 yrs and above should no longer be taxed. Especially those over 80 yrs and having to still help family members are under much stress daily and especially when having to hand in and pay their tax obligations. It is a very sensitive and vulnerable age when every second of life is so uncertain and unpredictable.

stop taxing people for their addiction rather help them with their addiction drinking is also the only entertainment in their lives government thinks its punishing them for sin