Alexforbes released its latest Manager Watch Survey last week, providing a detailed view of South Africa’s retirement fund investment industry at a point where both market conditions and longer-term assumptions are shifting.

The firm framed the December 2025 edition around the theme “the next 30 years: strategy for a changing world”, positioning the survey as examining how asset managers and allocators are adapting to shifting economic, regulatory, and market conditions.

That framing was reinforced by the investment backdrop outlined by in a presentation by Janina Slawski, the head of investment consulting at Alexforbes. By the end of 2025, conditions appeared to be improving, supported by moderating inflation, fiscal discipline, and sovereign upgrades. However, Slawski noted this trajectory shifted abruptly on 28 February, when geopolitical developments linked to the military action by the United States and Israel against Iran unsettled markets and altered the outlook.

The latest survey covers 30 individual surveys – 15 balanced, 14 specialist and a multi-manager survey – spanning 94 asset managers and 875 strategies, alongside insights drawn from Alexforbes’ June 2025 Assets Under Management Survey. This represents year-on-year increases of 2.2% in managers and 9.8% in strategies.

Participation has broadened across categories, with particularly strong growth in transformation-focused offerings. Presentation data shows that BEE strategies increased to 193 in 2025, representing the largest increase among all survey categories.

Over a longer period, the number of participating managers and strategies has steadily increased, reflecting both product proliferation and expansion of the institutional investment universe.

Assets under management and rankings

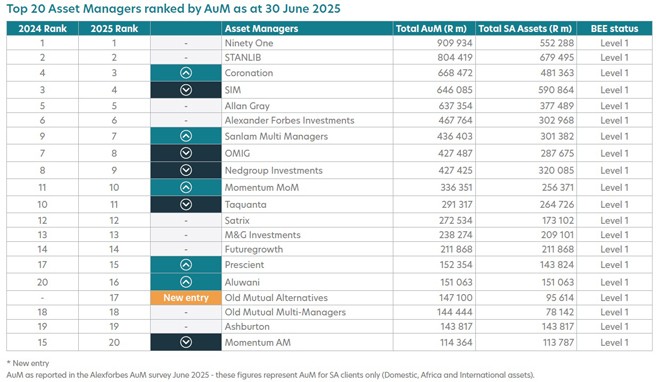

Ninety One remained the largest asset manager by South African client assets, increasing its AUM by 6% compared with the previous year. Stanlib retained second place, recording growth of 13% in assets over the same period.

Coronation moved into third place after reporting 17% growth in assets. Sanlam Investment Management (SIM) moved down one place to fourth, although it reported growth of 9%. Allan Gray remained in fifth place, with AUM increasing by 14%.

Alexander Forbes Investments strengthened its position as the leading multi-manager in South Africa. It remained in sixth place, supported by a 10% increase in AUM over the past year.

The growth of multi-managers relative to single managers continued in 2025. In 2019, for every R1 managed by single managers, multi-managers held 15 cents. By 2025, this had doubled to 30 cents.

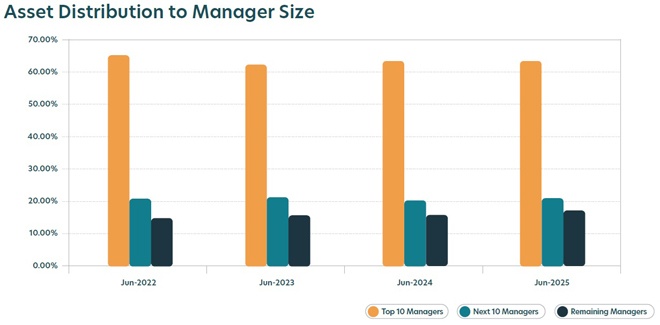

Total assets reported by participants increased by 13% year on year. However, the survey indicates that this growth has not materially altered market concentration: the top 10 managers account for about 62% of the total assets across the managers included in the survey. The share of assets held by the largest managers has remained broadly stable over time. Alexforbes attributes this trend to increased use of diversified implementation approaches by institutional investors.

Transformation and BEE trends

The survey highlights transformation as a significant and continuing feature of the asset management landscape.

The number of BEE-focused strategies increased by 17% in 2025, continuing a multi-year upward trend.

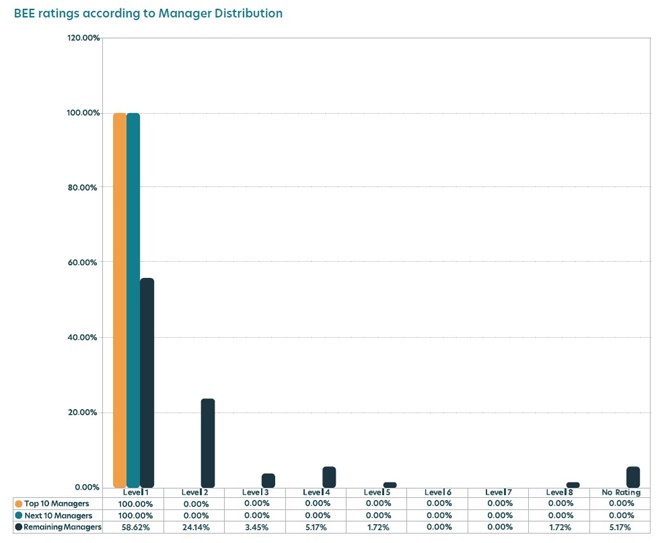

In terms of manager ratings, 54 managers were rated as Level 1 contributors, an improvement from 52 in the previous year. In addition, the top 22 asset managers in the survey all achieved a Level 1 rating.

“These results show that leading asset managers are increasingly aligning their strategies with transformation objectives. The continued rise in Level 1 ratings suggests that BEE compliance remains a priority across the South African asset management industry,” according to the survey.

Slawski said the increase in BEE strategies is a response to client demand and regulatory drivers. She noted that institutional clients are increasingly setting minimum allocation targets to transformed managers, alongside expectations from regulators and policymakers.

In 2024, Level 1 and Level 2 contributors accounted for 92% and 4% of total assets, respectively. In 2025, this trend continued, with Level 1 contributors increasing to 94% of total assets, while Level 2 contributors declined to 3% compared with the previous year.

The growth of black-owned asset managers has also continued. According to the June 2025 AUM survey, the top five black-owned asset managers recorded an 11% increase in total assets compared with June 2024.

Five BEE survey participants secured positions in the top 10 of the AUM survey, while 12 majority black-owned managers ranked within the top 20. “This progress highlights the continued advancement of transformation in the asset management industry. It also demonstrates that black-owned investment businesses are growing within the market,” the survey said.

Asset allocation trends

The survey’s Best Investment View (BIV) portfolios provide insight into how managers are positioned across asset classes.

Survey data shows that domestic allocations remain significant, particularly in the South Africa BIV category, which maintains a high exposure to local equities.

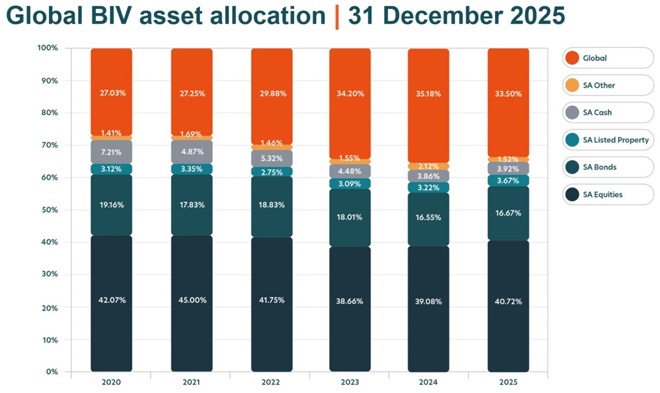

In the Global BIV category, 40 of 53 managers allocate more than 30% to global assets, with an average offshore allocation of 33.5%. This follows a steady increase in global allocations in recent years, with exposure rising to 35.2% in December 2024.

Slawski indicated that changes in asset allocation during 2025 were largely driven by relative asset class performance rather than significant strategic repositioning. Strong domestic equity returns increased local weightings, while weaker offshore returns reduced the relative contribution of global assets.

Investment performance

Survey data shows that 2025 was a strong year for South African markets. The FTSE/JSE All Share Index (ALSI) returned 42.4%, compared with 13.4% in 2024.

Within the SA Equity Manager Watch survey universe, managers delivered an average return of 44.1% for the year, 34 portfolios outperformed the ALSI, and the top-performing fund returned 48.9%.

Within the SA BIV category, all managers delivered positive returns, with 10 of 19 outperforming the median return of 31.9%. The top-performing portfolio in the SA BIV category was Mergence Domestic Balanced Fund, which delivered a return of 37.2% in 2025.

The Global BIV category recorded a lower median return of 21.1%. Twenty-nine out of the 53 portfolios outperformed the Global BIV median. The best performer in the category was the Nedgroup Investments (Truffle) Balanced Fund, which returned 32.8% for the year.

Slawski said that by the end of 2025, South Africa seemed to be moving into a more stable, lower-inflation, fiscally disciplined regime. Yield curves had fallen, sovereign upgrades had come through, and optimism was starting to rebuild. Then, on 28 February, the United States and Israel launched major strikes against Iran, unsettling markets and clouding the outlook once more. The next survey, Slawski suggested, is likely to show sharp reversals in some of the patterns that emerged recently.

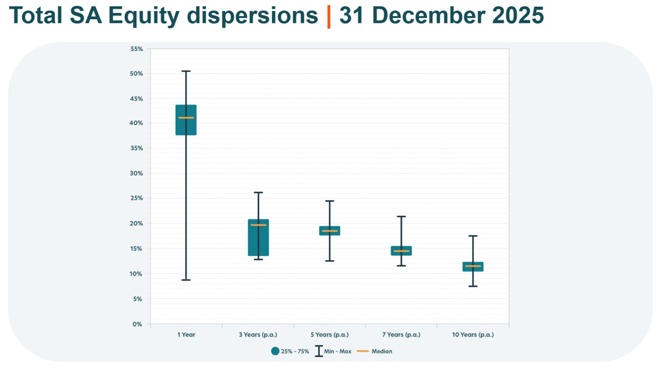

Wide dispersion – particularly among equities

The strong headline returns mask significant dispersion across asset classes, within asset classes, and between managers.

The most pronounced dispersion is observed within South African equities.

Slawski noted that the local market is characterised by a relatively small number of listed companies and wide variation in performance between sectors and individual stocks. This dispersion reflects both sectoral differences and stock-specific outcomes. As a result, portfolio performance was highly dependent on stock selection during the period.

But the challenge for active managers is not simply one of insight; it is also one of risk tolerance. In periods when a single sector or small group of stocks drives the bulk of market returns, indices become heavily concentrated. Many active managers are unwilling – or unable, under mandate constraints – to take on such concentrated exposures. That means benchmarks can soar on the back of a few dominant names, while diversified active portfolios struggle to keep up. As Slawski noted, this led to many active managers underperforming their benchmarks in 2025, despite applying prudent risk controls.

Although the past year highlighted the short-term challenges of staying with active management in a concentrated market, the survey suggests that over extended time horizons, active allocations can still add value.

Low-return environment over 10 years

Slawski referred to the theme of the low-return environment, particularly over 10‑year horizons in relation to the global large manager returns.

The one-, three- and five‑year numbers have seen “quite a dramatic improvement,” pulled up by the very positive returns of 2025. By contrast, she described the 10‑year returns as “still quite challenged”.

She contrasted current conditions with earlier decades, saying it is unlikely there will be a return to the times when investors were seeing returns of 20% a year that were compounding over 10 years.

She linked this shift to changes in South Africa’s economic profile. Slawski said the country was “becoming more and more of a developed market, becoming more like Australia than maybe the rest of the BRICS countries”. She explained that in a low-inflation environment, where “you don’t expect your rand to depreciate as much, because the inflation differentials are less compared to the developed world”, the expectation is that overall returns will be lower in nominal terms – and contracting in terms of real returns.

Slawski added that if South Africa is seen as a less risky environment, it is “less likely to get returns to compensate for the lower level of risk”.

Under these conditions, “asset allocation becomes different, more challenging”. Therefore, it may be necessary to look at either taking more risk into accumulation portfolios for retirement funds or potentially tempering some of the expectations and looking at different post-retirement annuity strategies.

Bonds: exceptional one year, flat over the longer term

On South African bonds, Slawski drew a distinction between the latest year and the longer-term picture.

The one‑year return was “extremely positive because of the yield curves moving down, which reflected the impact of the sovereign upgrades and a shift in expectations. However, over five, seven, and 10 years, the results were “a lot less exciting”.

She said bond investors could expect more pedestrian returns going forward, because there’s less compensation for a sovereign risk after the upgrades, while also acknowledging uncertainty given geopolitical developments and concerns about oil prices.

Partial recovery in property

Slawski said listed property has been a challenging asset class for some time, citing “very bad returns” around 2018 and a further decrease in returns because of the Covid lockdowns. She said that more recently there had been “some nice recoveries”, and the one‑year figures now “almost look like a normal picture”.

Despite this recovery, property remains “quite challenged” over longer periods. Slawski noted the wide dispersion in returns across the property universe, saying stock-picking is essential to demonstrate outperformance within the asset class.

Looking ahead

Taken together, the survey points to an industry that is evolving along several dimensions: increasing use of multi-managers, continued progress in transformation, and a growing emphasis on diversification and manager selection.

At the same time, the investment environment is becoming less predictable. The shift from improving conditions at the end of 2025 to renewed uncertainty following events in early 2026 highlights the need for flexibility in both strategy and implementation.

In that context, the survey highlights the need for asset managers and institutional investors to adapt to a world characterised by lower returns, changing risk premia, and more variable market conditions over the coming decades.